Post

PostBest Final Expense Life Insurance in 2026

The best final expense life insurance comes from Mutual of Omaha, Nationwide, and Guardian, with rates starting at $17 per month. Final expense life insurance......

Post

PostThe best final expense life insurance comes from Mutual of Omaha, Nationwide, and Guardian, with rates starting at $17 per month. Final expense life insurance......

Post

PostGuardian, MassMutual, and Northwestern Mutual have the best life insurance for children starting at just $3 a month, offering plans with cash value growth and......

Post

PostState Farm has the best life insurance for veterans, with its guaranteed annual cash value growth for military retirees. Protective Life offers the most affordable......

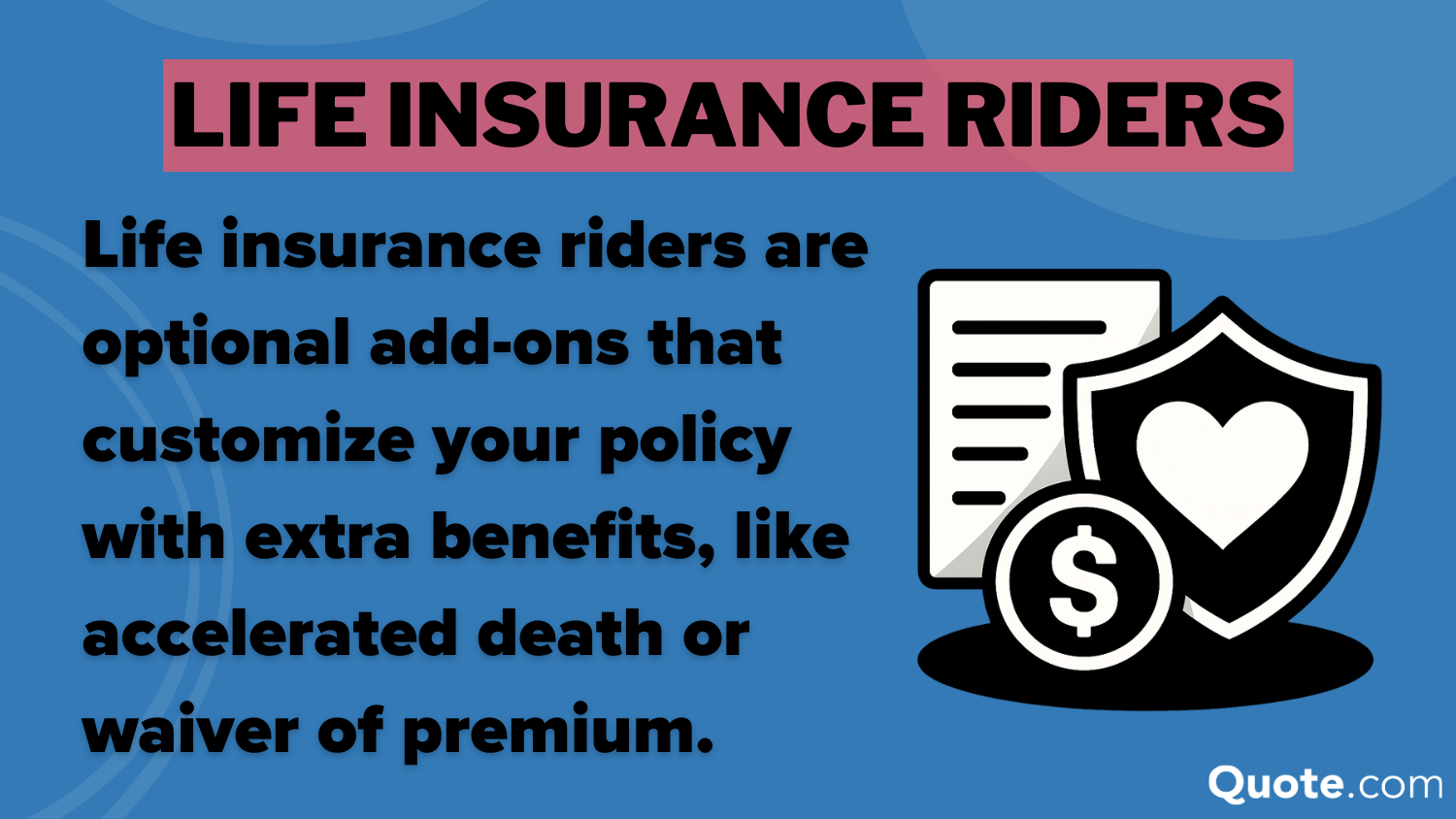

Post

PostLife insurance riders attach additional protections to a term or whole policy. Popular types of riders in insurance include living benefits, accidental death payouts, and......

