How to File a Wildfire Home Insurance Claim in 2026

Claim denials are as high as 51% at some companies, so learning how to file a wildfire home insurance claim is crucial. Getting the best wildfire insurance payout requires you to document the damage and work with an adjuster. Our eight steps make it easy to resolve your claim and start repairing your home.

Read more

Table of Contents

Table of Contents

Insurance and Finance Writer

Luke Williams is a finance, insurance, real estate, and home improvement expert based in Philadelphia, Pennsylvania, specializing in writing and researching for consumers. He studied finance, economics, and communications at Pennsylvania State University and graduated with a degree in Corporate Communications. His insurance and finance writing has been featured on Spoxor, The Good Men Project...

Luke Williams

Senior Director of Content

Sara Routhier, Senior Director of Content, has professional experience as an educator, SEO specialist, and content marketer. She has over 10 years of experience in the insurance industry. As a researcher, data nerd, writer, and editor, she strives to curate educational, enlightening articles that provide you with the must-know facts and best-kept secrets within the overwhelming world of insurance....

Sara Routhier

Licensed Insurance Producer

Dani Best has been a licensed insurance producer for nearly 10 years. Dani began her insurance career in a sales role with State Farm in 2014. During her time in sales, she graduated with her Bachelors in Psychology from Capella University and is currently earning her Masters in Marriage and Family Therapy. Since 2014, Dani has held and maintains licenses in Life, Disability, Property, and Casualt...

Dani Best

Updated March 2026

Figuring out how to file a wildfire home insurance claim might be the furthest thing from your mind after a loss.

- Most home insurance providers offer 24/7 claims support

- Keep a record of temporary repairs for reimbursement on your claim

- One claim raises rates to an average of $154/mo for a $350K home

However, all you need to do to get your home insurance payout as quickly as possible is follow eight easy steps. To successfully submit a wildfire homeowners insurance claim, you’ll need to take steps like speaking with a claims adjuster and documenting the damage done to your home.

Get homeowners insurance coverage and learn everything you need to know about how wildfire insurance claims work below. If you don’t have coverage or you want to upgrade an existing policy, enter your ZIP code into our free comparison tool to find the cheapest rates in your area.

Filing a Home Claim After Wildfire Damage

When your home is damaged or destroyed in a wildfire, figuring out the claims process for your home insurance might be stressful.

Buying homeowners insurance is always important, but it’s critical if you live in a fire-prone state, especially since some policies specifically exclude wildfire coverage from house fire insurance claims.

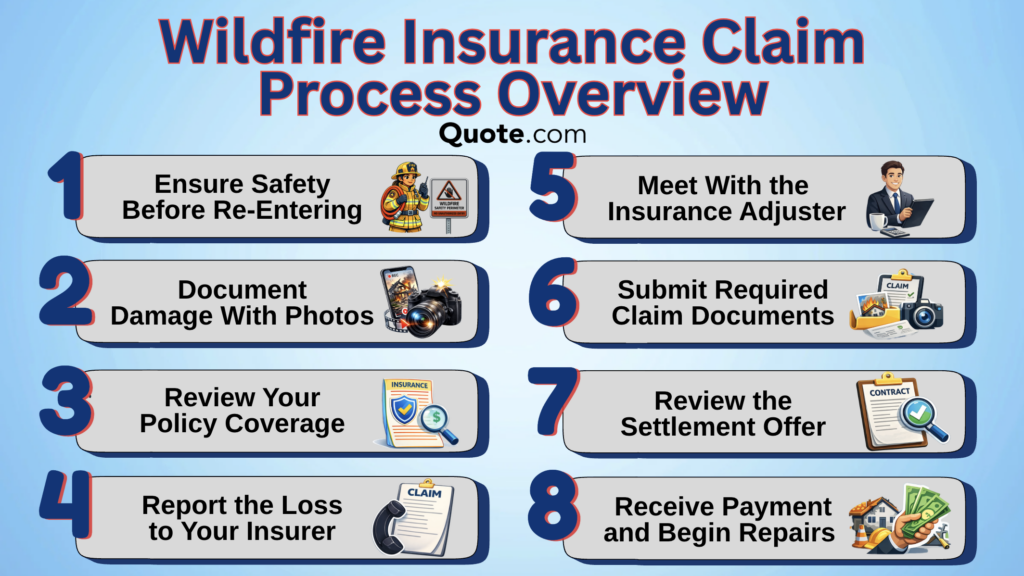

How to File an Insurance Claim After a Wildfire| Step | Action | Details |

|---|---|---|

| #1 | Notify Company | Notify your insurer immediately to report damages |

| #2 | Document Damage | Record all damage to structures and belongings |

| #3 | Keep Records | Log insurance communication with dates and names |

| #4 | Temporary Repairs | Make temporary repairs to prevent further damages |

| #5 | Form Submission | Submit the claim form with other required documents |

| #6 | Meet Adjuster | Allow adjuster to inspect damages to assess the claim |

| #7 | Review Settlement | Review the offer and negotiate if it doesn't cover losses |

| #8 | Close Claim | If satisfied, finalize the claim to receive compensation |

After figuring out that home insurance does cover wildfire damage, most homeowners want to start the claims process immediately. Related: Does home insurance cover wildfires?

