Gap Insurance: How it Works & When You Need it (2026 Rates)

Gap insurance helps pay the difference between your car’s actual cash value and what you owe on a loan or lease if it’s totaled or stolen. While gap insurance prices start at just $168 annually, not every company offers this coverage as an add-on. Gap coverage is ideal for drivers financing or leasing a new car.

Read more

Table of Contents

Table of Contents

Insurance Claims Support & Senior Adjuster

Kalyn grew up in an insurance family with a grandfather, aunt, and uncle leading successful careers as insurance agents. She soon found she had similar interests and followed in their footsteps. After spending about ten years working in the insurance industry as both an appraiser dispatcher and a senior property claims adjuster, she decided to combine her years of insurance experience with another...

Kalyn Johnson

Senior Director of Content

Sara Routhier, Senior Director of Content, has professional experience as an educator, SEO specialist, and content marketer. She has over 10 years of experience in the insurance industry. As a researcher, data nerd, writer, and editor, she strives to curate educational, enlightening articles that provide you with the must-know facts and best-kept secrets within the overwhelming world of insurance....

Sara Routhier

Licensed Insurance Agent

Brad Larson has been in the insurance industry for over 16 years. He specializes in helping clients navigate the claims process, with a particular emphasis on coverage analysis. He received his bachelor’s degree from the University of Utah in Political Science. He also holds an Associate in Claims (AIC) and Associate in General Insurance (AINS) designations, as well as a Utah Property and Casual...