Post

PostThe leading providers for the best life insurance for seniors are Aflac, Fidelity Life, and Liberty Mutual, with term plans starting around $80 a month......

Post

PostFidelity Life, State Farm, and Nationwide offer the best life insurance for young adults. Fidelity Life skips medical exams for qualified applicants through its RAPIDecision......

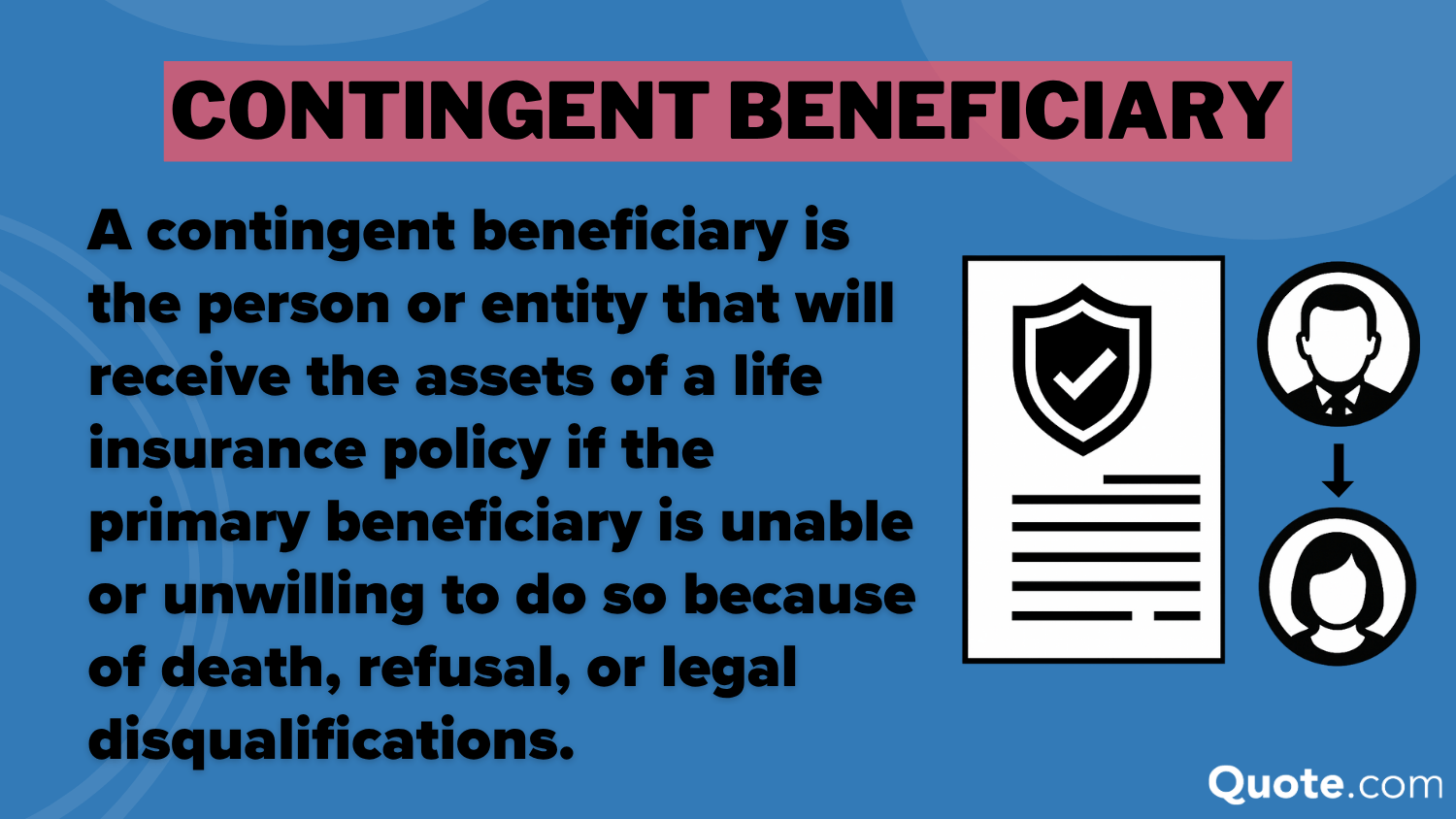

Post

PostIf your primary beneficiary is unable to receive life insurance benefits as stated in your policy, you can designate a contingent beneficiary to receive assets.......

