Post

PostRebuilt vs. Salvage Title: Key Differences, Costs, & Insurance (2026)

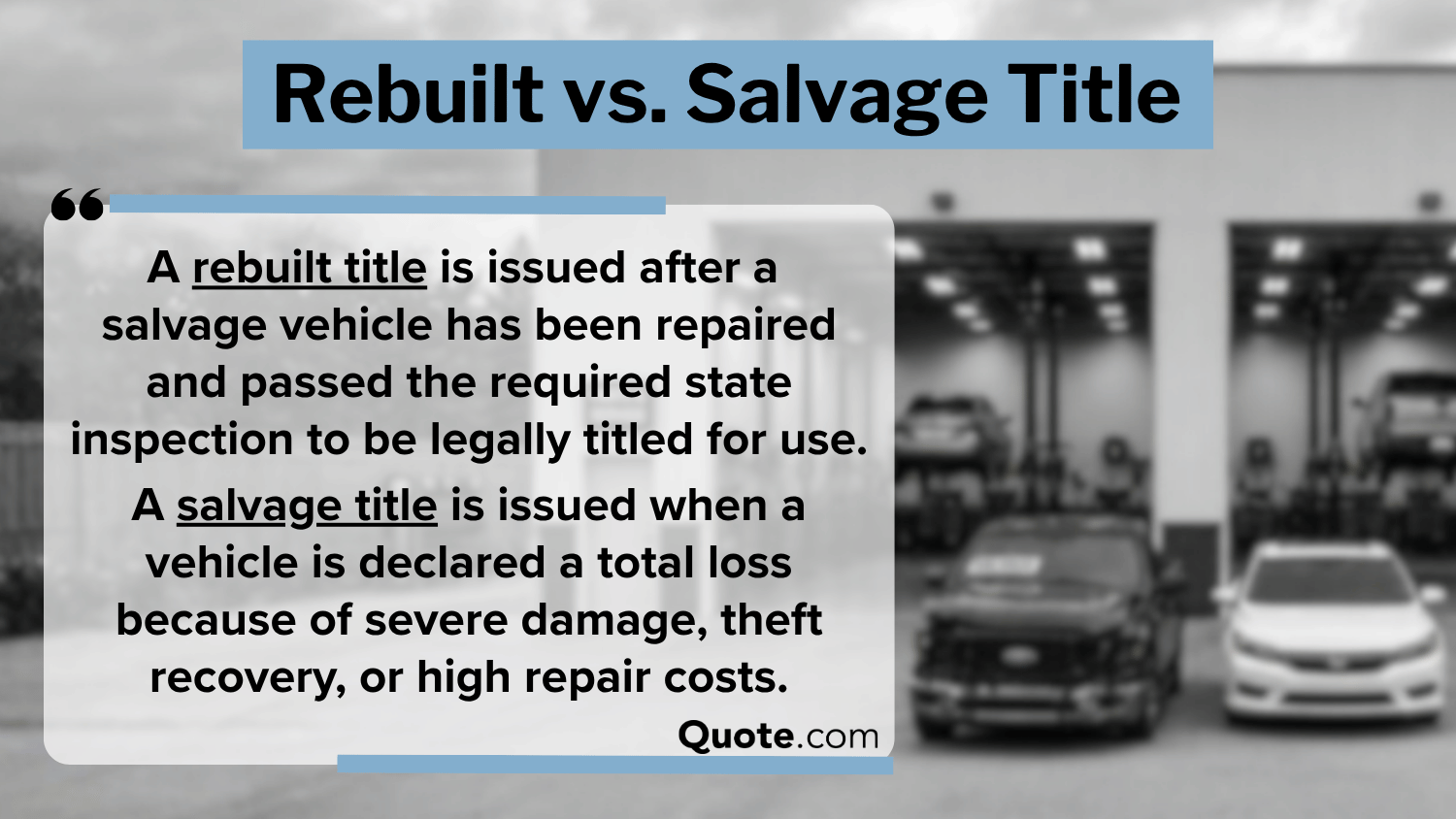

Rebuilt vs. salvage title insurance compares rebuilt vehicles that have been repaired with salvage vehicles declared total losses after 60% to 100% damage in many......

Post

PostRebuilt vs. salvage title insurance compares rebuilt vehicles that have been repaired with salvage vehicles declared total losses after 60% to 100% damage in many......