Brad Larson

Updated June 2026

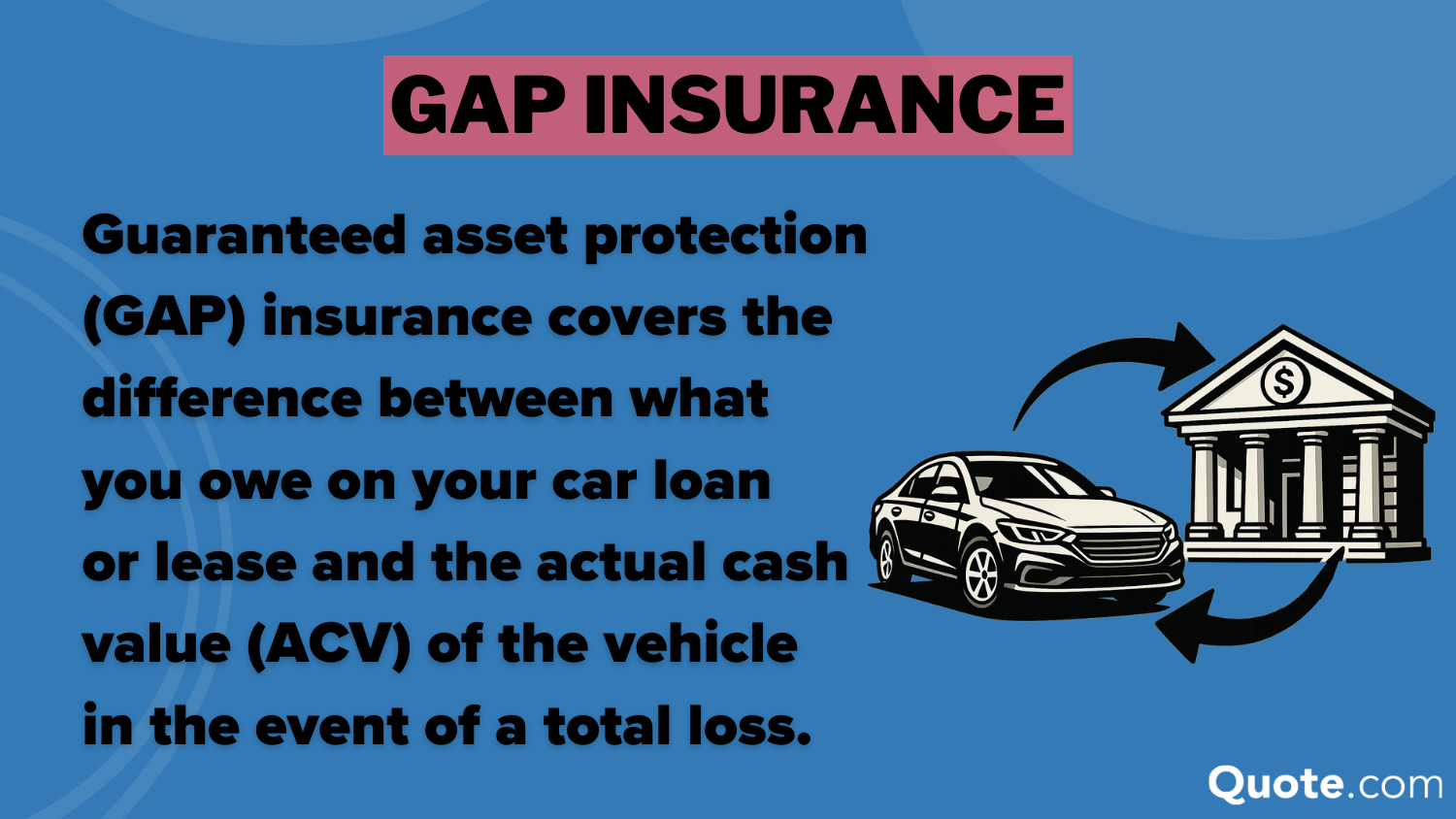

Gap insurance, short for “guaranteed asset protection,” is an optional auto insurance add-on that protects you financially if your car is totaled. Costs range from $14 to $23 a month.

- Gap insurance pays the difference on an underwater loan

- Vehicles typically must be three years old or newer to qualify for coverage

- Full coverage with gap insurance costs as low as $126 a month

If your vehicle is declared a total loss, gap insurance helps cover the difference between your car’s actual cash value and the remaining balance on your loan or lease.

This coverage is most useful for drivers who finance or lease a new vehicle. Cars lose value quickly, which means you may owe more on your loan than the vehicle is worth, especially during the first few years of ownership.

Learn how to buy auto insurance with gap coverage and whether it’s the right choice for your policy in our guide. Then, enter your ZIP code into our free comparison tool to see the lowest rates in your area.

What is Gap Insurance and How Does it Work?

Gap insurance explained simply is an optional auto insurance coverage that helps pay the difference between what you still owe on your car loan or lease and your vehicle’s current value if it’s totaled or stolen.

When a vehicle is declared a total loss, standard auto insurance typically pays only what the car is worth at the time of the loss. You can then file a gap insurance claim to help cover the remaining balance on your loan or lease.

Even if you know how to file an auto insurance claim and win each time, the payout will usually be less than what you originally paid for the vehicle.

To understand the meaning of gap insurance, it helps to know how car depreciation and loan balances work.

New cars depreciate quickly, often by 20% or more in the first year. Since auto loans usually pay down more slowly than vehicles lose value, drivers can end up with negative equity, meaning the loan balance is higher than the car’s value.

This type of coverage usually works alongside your collision and comprehensive insurance, which must be active for gap insurance to apply after a covered loss.

How Gap Insurance Pays After a Total Loss| Scenario | Loan Balance | ACV Payout | Gap Pays |

|---|---|---|---|

| Leased Vehicle | $33K | $30.5K | $2.5K |

| Long-Term Loan | $36K | $29K | $7K |

| Low Down Payment | $31K | $23.5K | $7.5K |

| New Car (Year 1) | $34K | $26K | $8K |

For example, if you owe $25,000 on your loan but your car’s actual cash value (ACV) is only $20,000 at the time of a total loss, gap insurance would help cover the $5,000 difference. This keeps you from having to pay out of pocket for a car you no longer have.

Many lenders have gap insurance requirements for leasing a car, since the vehicle’s value can depreciate quickly during the lease term. Gap auto coverage protects the lender if the car is totaled while the loan balance is still higher than the vehicle’s value.