While you should file quickly, your claim will be more likely to be approved if you follow the proper steps for the standard fire insurance company claims.

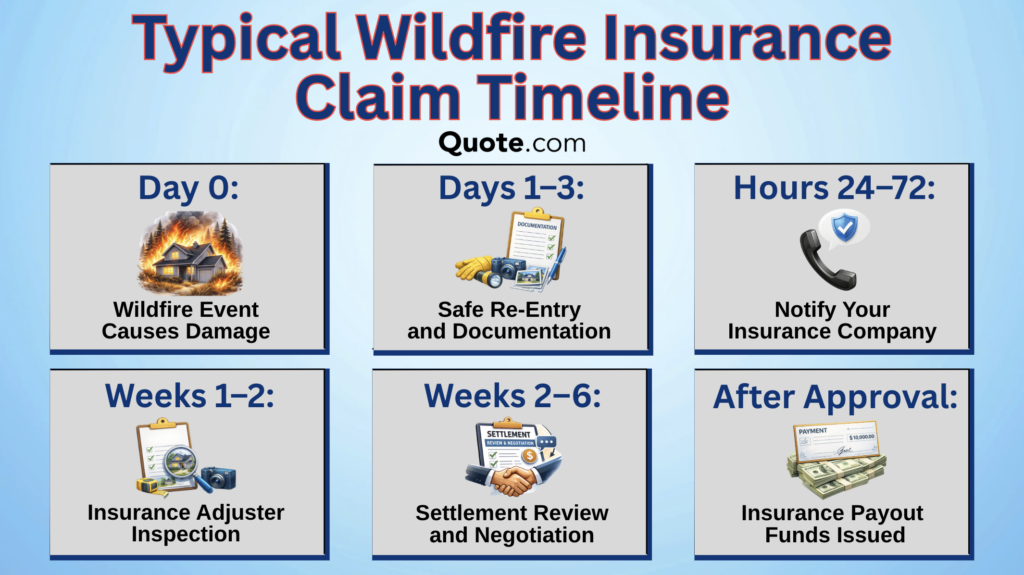

You can have your claim successfully filed in just eight simple steps, starting by notifying your insurance company.

Then, you’ll want to follow the steps your provider outlines on how to claim fire insurance, from collecting evidence of damage to filling out forms.

Step #1: Contact Your Provider

Contacting your provider as soon as you can is the first crucial step in getting your home repaired or rebuilt. If you are with one of the best providers for home insurance, the process is usually simple. Read our article for more details: Best Homeowners Insurance Companies

Whether you want to contact your provider over the phone, through a mobile app, or on your company’s website is up to you, but you should do it as soon as you’re safe. State laws for claim-filing deadlines vary, but generally, you’ll want to file as soon as possible.

Most providers offer 24/7 claims support. After natural disasters, these support systems are swamped with requests, so get your claim in early.

Kristen Gryglik Licensed Insurance Agent

When you initially contact your provider, you’ll need some basic information on hand. You don’t need every detail yet, though – your provider only needs the basics at this point.

If you can’t get to your homeowners insurance claim right away, that doesn’t mean you won’t be able to file. All insurance companies give you a little wiggle room to make your claim.

While most homeowners have up to a year to file a claim, that may not be the case. For example, Arizona state law gives homeowners up to six years to file a claim. Other states only require insurance providers to accept claims for 30 days.

Regardless of how much time you have to file, you’ll get your fire insurance payout quickest by filing early. You can also receive a smaller payout if you postpone filing your claim for too long, as it will be harder to prove fire damage.

Step #2: Document Wildfire Damage

Once you can safely enter your home, you’ll need to gather evidence for your wildfire damage insurance claim.

The more information you gather in this step, the better your chances of a successful claim are. Following a wildfire claim documentation checklist can help you make sure you have all the evidence you need.

You’ll need to make sure you record as much information as possible to increase your chances that your insurance claim for wildfire damage will be successful, whether you are filing a fire claim with Utica or Allstate.