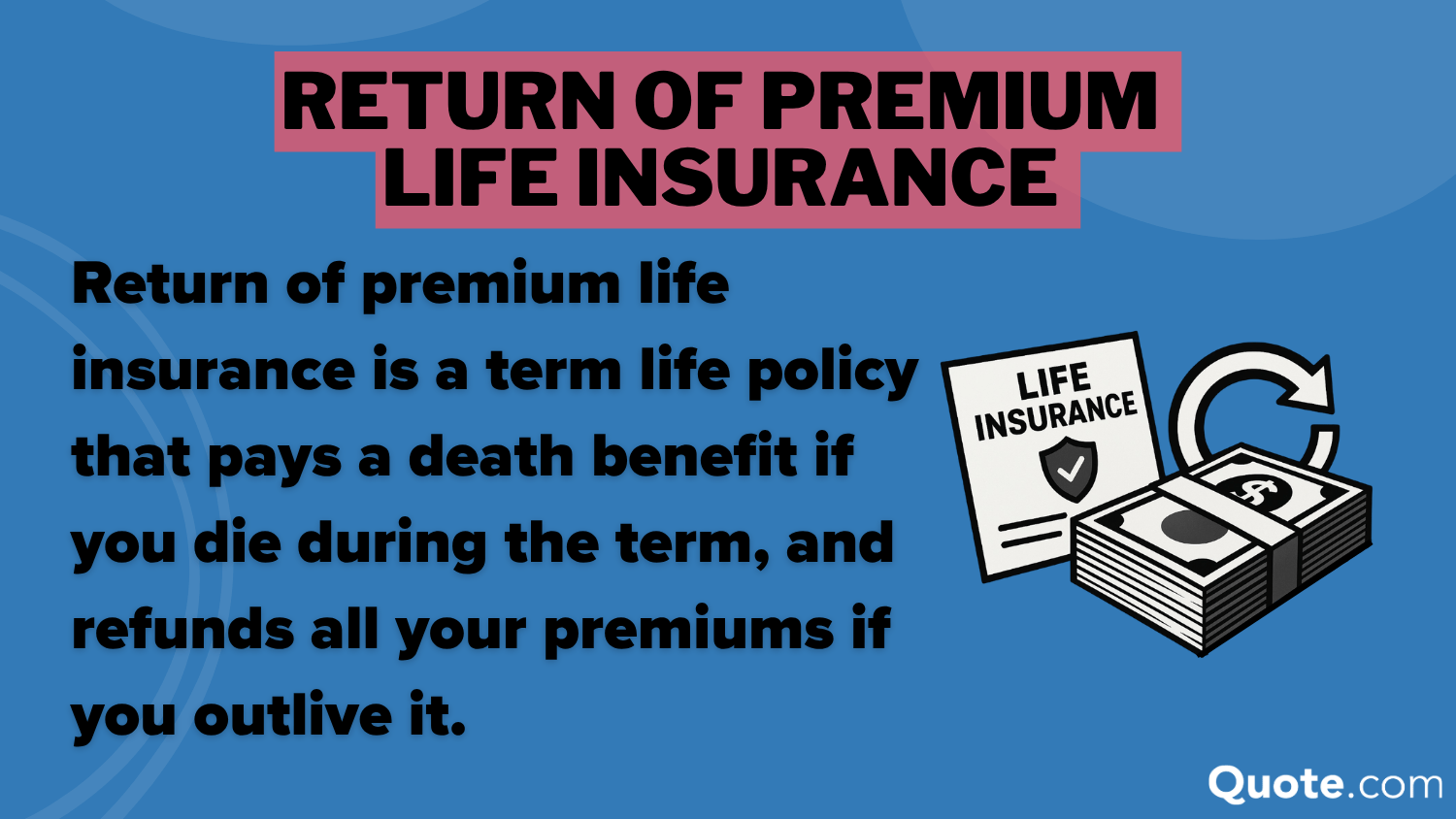

Post

PostIf you have term life insurance and outlive your policy, return of premium (ROP) life insurance riders refund every premium you paid. Unlike traditional term......

Post

PostState Farm, MassMutual, and Nationwide have the best no-exam life insurance options that eliminate medical testing for faster approval. State Farm uses accelerated underwriting to......