Gap insurance is beneficial for drivers who have a long-term loan, lease their vehicle, or have made a small down payment on their car.

Michelle Robbins Licensed Insurance Agent

Gap insurance typically applies only to new or relatively new vehicles, and most insurance companies require that you add the coverage within a short window after purchasing or leasing the car.

If your loan or lease doesn’t include coverage, you can usually add it to your existing policy with insurance companies that offer gap insurance.

When Gap Insurance Is Worth It

Gap insurance helps if your car is stolen or totaled and you owe more than the vehicle is worth. Standard auto insurance usually pays only the car’s current market value. Gap insurance covers the difference between that payout and the remaining balance on your loan or lease.

This coverage can be especially helpful if you financed a car with a small down payment. When you put little money down, you may owe more than the vehicle’s value early in the loan. The same can happen if you choose a long loan term, since it takes longer to build equity.

Drivers Who Should Consider Gap Insurance| Situation | Gap Risk | Recommended? | Reason |

|---|---|---|---|

| Large Down Payment | Low | ❌ | Equity lowers gap risk |

| Long Loan Term | High | ✅ | Loan payoff is slower |

| Low Down Payment | High | ✅ | Loan may exceed value |

| Paid in Cash | None | ❌ | No loan balance exists |

| Vehicle Lease | Medium | ✅ | Often required by lease |

Gap insurance may also be worth considering if you rolled negative equity from a previous auto loan into a new one. In that case, you may start the loan already owing more than the car’s value.

It may also make sense if you drive many miles each year. Higher mileage can lower a vehicle’s value faster, which increases the chance that your loan or lease balance could exceed what the car is worth.

While it isn’t the right choice for every driver, gap insurance can save you thousands of dollars if you owe more on your loan than the car is worth. Gap policies are most common for drivers with an auto loan, but it can also be valuable for people leasing a vehicle.

Additionally, not every company sells gap insurance. Reviewing a gap insurance quote comparison can help you find insurers that offer this coverage and how their prices stack up.

Gap Insurance Company Requirements

While gap insurance can be valuable for some drivers, not every vehicle qualifies for coverage. Most insurers only offer gap insurance for cars that are three model years old or newer. Many companies also set a maximum mileage limit.

In addition, drivers typically must add auto insurance gap protection within 30 days of buying a new vehicle. After that window closes, most gap insurance providers won’t allow the coverage to be added.

Gap Insurance Coverage Limits and Policy Details| Company | Limits | Requirement | Term | Benefits |

|---|---|---|---|---|

| $50K | Loan/Lease | 6 yrs | Gap Waiver | |

| $30K | Full Coverage | 5 yrs | Flexible Terms | |

| $50K | Comprehensive | 5 yrs | Flexible Limits | |

| $30K | Loan/Lease | 6 yrs | Loan Payoff | |

| $75K | Vehicle ≤ 4 yrs | 5 yrs | Policy Add-Ons | |

| $30K | Loan/Lease | 6 yrs | Value Cap | |

| $100K | Loan/Lease | 5 yrs | Dealer Access | |

| $100K | Nearly-New Car | 5 yrs | Dealer Purchase | |

| $100K | Military/Veteran | 5 yrs | Military Savings |

As you can see, some of the top insurance companies are missing from the list. For example, many drivers wonder, “Does Geico offer loan lease payoff?” No, Geico doesn’t sell gap insurance, so drivers won’t find a Geico gap insurance cost to compare with other insurers.

That’s why it’s important to compare multiple insurance companies when you’re shopping for loan/lease payoff coverage.

Free Auto Insurance Comparison

Compare Quotes From Top Companies and Save

What Gap Insurance Doesn’t Cover

While gap insurance can be a financial lifesaver in certain situations, it doesn’t cover everything. Before you purchase gap coverage, make sure you understand what it doesn’t cover:

- Car Repairs or Maintenance: Gap insurance only applies if your vehicle is totaled or stolen. It won’t cover mechanical repairs, breakdowns, or routine maintenance costs.