Make sure to take photos and video of anything that was damaged by the fire, including burnt structures, destroyed belongings, and anything damaged by soot.

Important Documentation for Wildlife Insurance Claims| Type | How it Helps |

|---|---|

| Claim Forms | Required to start a wildfire claim |

| Insurance Policy | Lays out your coverage limits |

| Inventory of Damages | Provides a list of damaged belongings |

| Photographs & Videos | Acts as visual proof for your claim |

| Receipts for Expenses | Shows what reimbursement should be |

You’ll need all the evidence you collected for the upcoming steps below, so make sure to be as detailed as possible.

This is also an important step if you rent your home. The best renters companies will require similar documentation for your damaged belongings. See More: Best Renters Insurance Companies

Step #3: Keep Records and Receipts

The next step in how to file an insurance claim for fire damage is to keep all records of what you spend. While you should wait for your wildfire payout to arrive before you start repairing your home, some repairs can’t wait.

Whether you are a landlord making quick repairs for tenants or a homeowner, if you need to spend money before your claim is resolved, make sure to keep receipts. Read More: Best Home Insurance for Landlords

In most cases, your insurance provider will reimburse you for anything covered by your policy in your insurance claim quote, so long as you keep your receipts. Having these receipts from temporary repairs for damages caused by the fire will also help you appeal a claim denial. Documents required for a fire insurance claim reimbursement can include:

- Temporary lodging

- Food

- Clothes

- Urgent repairs to make your home livable

Many insurance experts recommend having an updated home inventory that you can show your provider during the wildfire insurance claims process.

Fire damage can be extensive, but having an inventory makes learning how to file a claim after a wildfire that much easier.

Step #4: Perform Temporary Repairs

When you compare homeowners insurance quotes, hopefully you’ll get the best coverage possible to help pay for fire damage repair services. See More: How to Compare Home Insurance Quotes

However, not even the best home insurance policy will pay out immediately after you file a claim. If your home needs temporary repairs to prevent more damage from happening, you won’t have time to wait for your insurance payout. Remember – your insurance company will reimburse you for covered expenses.

Examples of temporary repairs you should make include boarding up windows, patching holes, and removing debris.

Try to hold off on any permanent repairs until your claim has been processed. Once you receive your settlement, you’ll have a clearer picture of your repair budget.

Step #5: Submit a Wildfire Insurance Claim

No matter what type of property insurance you have, submitting a fire insurance claim form is usually easy. Most companies offer a variety of ways to start a claim, including over the phone and with a mobile app.

Not every company has a mobile app that accepts home insurance claims, but the major providers like State Farm do. Our State Farm insurance review goes into more detail on filing an insurance claim with State Farm.

To start your property or wildfire belongings claims, you’ll need to fill out a claim submission form. Make sure to fill the form out completely and include any documentation you’ve collected.

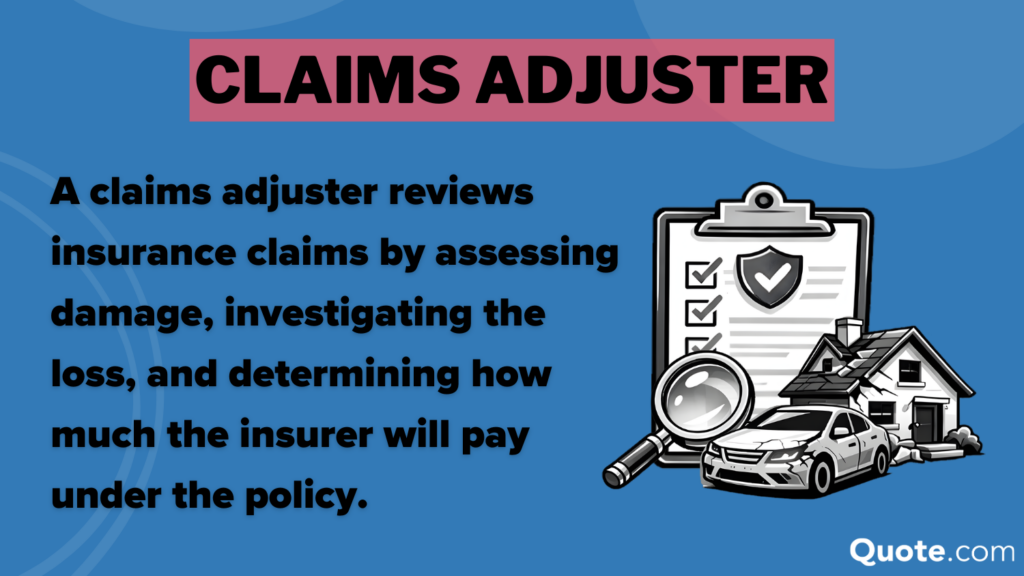

Step #6: Meet With an Adjustor

Once your company has processed your claim request, they’ll send a claims adjuster to assess. Meeting with an adjuster might be intimidating, but one of our best wildfire insurance adjuster tips is to remain available by phone, email, or text in case an insurance adjuster has questions.