Post

PostThe best term life insurance companies are State Farm, MassMutual, and Nationwide. State Farm stands out as the overall top pick thanks to its 699/1,000......

Post

PostIf you’re looking for the cheapest life insurance companies, Liberty Mutual, AAA, and Nationwide stand out with rates starting around $24 per month. Liberty Mutual......

Post

PostThe top providers for the best instant life insurance are State Farm, Mutual of Omaha, and Erie, because of their proven strength in fast approvals......

Post

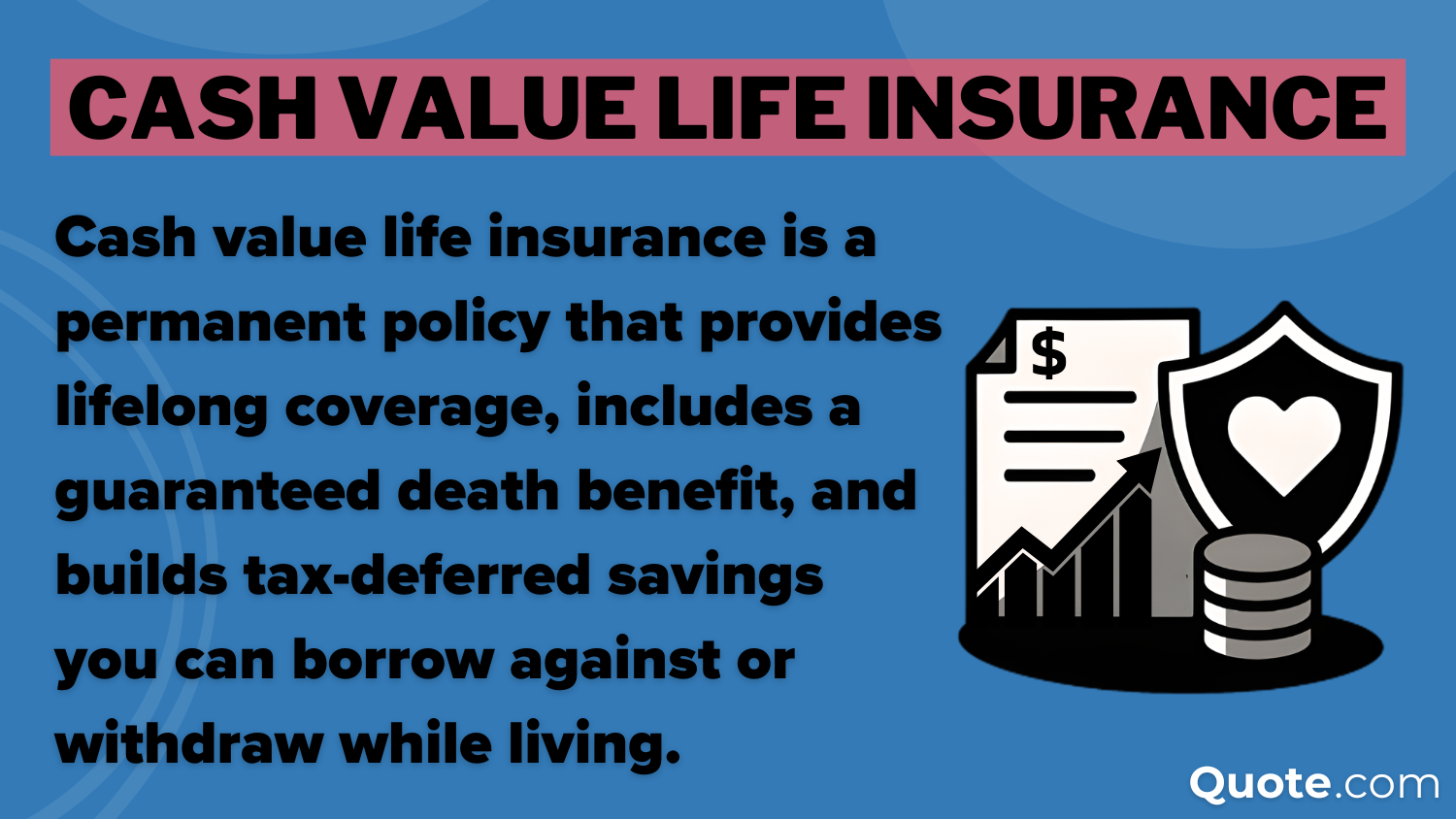

PostCash value life insurance provides permanent coverage and includes a built-in savings account that grows through interest or investments. As long as you pay your......