Post

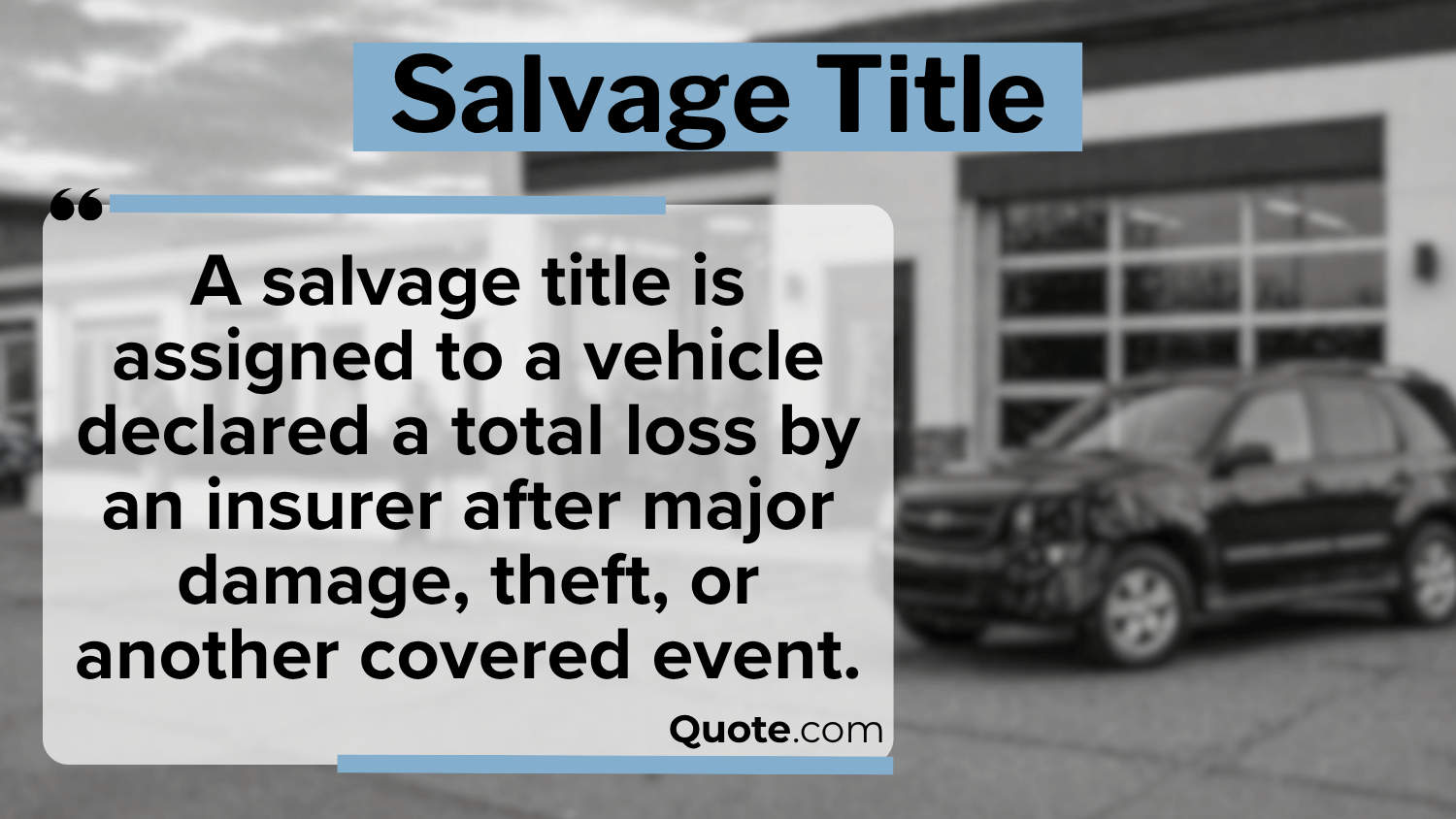

PostVehicles acquire a salvage title after an insurer declares a car a total loss because of a collision, flood, fire, theft, or other serious damage.......

Post

PostThe cheap SR-22 auto insurance are Auto-Owners, Geico, and Erie. Auto-Owners offers the lowest rate at $90 per month after a DUI, while Geico and......