Keeping in touch with your provider is a simple way to keep the claims process moving toward a resolution and to get help with an insurance claim after a fire.

The claims adjuster’s evaluation of the damage to your home is one of the most crucial steps in the claim process.

They’ll likely have questions, so you can help keep things smooth by providing information and responding quickly to any requests.

Step #7: Review Your Claim Settlement

After the adjuster finishes their evaluation, you’ll get a settlement offer. Review it closely to confirm it covers all damages and costs.

While meeting with an adjuster might make you nervous, you’ll have ample opportunity to make your case. If you need to negotiate your claim settlement to maximize your fire damage insurance payout, you can counter your insurance company’s offer.

Your adjuster will stay in touch, allowing you to provide supporting evidence, like photos and repair estimates.

Stay courteous but firm throughout the process – adjusters are fair, but companies often want to minimize how much they have to pay.

Scott W. Johnson Licensed Insurance Agent

Similar to the worst states to file a car insurance claim in, some states may see slower claim resolutions for home insurance.

If you feel like your claim payout is well below the average insurance payout for house fires, and your insurance company won’t work with you, you may need legal help for your insurance claim for fire damage. A lawyer who specializes in insurance law will know all your options.

Step #8: Close Your Claim

Once you accept the settlement and receive the house fire insurance payout from a wildfire, verify that your claim is officially closed. Hopefully, you won’t need it, but keeping all documentation is wise for future reference on standard fire insurance company claims.

After your claim is closed, your provider will send a check for the agreed amount. While wildfire claim timelines vary, most insurers issue payments within 2 months.

Taking steps like safeguarding your home and updating your coverage can help streamline any wildfire claims you may file.

If you’re not satisfied, some companies make it easy to re-evaluate your claim. For example, Allstate offers a claim guarantee that may apply to your home insurance. To learn more, check out our Allstate insurance review.

Free Home Insurance Comparison

Compare Quotes From Top Companies and Save

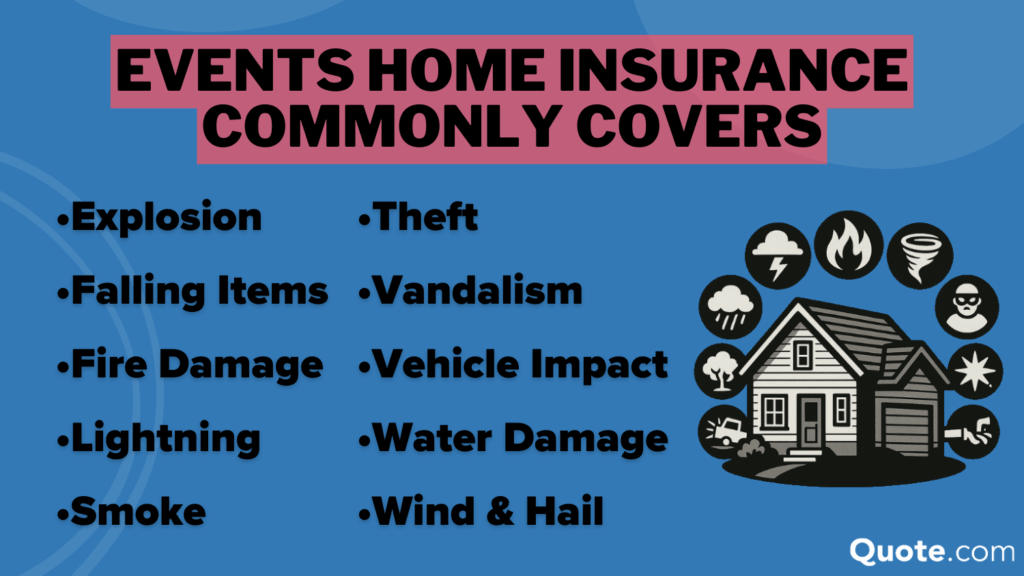

Wildfire Damages Typically Covered

Home insurance usually covers several types of damage that may result from a fire, landscaping losses, and shed damage. Home insurance will also cover smoke and soot damage if you file a wildfire smoke damage claim.

However, there may be limits on what your home insurance covers, such as debris removal after a wildfire or how much insurance will pay for wildfire additional living expense (ALE) reimbursement.