Post

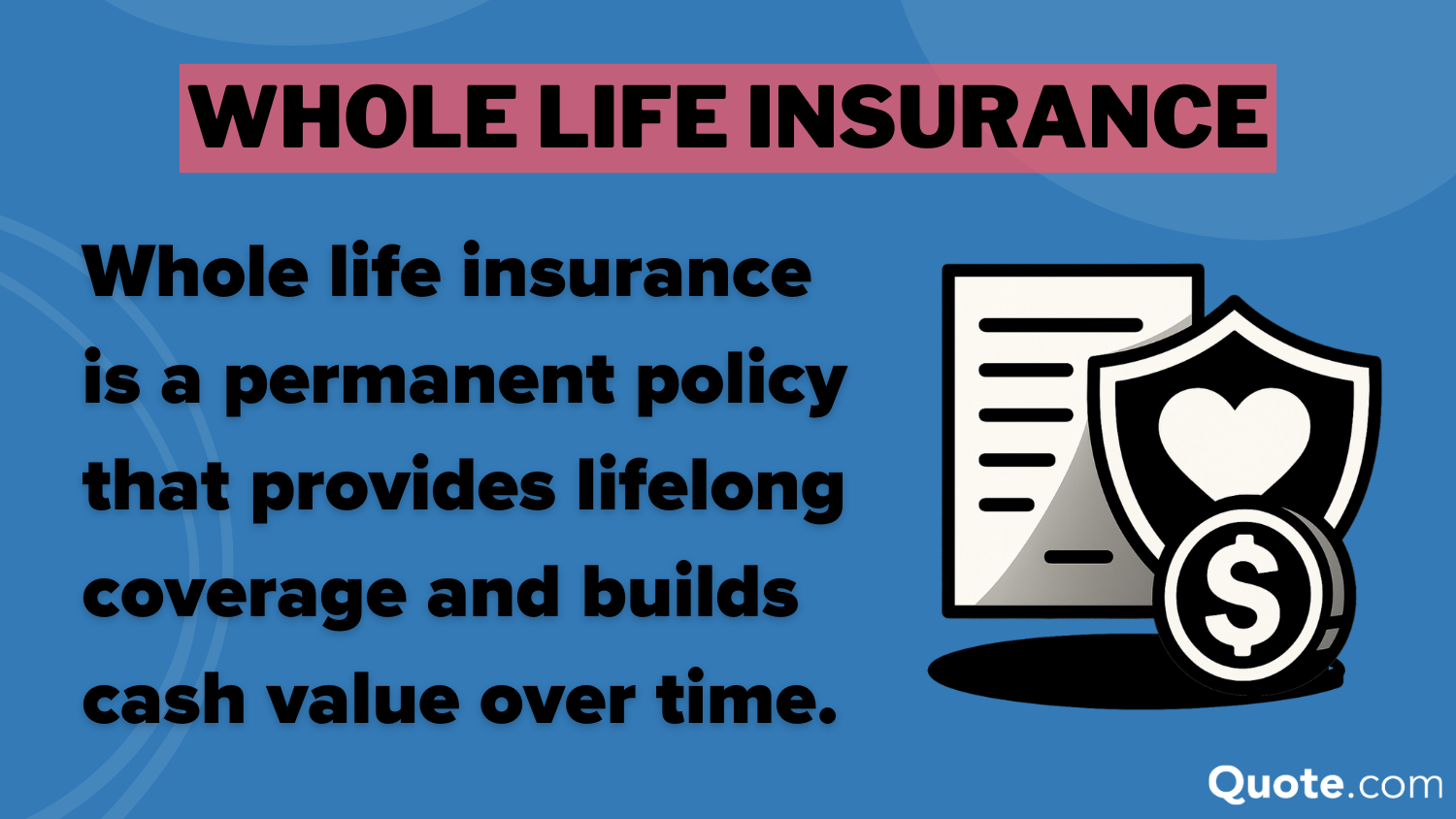

PostWhole life insurance is permanent coverage that lasts a lifetime as long as premiums are paid, ensuring a guaranteed payout to beneficiaries. It differs from......

Post

PostThe cheapest million-dollar life insurance starts at just $25 per month with Pacific Life, Prudential, and MassMutual, backed by strong financial stability. Pacific Life keeps......

Post

PostThere are several factors to consider when deciding how much life insurance you need, including your annual income, unpaid debts, and the number of dependents......

Post

PostThe main types of life insurance are term, whole, universal, variable, variable universal, final expense, and group insurance. Term life is most popular for affordability,......