Post

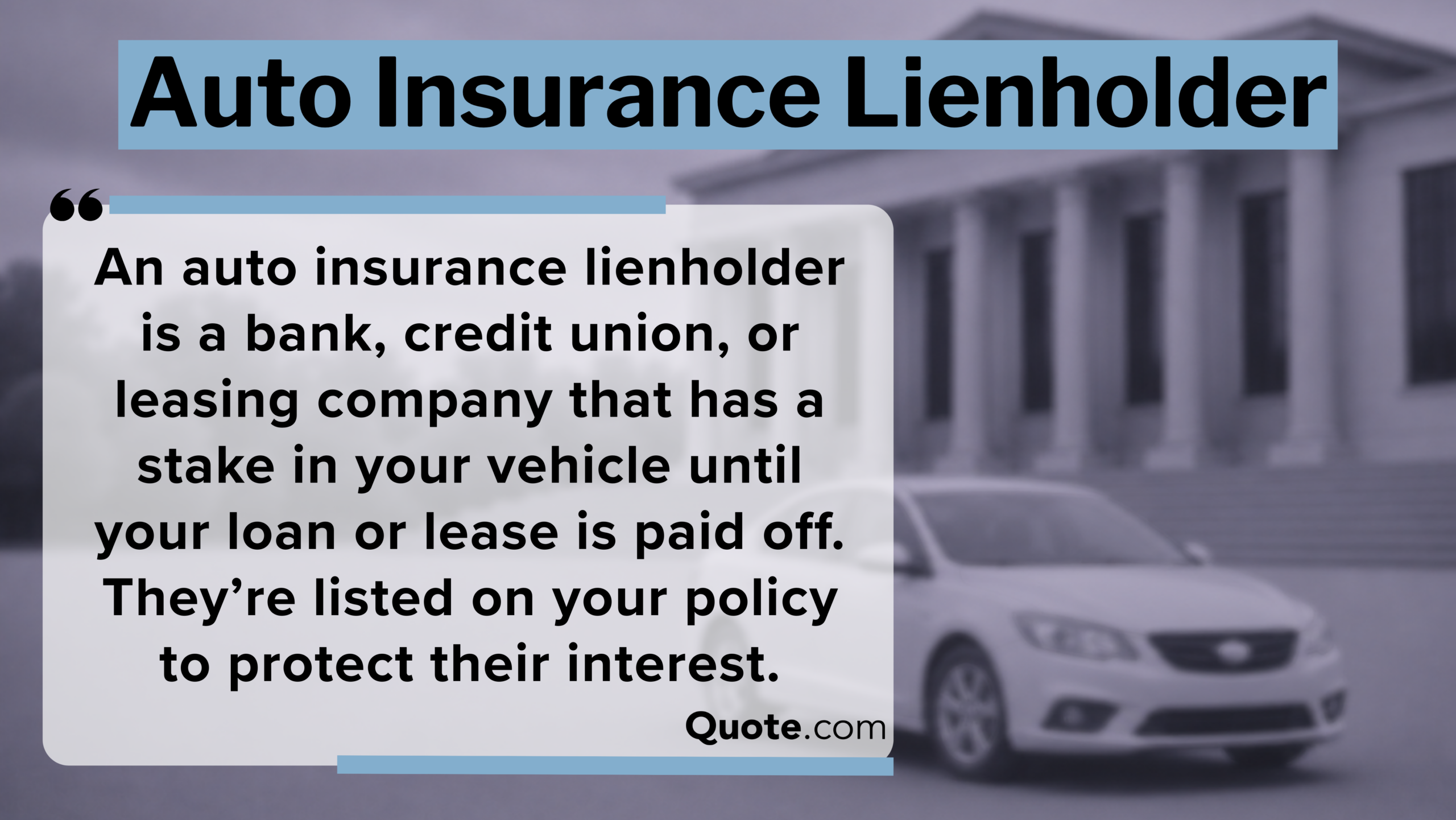

PostAn auto insurance lienholder is the person or company funding your car loan or lease, and their lien remains on your insurance policy until you......

Post

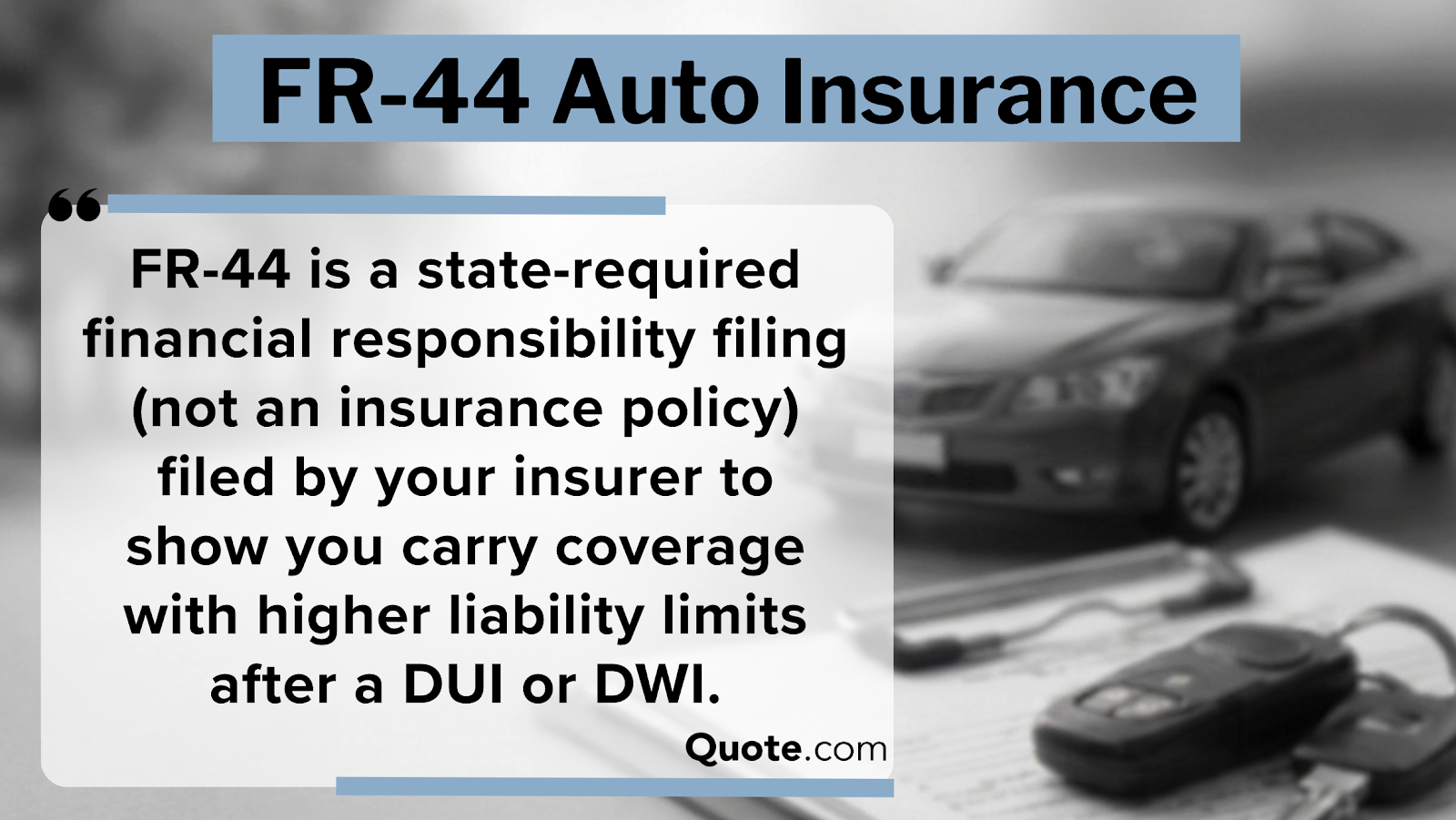

PostFR-44 auto insurance helps drivers with a DUI in Florida and Virginia meet state requirements and get their licenses back by providing 100/300/50 liability coverage.......