What Home Insurance Covers After a Wildfire| Claim Type | Covered? | Details |

|---|---|---|

| Additional Living | ✅ If uninhabitable | Temporary housing and meals |

| Debris Removal | ⚠️Limit applies | May have reimbursement cap |

| Dwelling Structure | ✅ Core protection | Primary home structure |

| Fire Damage | ✅ Core protection | Direct flame-related loss |

| Landscaping Loss | ⚠️ Limited benefit | Trees and plants limited |

| Other Structures | ✅ Separate limit | Detached garages or sheds |

| Personal Property | ✅ Personal items | Furniture and belongings |

| Smoke and Soot | ✅ Cleaning required | Professional cleaning needed |

| Vehicle Damage | ❌ Auto policy | Covered under car insurance |

| Water Damage | ⚠️ Often included | From firefighting efforts |

For instance, while you should make sure to carefully document your additional living expenses (ALE) for temporary housing and food, such as keeping hotel bills, bear in mind that there may be a limit on what insurance will cover.

Other things, like vehicle damage, will be wildfire policy exclusions for fire damage, as they’re protected under other types of insurance.

Learning more about what home insurance covers will help you understand what insurance coverage you should keep on your policy for the best protection. Read more: Ultimate Insurance Cheat Sheet

Documenting Damages Safely After a Wildfire

When is it safe to re-enter a property after a wildfire? While you may want to rush back to your home to assess damages, you should only go back to your property to document the damage after law enforcement or the fire department says it is safe to do so.

The last thing you want to do is to have to file a claim with your health insurance because you got injured on your property, which is why you should always ensure safety before rushing to file a claim.

Make sure to watch out for hotspots and other hazards when inspecting your property after a wildfire. If your home is deemed structurally damaged, do not enter the home.

You should also not attempt to turn utilities on yourself until a utilities company has inspected your property and says it is safe to do so.

How to Handle Wildfire Claims Denials

Now that you know how to file an insurance claim after a wildfire, we will go over what to do if insurance denies your wildfire damage claim.

There are several wildfire claim denial reasons why your claim might be denied or delayed after a fire. You may even be denied coverage after a fire at your next renewal if you are deemed high-risk. Check out our guide for more details: What to Do When You’re Denied Insurance Coverage

Top Reasons Wildfire Claims Get Delayed or Denied| Issue | Risk | How to Avoid |

|---|---|---|

| Coverage Exceeded | ⚠️ Limit reached | Loss exceeds policy limits |

| Damage Disputed | ⚠️ Value dispute | Insurer questions damage scope |

| Documentation Gaps | ⚠️ Missing proof | Incomplete photos or inventory |

| Late Reporting | ✅ Report early | Notify your insurer promptly |

| Missed Deadlines | ⚠️ Filing lapse | Required forms not submitted |

| Policy Exclusions | ❌ Not covered | Excluded under policy terms |

| Unverified Ownership | ⚠️ No receipts | No proof of item ownership |

While not all denials can be prevented, such as if you have inadequate coverage for damages, there are some denials or delays you can try to fix.

For example, denials and delays caused by missing proof can be avoided by ensuring you make a complete inventory of all damaged items and include photographs.

Provider Wildfire Claim Denials

One step you can take to reduce the chances of a future claim being denied is to shop at companies with a good reputation for paying claims.

This is especially important if you need California wildfire insurance, as wildfires are frequent in California.

The list of providers with the worst history of denying homeowners insurance claims after a wildfire includes companies like Allstate and Farmers. When reviewing Allstate, we found that they also have consistently higher rates than most providers.

If your coverage comes from one of the best homeowners insurance companies and you’ve still been denied, you’re not totally out of options.

Reversing a Denial from Your Insurance Provider

Even the best companies may deny claims. See More: Best Home Insurance Companies

If your claim has been denied by your company, there are a few things you can do to try to reverse the decision. Try the following steps to reverse a denied wildfire insurance coverage claim at your company:

- Review the Denial: Your insurance company will send you a letter listing why your claim was denied. If you need help, an insurance representative can walk you through it.

- Submit an Appeal: Request the paperwork you need to file an appeal from your company. Provide as much evidence as possible for your company to review.

- File a Complaint: If your insurance provider isn’t dealing with you fairly, you can submit a complaint to your state’s insurance department.

Getting home insurance for wildfires can be stressful, especially in areas with increasing fire risks.