Post

PostThe reasons to buy life insurance often come down to protecting your family, covering expenses, and building long-term financial security. Life insurance ensures that loved......

Post

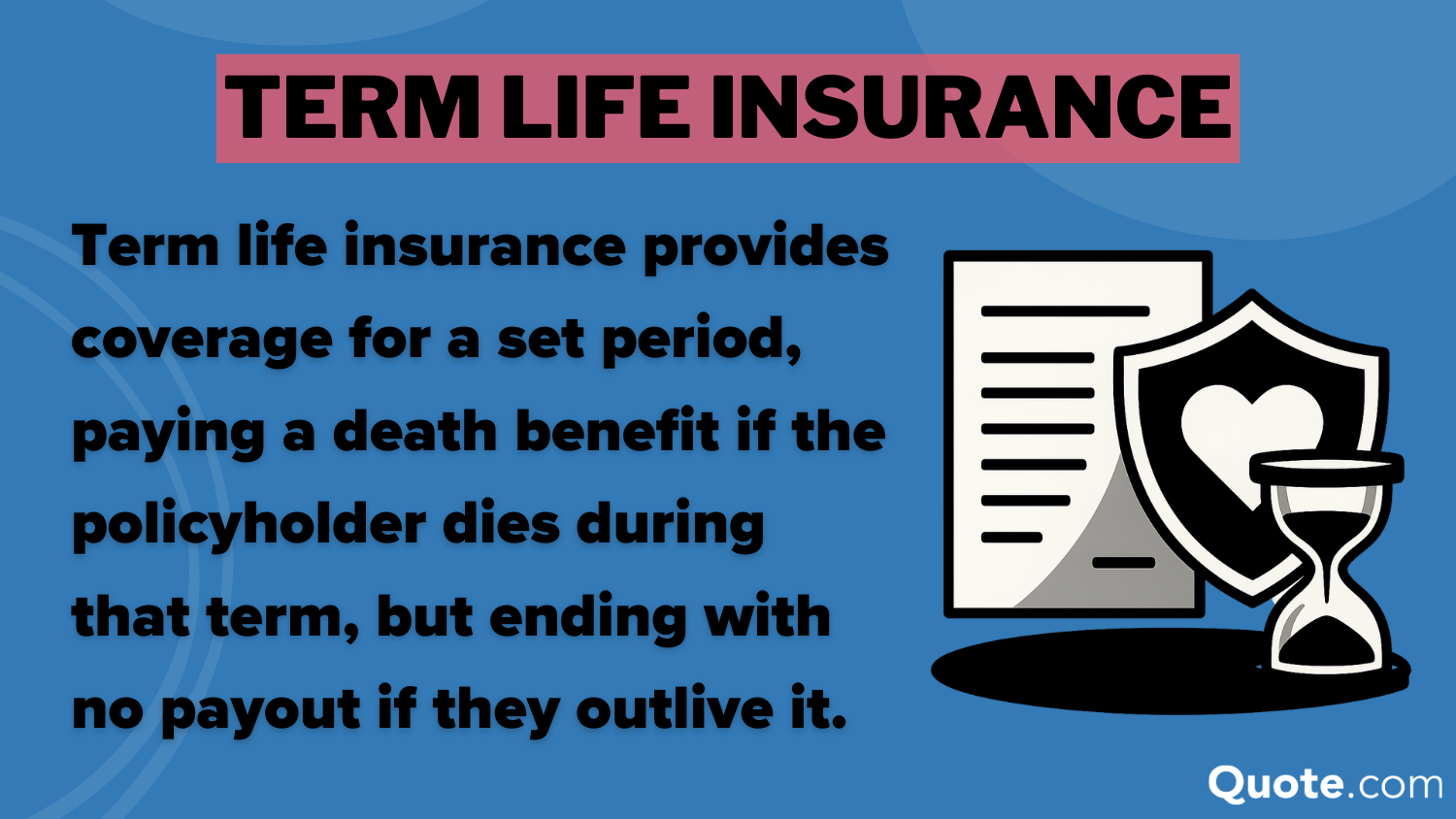

PostTerm life insurance provides simple, affordable financial protection during your family’s most critical years. Policies typically last 15-30 years, offering flexibility for different life stages......

Post

PostThe average cost of life insurance varies depending on the policy type, age, health, and more. A 20-year term life insurance policy may start as......

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.

Enter your zip code below to view companies that have cheap insurance rates.