Post

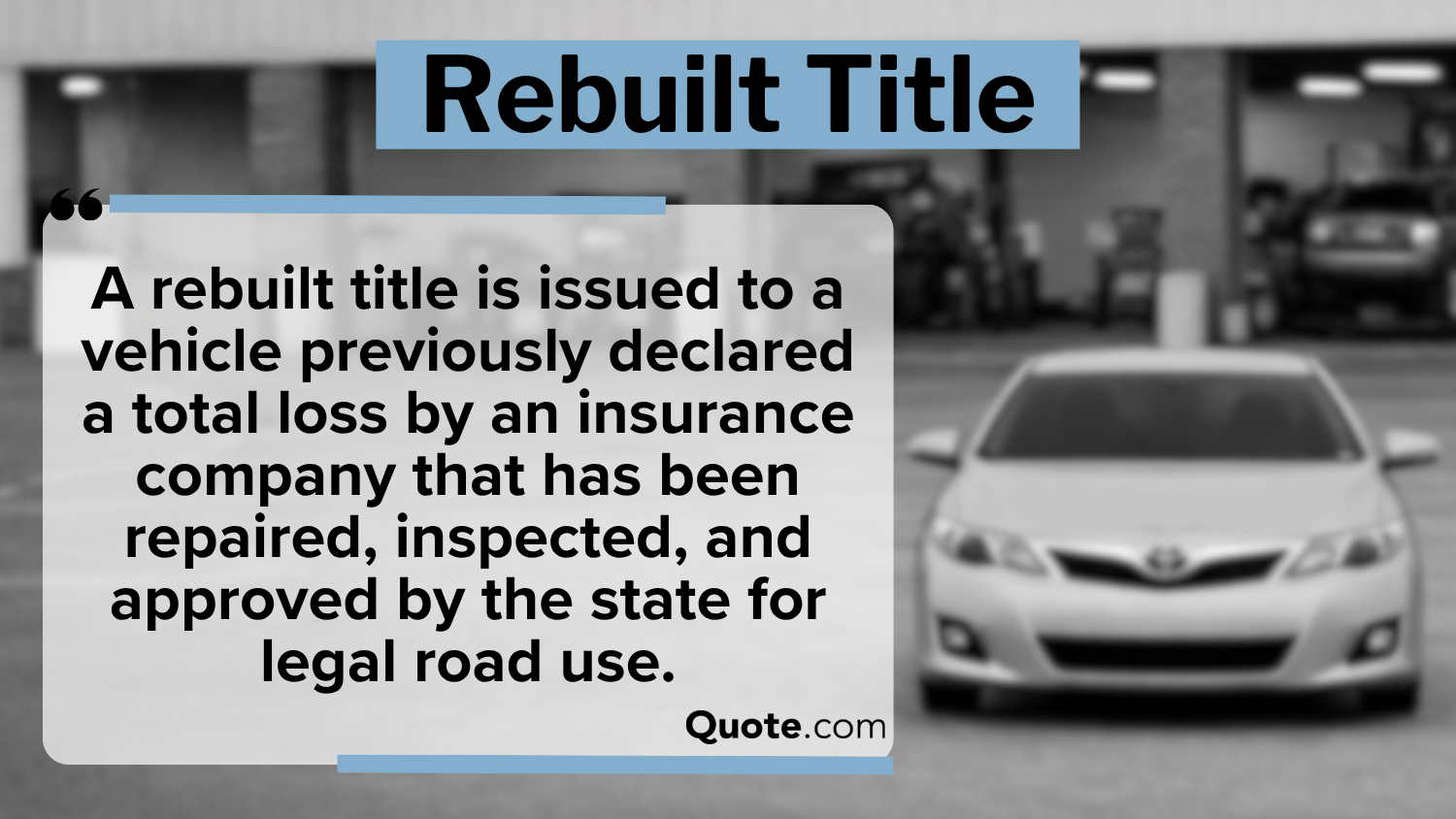

PostHaving a rebuilt title means a vehicle was once declared a total loss but has been repaired and inspected to meet road standards. A rebuilt......