That’s particularly true in states like California and Florida, where disaster insurance claims happen more frequently. Related: Home Insurance Rates by State

Free Home Insurance Comparison

Compare Quotes From Top Companies and Save

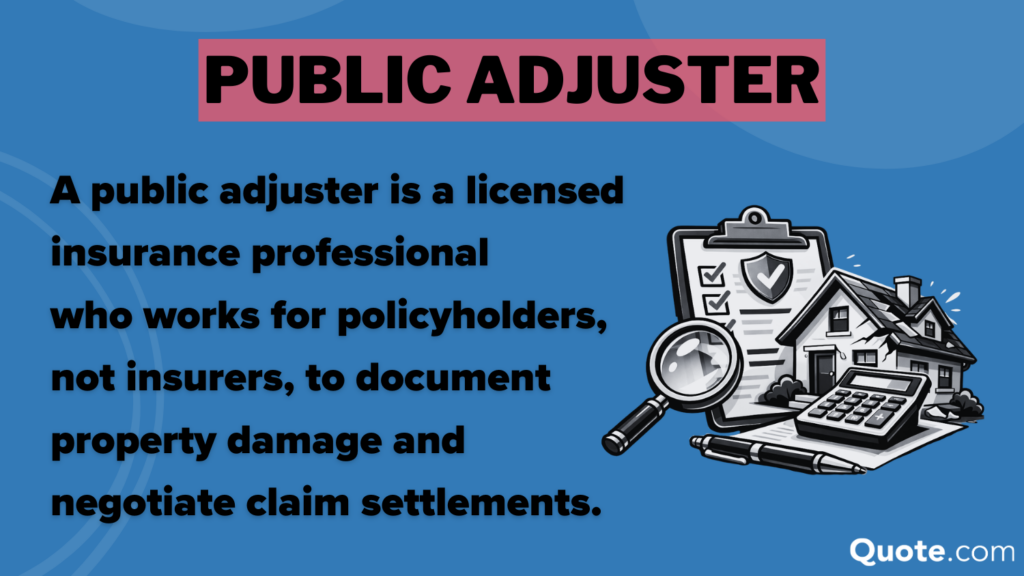

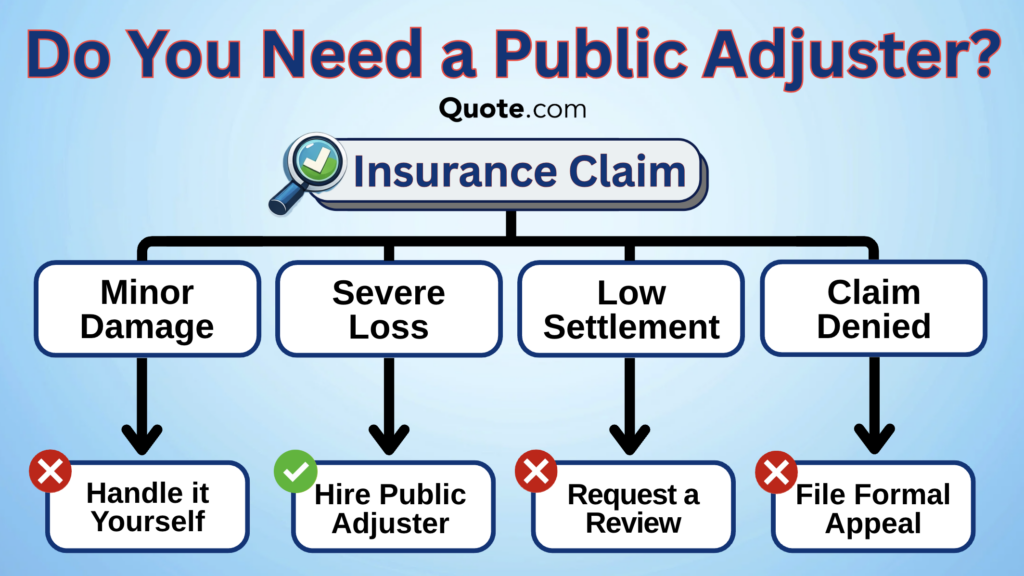

Hiring a Public Adjuster or Attorney

If you need help with appealing a claim or want a second opinion, you can get help from a public adjuster before going to an attorney. There are several wildfire public adjuster benefits that will make the process smoother.

Public adjusters work with you to help negotiate a wildfire claim settlement with your insurance company. This is useful if you believe your settlement is inadequate.

It can be beneficial to hire a public adjuster if you don’t feel confident in contesting a claim settlement.

They can also advise you on when it might be wise to reach out to a state insurance regulator for additional assistance.

A public adjuster can help you negotiate your claim settlement after assessing the damage done to your home from a wildfire.

In extreme cases where a company is unwilling to approve a claim or is offering an unfair settlement, you can hire an attorney to help resolve your claim. No matter how your claim is resolved, make sure to keep records of all communication you have with your insurance provider to help your case if you have to contest it in court.

