CLUE Report: How Claims History Affects Insurance Rates in 2026

Your CLUE report contains up to seven years of auto and home insurance claim history. Drivers without claims pay an average of $110 a month, and claim-free homeowners average $95 monthly. Top insurers like Geico, Progressive, and Allstate use LexisNexis CLUE reports to evaluate risk and price your policy.

Read more![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Table of Contents

Table of Contents

Insurance and Finance Writer

Karen Condor is an insurance and finance writer who has degrees in both journalism and communications. She began her career as a reporter covering local and state affairs. Her extensive experience includes management positions in newspapers, magazines, newsletters, and online marketing content. She has utilized her research, writing, and communications talents in the areas of human resources, f...

Karen Condor

Head of Content

Meggan McCain, Head of Content, has been a professional writer and editor for over a decade. She leads the in-house content team at Quote.com. With three years dedicated to the insurance industry, Meggan combines her editorial expertise and passion for writing to help readers better understand complex insurance topics. As a content team manager, Meggan sets the tone for excellence by guiding c...

Meggan McCain

Commercial Lines Coverage Specialist

Michael Vereecke is the president of Customers First Insurance Group. He has been a licensed insurance agent for over 13 years. He also carries a Commercial Lines Coverage Specialist (CLCS) Designation, providing him the expertise to spot holes in businesses’ coverage. Since 2009, he has worked with many insurance providers, giving him unique insight into the insurance market, differences in ...