Post

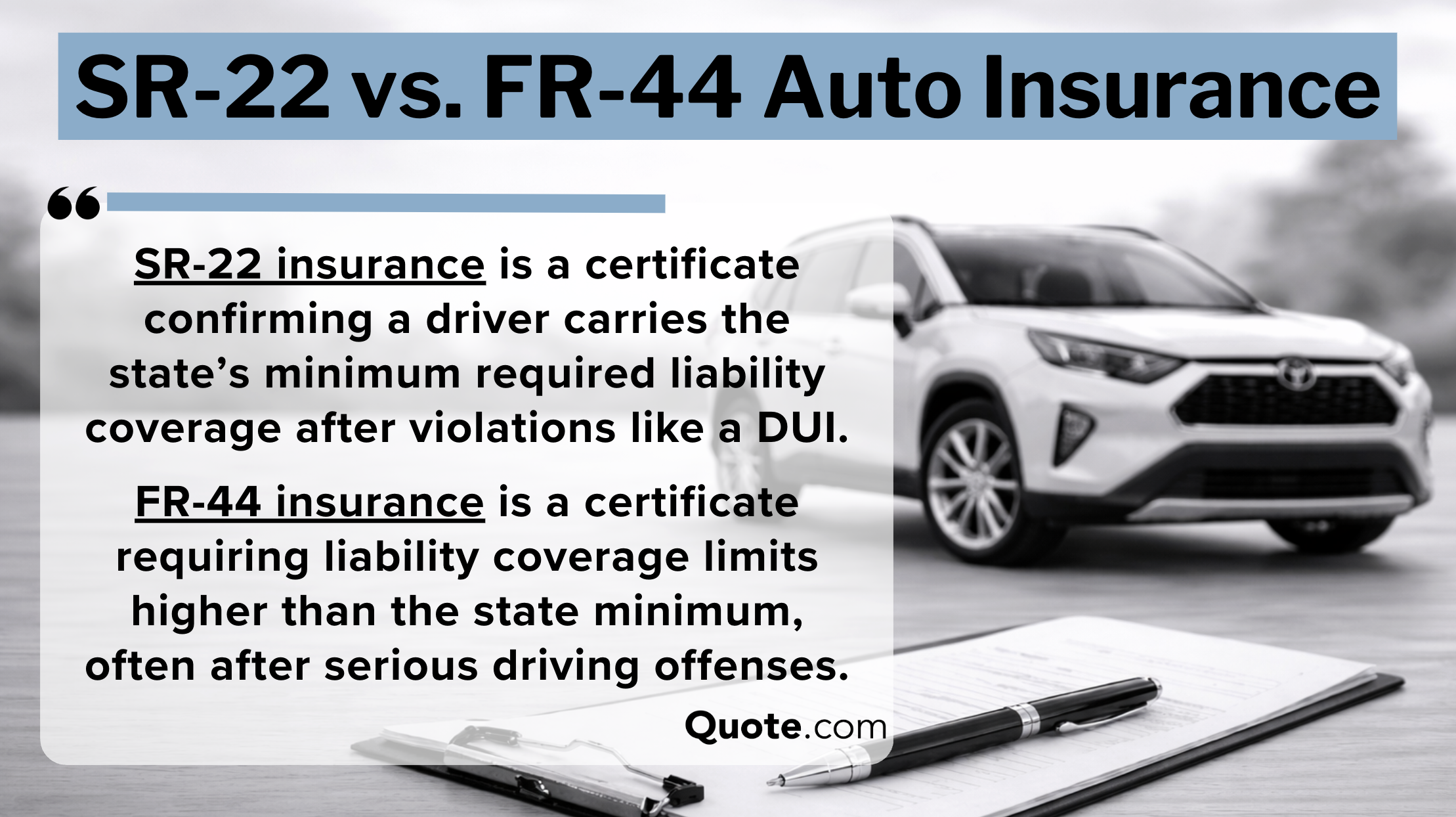

PostThe biggest difference between SR-22 vs. FR-44 auto insurance is that FR-44 certificates raise rates more than SR-22 certificates. Are FR-44 and SR-22 the same?......

Post

PostYour auto insurance premium is the amount you pay every month or every period to keep your coverage active. The average cost of auto insurance......