When finding the cheapest homeowners insurance for wildfires, using a free online comparison tool makes it much easier. Using one is easy – simply enter your ZIP code to get started.

Wildfire Claims and Insurance Rate Raises

Before filing a claim with your home insurance provider, you should make sure that filing a claim is the right choice.

There are many factors that affect home insurance rates, but your claims history is among the most impactful.

Home Insurance Monthly Rates by Claims & Coverage| Claims | $350K | $500K |

|---|---|---|

| 0 | $140 | $184 |

| 1 | $154 | $198 |

| 2 | $175 | $220 |

| 3 | $203 | $250 |

| 4 | $238 | $288 |

Filing a home fire insurance claim for damages will increase your home insurance cost per month.

Consequent claims on your home insurance record indicate that you live in a higher-risk area, which will substantially raise your rates annually.

Because claims have such an impact on your home insurance rates, if home repairs after a wildfire will cost less than your home insurance deductible, you should skip filing a claim. Read our article for more details: Insurance Deductibles

However, make sure you have assessed the damage to make sure that home repairs won’t cost more than expected before choosing to forgo house insurance fire claim filing.

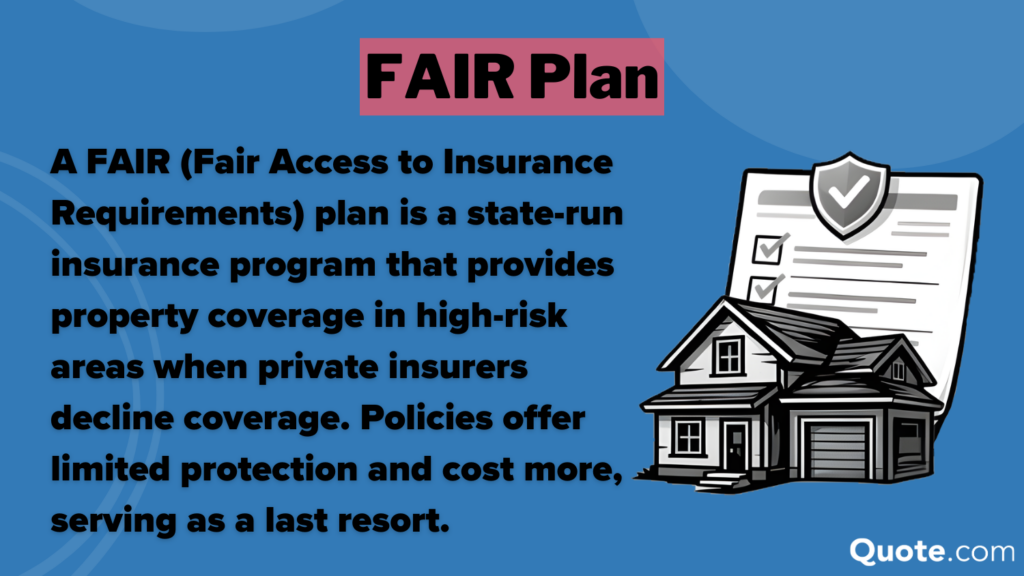

FAIR Plans for High-Risk Homes

Not sure how to get home insurance after a fire if you live in a high-risk area? FAIR programs help homeowners in fire-prone areas get insurance for their homes.

For example, the California FAIR plan ensures California residents can get wildfire recovery assistance in even the highest-risk areas where homeowners may have trouble getting home fire insurance in California.

Check Out: Is home insurance required?

With wildfires being one of the most dangerous risks homeowners face, having FAIR fire insurance in California can save you thousands.

Compared to traditional policies, FAIR home insurance plans offer less protection. However, California fire insurance FAIR plans can be affordable, depending on where you live. FAIR policies are managed by multiple companies, so you will have to get a California home owner insurance quote from the FAIR website.

You’ll file claims on the FAIR website, but each company involved in your policy will pay a portion of your claim for wildfire damage.

However, FAIR shouldn’t be your first stop for home insurance for a high-risk home, particularly because it won’t cover everything you lose in your home, and it may not offer the cheapest fire insurance in California. Read our article for more details: Best Insurance for High-Risk Homes

In fact, one of the requirements for FAIR approval is providing proof that you’ve been denied coverage from other providers. So it may be harder to qualify for a pooled insurance plan if you are shopping for Kentucky home insurance after a fire, compared to somewhere higher risk like California.

However, if you can’t find coverage anywhere else, a FAIR plan will make sure you won’t completely lose your home after a fire, even though it isn’t the cheapest California home insurance in high fire risk areas.