- Deductibles: Some gap policies don’t cover your auto insurance deductible, although a few may offer limited help.

- Late or Missed Payments: Overdue payments, interest charges, or late fees on your loan or lease usually aren’t covered.

- New Vehicle Replacement: Gap insurance covers the financial gap between your loan balance and the car’s actual cash value. It doesn’t pay for a brand-new replacement.

- Negative Equity From a Trade-In: If you rolled negative equity from a previous loan into your current loan, that extra balance usually isn’t covered.

Always read your gap policy carefully and ask your insurer about specifics to make sure you’re fully protected in the event of a loss.

Read More: What to Do if You Can’t Afford Your Auto Insurance

Where You Can Get Gap Insurance

You can buy gap insurance from several places, including your auto insurance company, a dealership, or the lender financing your vehicle.

Each option works a little differently and can vary in cost, convenience, and eligibility requirements.

Where you buy gap insurance can also affect how you pay for the coverage. Some providers charge a one-time fee that’s added to your loan, while others offer gap coverage as a small monthly add-on to your auto insurance policy.

Pricing and eligibility vary by provider, so it’s smart to compare gap insurance options before purchasing coverage and choose the one that best fits your lender, insurer, and preferred payment structure.

🚗Dealership

Many dealerships offer gap insurance when you finance a vehicle through their in-house financing or a partner lender. This option is convenient because it’s added to your auto loan during the purchase process. Related: How to Buy Insurance for a New Vehicle

However, dealership gap insurance is usually the most expensive option. The cost is often rolled into your loan, which means you may also pay interest on the coverage over time.

Gap insurance is often offered alongside other optional dealership add-ons, such as extended warranties or credit insurance. If the coverage is rolled into your auto loan, it increases the total amount financed and may raise the interest you pay over time.

🛡️Auto Insurance Company

Many top car insurance providers offer gap insurance as an add-on to a full coverage auto insurance policy. In most cases, this is the most affordable way to get gap coverage.

Adding gap insurance to your existing policy also makes it easier to manage your coverage and billing in one place. Availability may depend on your insurer and whether your vehicle meets eligibility requirements, such as being new or recently financed.

🏦Banks and Credit Unions

If you finance your vehicle through a bank or credit union, the lender may offer gap insurance when you take out the loan. Credit unions, in particular, often provide some of the cheapest gap insurance options available.

In many cases, coverage is offered as a one-time fee added to the loan or paid upfront, making it a cost-effective alternative to dealership gap insurance.

Cost of Gap Insurance Coverage

Gap insurance is typically one of the least expensive auto coverage add-ons and offers affordable protection against negative equity. Rates vary by insurer, but most companies charge a flat monthly add-on fee rather than calculating premiums based heavily on driving history.

When reviewing a gap insurance quote, you’ll usually see this cost listed as a small monthly fee added to your existing policy. The average cost of gap insurance from a standard auto insurer ranges from $14 to $23 per month.

Gap Insurance Monthly Rates by Provider| Insurance Company | Gap Only | Full Coverage + Gap |

|---|---|---|

| $20 | $195 | |

| $18 | $175 | |

| $21 | $193 | |

| $17 | $203 | |

| $19 | $170 | |

| $16 | $182 | |

| $22 | $155 | |

| $23 | $183 | |

| $14 | $126 |

Dealership gap insurance typically costs between $400 and $700 as a one-time fee. In many cases, that price is much higher than what you’d pay by adding gap coverage to your car insurance policy.

When you purchase gap insurance through a dealership, it’s usually added to your auto loan. This increases the total amount you’re financing, which means you’ll also pay interest on that added cost over time.

You’ll likely need to buy a full coverage policy if you want to add gap insurance. Full coverage consists of liability, comprehensive, and collision insurance.