Post

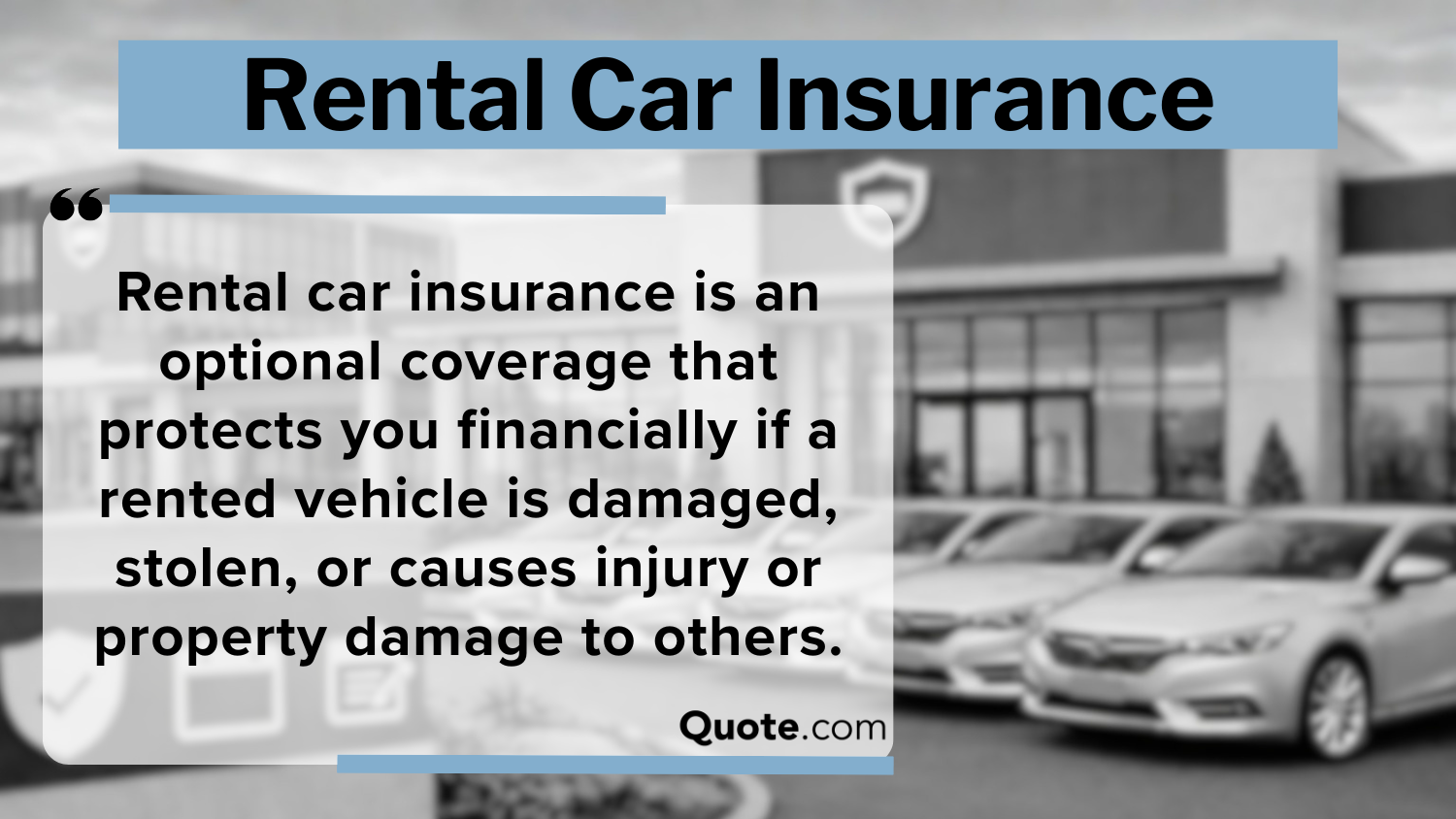

PostRental car insurance helps cover you against damage, theft, and liability when you’re on the road. Dollar prices basic coverage at $9 a day. This......

Post

PostThe American Automobile Association (AAA) offers roadside assistance memberships starting at $9 per month. Services are handled by regional motor clubs that work with AAA. Most members can......

Post

PostErie, USAA, and Liberty Mutual have the best auto insurance for Mercedes. Erie is the #1 company for Mercedes insurance claim satisfaction. Why is Mercedes......

Post

PostMileage affects auto insurance rates by increasing premiums for drivers who log more than 12,000 miles per year. Drivers who are on the road more......

Post

PostErie, USAA, and Liberty Mutual have the best auto insurance for Subarus, with high claims satisfaction and affordable rates. With high safety and crash-test ratings,......

Post

PostErie, USAA, and Liberty Mutual have the best auto insurance for BMWs. Erie has cheap full coverage insurance for BMWs at $165 monthly. BMW vehicles......

Post

PostThe cheapest vehicles to insure are the Honda CR-V, Subaru Forester, and Honda HR-V, with starting rates around $52 per month. These models stand out......

Post

PostAuto accidents affect insurance rates by increasing them for several years, sometimes by as much as 50%. Although an at-fault accident typically affects your premiums......