Maximizing Insurance Payouts After a Wildfire

When it comes to homeowners insurance and wildfires, making sure you have adequate coverage is one of the best steps you can take to avoid problems.

Knowing how to file a home insurance claim after a wildfire and increasing your home fire safety can help minimize the risk of filing a claim altogether.

If you don’t have the right amount of coverage for a wildfire, you should start looking for a policy with affordable rates today. Learn more in our guide: Home Insurance Rates

Checking your options periodically is an important step in maintaining a policy that works for you. Whether you want to shop for new homeowners insurance after a fire claim or need your first policy, you can find affordable home insurance rates by entering your ZIP code into our free comparison tool.

Frequently Asked Questions

How long do you have to file a wildfire home insurance claim?

The wildfire claim timeline varies by insurer, but most policies require you to file a house fire insurance claim within 30 to 60 days after the wildfire. It’s best to check your policy and report damage as soon as possible, as after a wildfire, how long to file a claim by state varies.

How do you file a homeowners insurance claim after a wildfire?

The first step in how to file a fire insurance claim is to contact your insurance provider. You should then document the damage with photos and provide an inventory of lost items. An adjuster will assess the loss and give a fire damage insurance quote for compensation, and your insurer will determine the payout based on your coverage.

Are wildfires covered by home insurance?

Wondering does home insurance cover wildfires? Yes, standard homeowners insurance typically covers wildfire damage, but coverage may vary by location and provider. Some high-risk areas may require separate wildfire insurance or a FAIR plan.

Knowing what coverage you need to cover wildfire damage can help you get the best policy for your house. Check Out: How Much Home Insurance You Need

What does home insurance cover for wildfire damage?

Now that you know the answer to “Does home insurance cover wildfire damage?”, you probably want to know exactly what damages are covered. Home insurance typically covers the cost to repair or rebuild your home, replace personal belongings, and pay for temporary living expenses if your home is uninhabitable.

It may also include coverage for landscaping, debris removal, and other structures like garages or sheds. Search for the best home insurance today by entering your ZIP in our free tool.

Does your home insurance go up after a fire?

Filing a claim will increase your home insurance costs, but home insurance rates after a wildfire will increase even if you didn’t file a claim. The increased risk of supplying home insurance in a wildfire area and the cost of your neighbors’ claims will impact your quotes for home fire insurance at the next renewal.

How much is wildfire insurance?

The cost of wildfire insurance depends on your location, home value, and risk level, with premiums ranging from a few hundred to several thousand dollars per year. Home insurance in high-fire-risk areas, like California, tends to have significantly higher rates.

For example, the average American pays $101 per month for home insurance, but rates in fire-prone Texas average $321 per month. In the top 10 states for wildfire risk, the average homeowner pays $207 per month for coverage.

You can compare home insurance quotes to find the best wildfire insurance rates in your area, as well as bundle auto and home coverage for a discount. Read our article for more details: Best Auto and Home Insurance Bundles

Do you still own the land if your house burns down?

Yes, if your house burns down, you still own the land, as homeowners insurance only covers structures and belongings, not the land itself. You can rebuild or sell the property as you choose.

Does homeowners insurance cover wildfire damage in California?

Standard homeowners insurance policies in California cover wildfire damage, but some insurers have pulled out of high fire risk areas. If private coverage is unavailable, homeowners may need to rely on the state’s FAIR plan. To see what wildfire insurance quotes are available, enter your ZIP code into our free insurance comparison tool.

What’s not covered by home insurance after a wildfire?

Standard policies may not cover certain losses, such as damage due to neglect, pre-existing conditions, or costs exceeding policy limits. Landscaping, fences, and expensive valuables like jewelry may require additional coverage. You’ll also need the right home insurance to cover wildfire damage. See More: Types of Home Insurance

Why do insurance companies deny claims after a wildfire?

Standard fire insurance company claims can be denied if the damage isn’t covered under the policy, if the homeowner failed to maintain the property, or if there’s insufficient documentation. Policies with exclusions for wildfires or lapsed coverage can also lead to denial.

Are accidental fires covered by insurance?

What’s the biggest mistake people often make when dealing with an insurance claim?

Related Articles

-

Jul 2026

Best Home Insurance in Rhode Island for 2026

-

Jun 2026

Cheap Earthquake Insurance in 2026 (Find the Best Rates)

-

Jul 2026

Best Home Insurance in South Dakota for 2026

-

May 2026

How Roof Inspections Affect Home Insurance: Cost & Coverage Impact in 2026

-

Jun 2026

How to Switch Homeowners Insurance: 6 Steps to Change Providers & Save (2026)

-

Jul 2026

Rental Property Insurance: Costs, Coverage & Savings Tips (2026)

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.