Jeff Root Licensed Insurance Agent

While gap coverage is generally affordable, you should only purchase gap insurance if you actually need it, especially if you’re looking for the cheapest auto insurance possible.

Like all types of auto insurance, you’ll need to compare rates to find the best gap insurance prices for you. Looking at multiple gap insurance quotes can help you understand typical pricing and what coverage limits different insurers offer.

If you’re ready to find cheap gap insurance, enter your ZIP code into our free comparison tool now.

Free Auto Insurance Comparison

Compare Quotes From Top Companies and Save

When to Drop Gap Insurance

Gap insurance is most valuable during the early years of a car loan or lease, but you won’t need it forever.

Consider dropping gap coverage when:

- You Owe Less Than the Car’s Value: Once your loan balance is equal to or less than your vehicle’s ACV, there’s no “gap” left to insure.

- You Refinanced Your Vehicle: Gap coverage doesn’t always carry over to refinanced loans, so check with your insurer. If you have equity in the car, you may not need it at all.

- You’re Near the End of Your Loan: As your car loan matures and you build equity, the risk of being upside down on your loan decreases.

- You’ve Paid Off the Loan: If you own the car outright, gap insurance no longer serves a purpose.

Longer auto loan terms increase the risk of negative equity since vehicles often depreciate faster than the loan balance declines. Drivers with 60- to 84-month auto loans are much more likely to owe more than their car is worth during the first few years of ownership.

Shorter loan terms reduce this risk because the loan balance is paid down more quickly.

Although gap insurance is typically inexpensive, knowing when to cancel it can help reduce your insurance costs. In fact, keeping coverage you no longer need is one of the top ways drivers are wasting money on their car insurance.

Review your finances and coverage limits annually to ensure you’re not paying for insurance you no longer need. If you need help, a representative from your company should be able to walk you through your coverage.

You can also have a representative verify that you’re receiving all the auto insurance discounts you qualify for, ensuring maximum savings.

Alternatives to Gap Insurance

Gap insurance may be one of the best options to protect you when you have a car loan or lease, but it’s not the only thing on the market. Consider the following add-ons as alternatives to gap insurance:

- New Car Replacement: This add-on pays for a replacement vehicle of the same make and model as your totaled car, rather than just paying for its ACV.

- Better Car Replacement: Some insurance providers offer better car replacement coverage, which replaces your totaled vehicle with a newer model.

- Loan/Lease Payoff: Loan/lease payoff is similar to gap insurance, but it usually only pays a percentage of your car’s ACV.

Most standard auto insurance policies only reimburse drivers for a vehicle’s actual cash value after a total loss, which may be less than what you paid for the car.

These alternatives are a great way to find the coverage you want, especially if you have a policy from a company that doesn’t offer gap coverage.

Read More: How to Lease a Car When You Can’t Afford to Buy One

How to Check if You Have Gap Insurance

If you’re not sure whether you have gap insurance, there are a few easy ways to find out. Knowing whether you’re covered can prevent surprises if your car is ever totaled or stolen.

- Review Loan Paperwork: Many dealerships include automobile gap insurance in lease agreements or as part of financing packages.

- Check Your Insurance Policy: Review the declarations page in your policy or contact your insurance company to ask if it’s included.

- Contact the Lender: If you financed or leased your vehicle through a bank or dealership, they can confirm if gap insurance was included and who provides it.

If you recently purchased your vehicle, the finance or insurance paperwork from the dealership is often the quickest place to confirm whether gap coverage was included.

Many drivers don’t realize they may already have gap coverage through their lender or dealership. Before buying coverage, review your loan and auto insurance policy. A quick check can help you avoid paying for duplicate protection.

Scott Young Managing Editor

If you plan to finance a new car soon, you can also ask the dealership whether gap insurance will be part of your loan or lease agreement.

Additionally, some policies ask if you want gap insurance when you buy it. For example, the best auto insurance for luxury and exotic vehicles often includes gap protection insurance to cover the larger loans associated with these cars.