Post

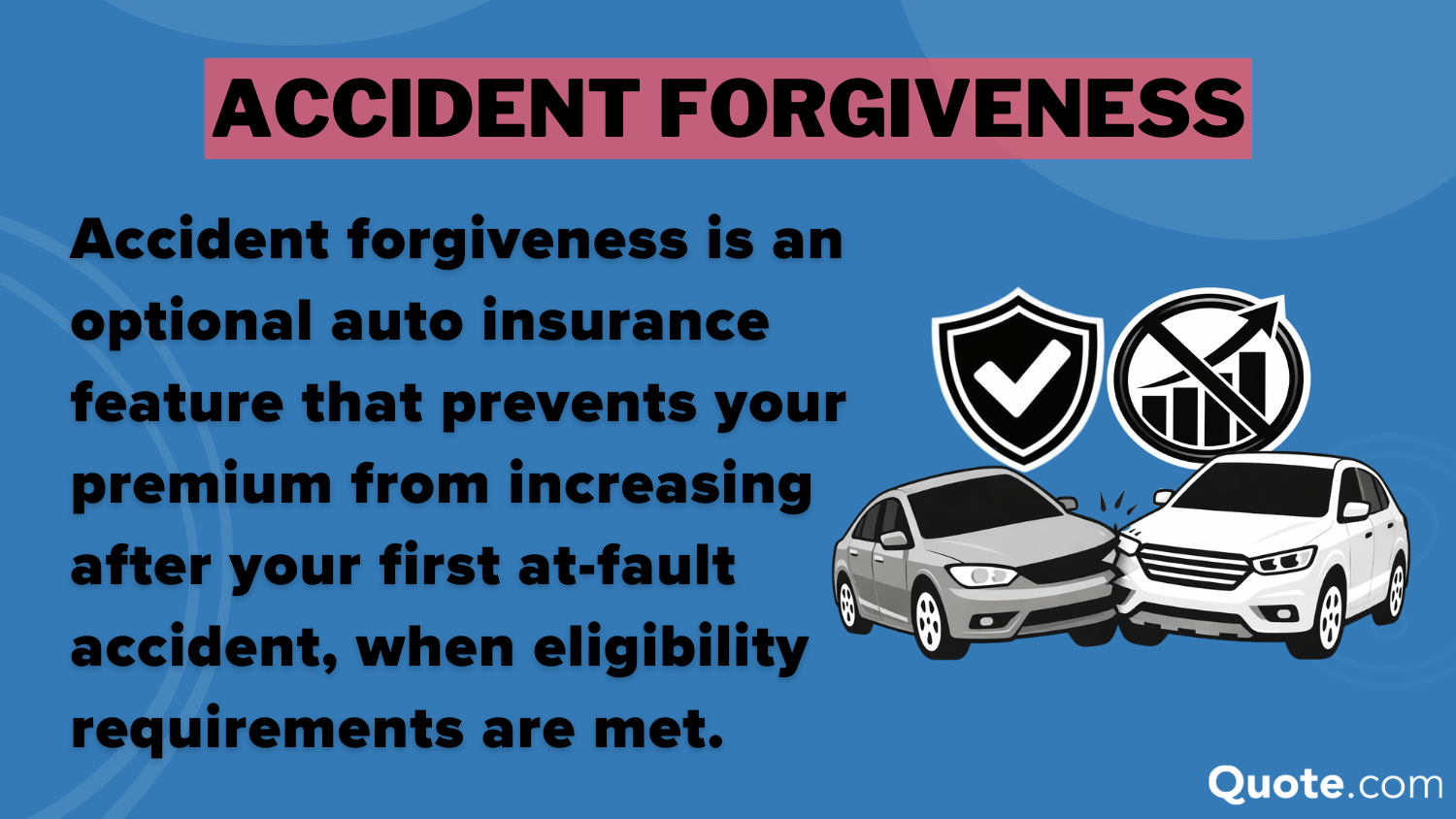

PostIf you have accident forgiveness, your insurer will overlook your first at-fault claim, so that your premium does not increase after a single accident. Accident......

Post

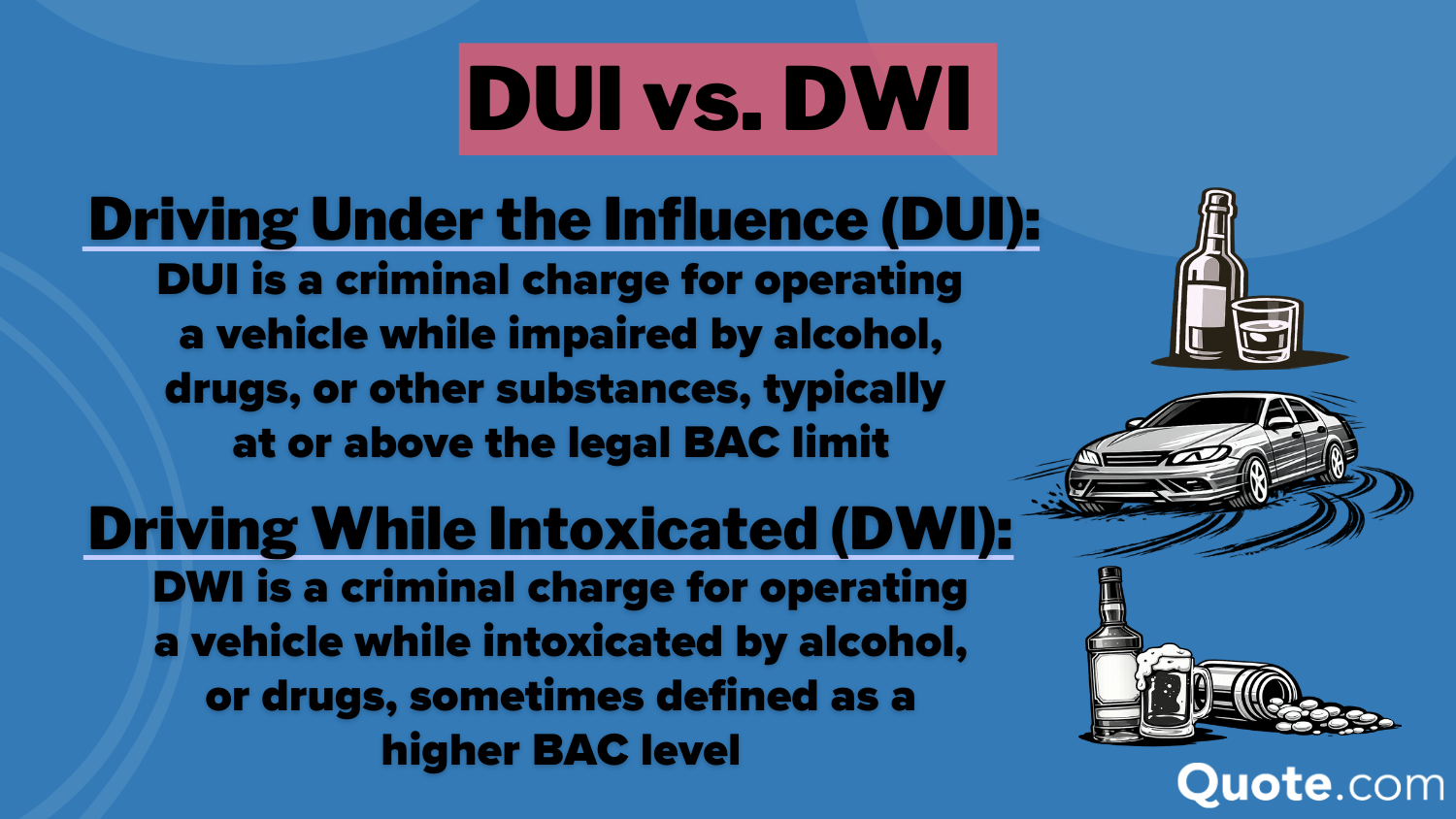

PostDUI vs. DWI both refer to impaired driving, but the exact charge depends on how each state defines the law and blood alcohol content (BAC)......

Post

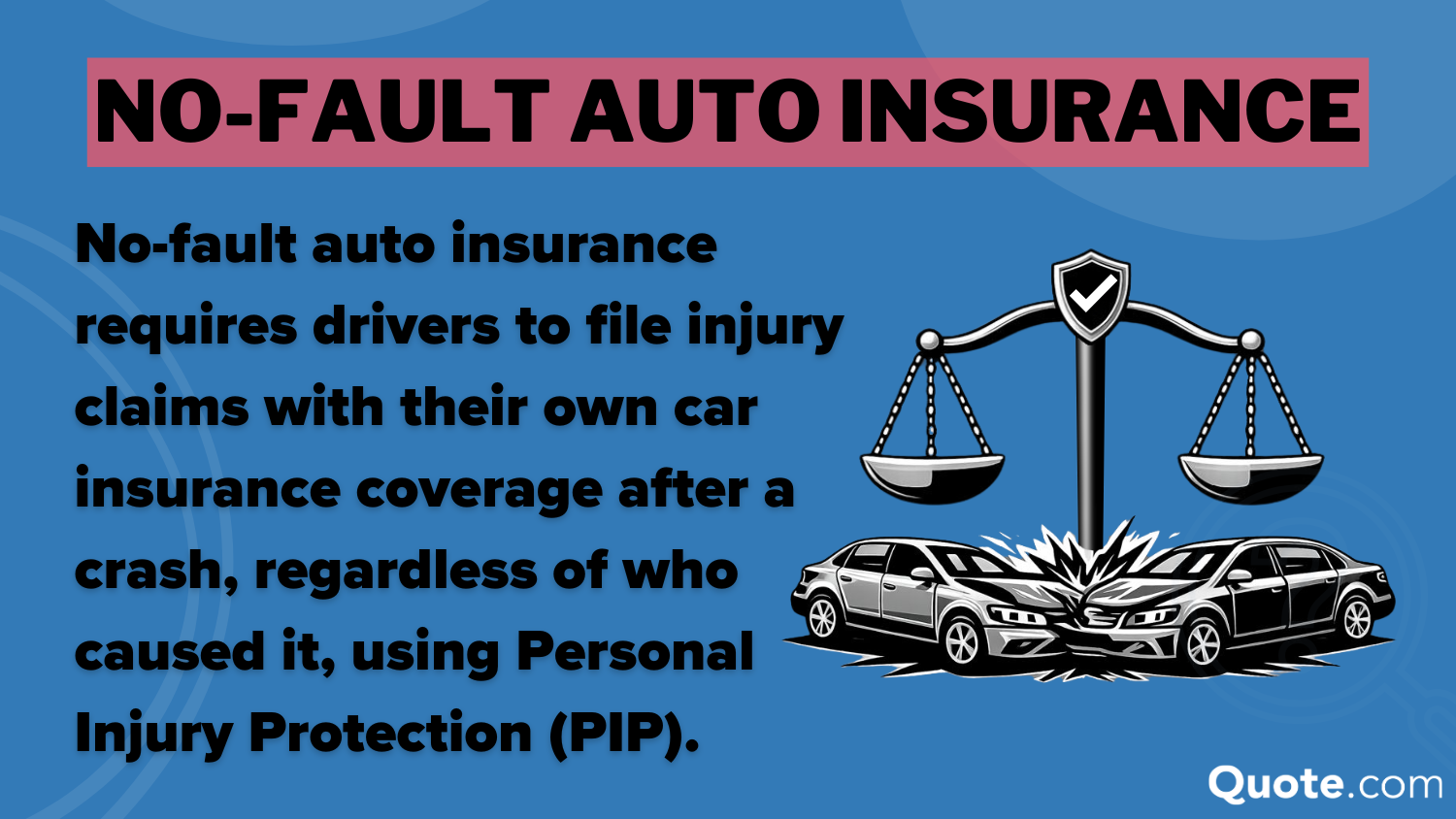

PostNo-fault auto insurance requires you to file injury claims with your own insurer first. Monthly rates for no-fault coverage range from $68 to $221, depending......

Post

PostLiberty Mutual, Progressive, and Farmers have the best auto insurance discounts for seniors. You can save 15% with Liberty Mutual’s senior discount. Liberty Mutual is......

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.

Enter your zip code below to view companies that have cheap insurance rates.