Free Auto Insurance Comparison

Compare Quotes From Top Companies and Save

Find the Best Gap Insurance Today

Whether you have a car loan or lease, gap insurance can protect you from having to pay for a vehicle you no longer own.

It’s not right for everyone, but gap coverage insurance could save you thousands of dollars in the right circumstances.

Since some companies don’t offer gap insurance, a gap insurance price comparison can help you quickly identify which insurers provide this coverage and how their prices differ. Learn More: How to Get Multiple Auto Insurance Quotes

To search for auto insurance companies that offer gap coverage, enter your ZIP code into our free comparison tool today.

Frequently Asked Questions

What does gap insurance actually cover?

Gap insurance pays the difference between what you owe on your car loan or lease and the vehicle’s actual cash value (ACV) if it’s totaled or stolen.

It’s most helpful early in a loan, when a car’s value depreciates faster than the loan balance. Gap insurance helps prevent you from paying out of pocket for a vehicle you no longer have.

Are gap insurance and loan/lease payoff coverage the same?

Gap insurance and loan/lease payoff coverage are similar, but there’s an important difference. Gap insurance typically covers the full difference between what you owe and your vehicle’s actual cash value if it’s totaled.

Loan/lease payoff coverage usually pays a percentage of your vehicle’s value, often around 25%, which may not cover the entire gap.

When does gap insurance not pay?

Gap insurance doesn’t pay unless your car is declared a total loss or stolen. It also doesn’t cover repairs, maintenance, or normal depreciation. Late loan payments, overdue fees, and negative equity from a previous loan rolled into your current loan are typically not covered.

Do I need gap insurance if I have full coverage?

Full coverage usually includes liability, collision, and comprehensive auto insurance, but doesn’t typically include gap coverage. If you have an underwater loan on your vehicle, you’ll most likely need to add gap coverage to your policy.

To find out how much gap coverage may cost and which insurers offer it, compare quotes and coverage options from multiple providers.

How much money do you get back from gap insurance?

Gap insurance helps pay the remaining loan balance that’s left after your car’s value is paid out in a total loss or theft. The payment generally goes to your lender. Keep in mind that some policies don’t include your deductible or any extra negative equity financed into the loan.

Why didn’t gap insurance pay off my car?

Gap insurance may not pay off your entire loan if the policy excludes certain costs or limits how much it will cover. For example, many policies don’t cover your deductible, missed payments, late fees, or negative equity rolled into the loan. It only pays the loan or lease payoff difference between your car’s value and the remaining balance.

Is it worth having gap insurance?

It depends on your situation. If you’ve recently purchased or leased a car, buying gap insurance might be worth it. While there are several factors to look at, you should purchase gap insurance during times when you owe more on your vehicle than it’s worth.

How much is gap insurance per month?

On average, gap insurance rates range from $14 to $23 per month, but it depends on several factors, including where you buy it, what type of car you drive, and how large your loan is.

A gap insurance cost comparison can also help you see how prices differ between insurers and providers. To see how much you might pay, enter your ZIP code into our free comparison tool today.

Can you buy standalone gap insurance?

Yes. You can often buy gap coverage through a dealership or lender when you finance or lease a car, usually as part of the loan or lease paperwork. You may also be able to add gap coverage to your existing auto insurance policy as an optional add-on if you have full coverage.

Some standalone gap insurance companies also offer this coverage directly. Gap insurance companies like EasyCare, Safe-Guard Products, AUL Corp, and GAP Direct specialize in gap protection that’s separate from traditional auto insurance policies.

Can gap insurance be added after buying a car?

Yes, you can often add gap insurance after you purchase a car, but only within a limited time. Many insurers require you to add it within the first few months of the loan or lease, and the vehicle usually must meet certain age and mileage limits.

Can you be denied gap insurance?

What insurance companies offer gap insurance?

Who sells the best gap insurance?

Who has the cheapest gap insurance?

Does Geico offer gap insurance?

Does Progressive have gap insurance?

Related Articles

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.