Michael Vereecke

Updated March 2026

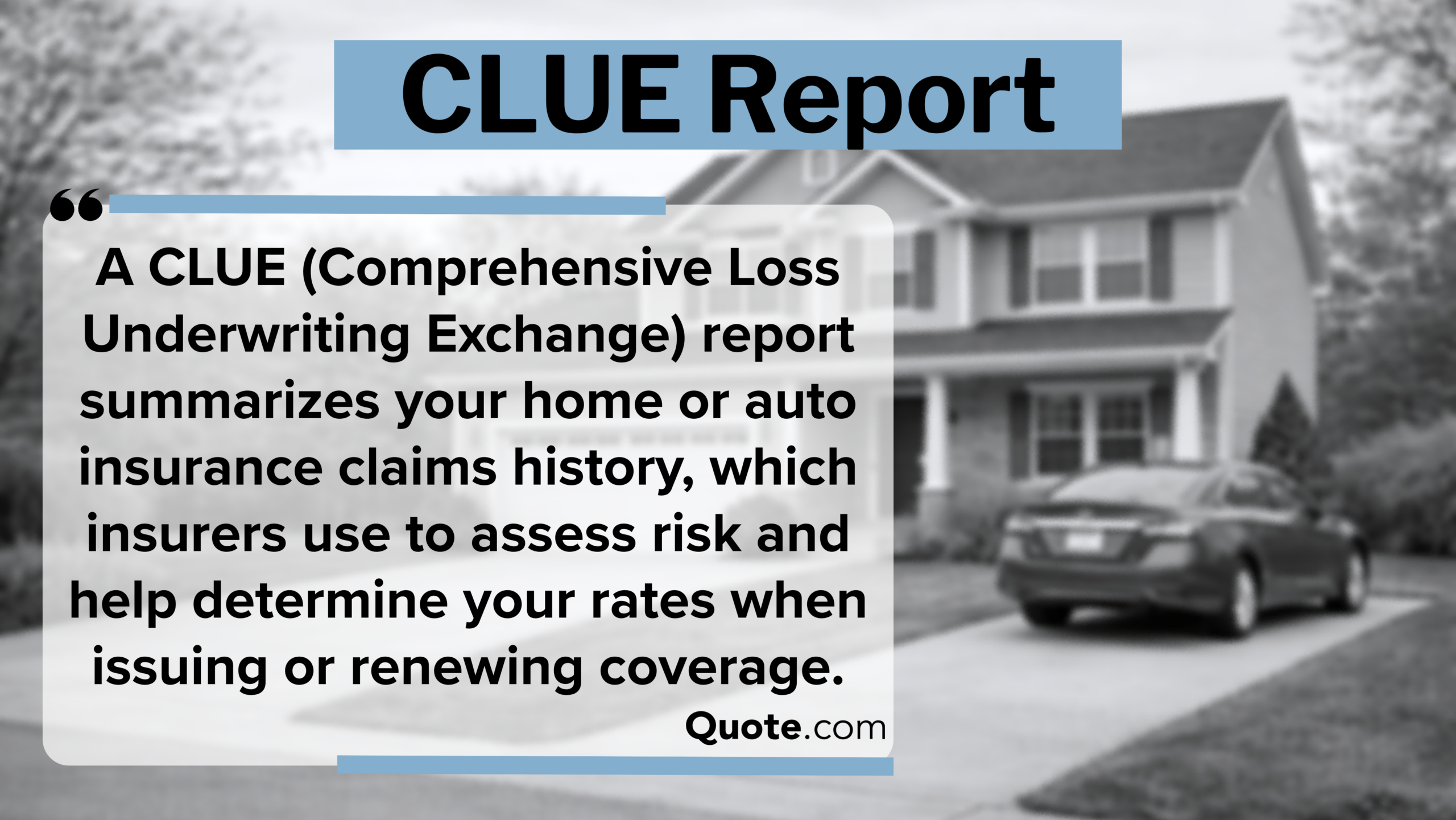

A CLUE report, also known as a Comprehensive Loss Underwriting Exchange report, includes up to seven years of insurance claim history.

- Insurers use CLUE report data to assess risk and price policies

- Three or more claims can raise monthly rates by $40 or more

- CLUE report errors can raise insurance rates if claim records are wrong

Insurance providers will review your CLUE report from LexisNexis to assess risk based on your claim history. At-fault accidents and auto insurance rates are closely linked, and having multiple accident claims on your record can push minimum coverage to $170 a month.

Reviewing your CLUE report can show how claim history may affect insurance quotes and coverage options. Enter your ZIP code in our free comparison tool to see how local providers price coverage near you.

How CLUE Reports Work

A CLUE (Comprehensive Loss Underwriting Exchange) report contains up to seven years of insurance claim history tied to a person, vehicle, or property.

It includes a detailed list of your claims, including loss date, claim type, payout amount, property, and status. Insurers use this information to assess risk and calculate annual premiums.

It’s important to review CLUE reports when comparing insurance quotes because claim history can affect coverage options and pricing.

Requesting your report can confirm that your claim record is accurate. Learn More: How to File a Claim and Win

Insurers review CLUE reports to understand past claims and estimate future risk, which can affect premiums and coverage eligibility. Correcting an inaccurate claim can help you get lower rates.

Dani Best Licensed Insurance Agent

Policyholders can request to review their own CLUE report insurance information at any time.

With it, they can check their claim history, confirm the details are correct, and dispute errors that could be raising their rates.

Not everyone can access your CLUE report. Only yourself, insurance companies and agents, and those selling or buying a home can request a CLUE report.

For instance, home sellers should request a CLUE report before listing a property to verify prior claims and prepare accurate disclosures.

Who Can Access Your CLUE Report| Requester | Reason | Focus |

|---|---|---|

| Home Buyers | Assess property risk | Property claim history |

| Home Sellers | Prepare sale disclosures | Property loss records |

| Insurance Agents | Compare policy quotes | Claim history summary |

| Insurance Companies | Price new policies | Full claim record |

| Policyholders | Review report accuracy | Personal claim history |

Home buyers will often ask sellers to provide a property report so they can review prior claims, such as fire or water damage, that could affect home insurance rates.

However, be aware that claim history does not directly set insurance rates. It is one of many variables insurers use to assess risk, and you should always compare multiple quotes to see how different providers calculate premiums.

Free Auto Insurance Comparison

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

How Claim History Impacts Insurance Premiums

Insurance companies review claim history for several years when setting premiums. A claim filed within the past year usually causes the largest premium increase.

Claims that are less than three years still influence quotes, but rates start to drop after five years, especially if you’ve avoided other losses during that time.

CLUE Report: How Claims Affect Insurance Rates Over Time

| Claim Filed | Cost Impact | Insurer Use |

|---|---|---|

| Under 1 Year | Largest price increase | Highest risk weight |

| 1–3 Years | Higher quote ranges | Still affects pricing |

| 3–5 Years | Moderate price change | Reduced rating weight |

| 5–7 Years | Small price change | Minimal pricing role |

| Over 7 Years | No price effect | Removed from record |

Claims between five and seven years old cause only small price changes. After seven years, most claims are removed from your record, although some states may keep certain claims on your record for 10 years.

A CLUE report matters when getting insurance because it shows your claim history and risk potential, which impacts your rates and whether you qualify for coverage.

Insurance premiums often increase after a claim because insurers consider you more likely to file a claim again.

Review your CLUE report regularly before shopping for quotes or applying for a policy in order to correct any errors that could lead to unexpected rate changes.

How Different Claims Affect Insurance Costs

Claims for water and fire damage have the biggest impact on rates because they typically involve extensive property repairs and replacements.

Glass damage, on the other hand, causes smaller rate changes because windshield or window repairs are relatively inexpensive. Get more details in our guide: Does auto insurance cover windshield replacement?

Weather damage only raises rates by 10% since these claims are outside of a policyholder’s control. However, non-weather claims, like a theft or plumbing leak, raise premiums by 15% or more because those losses can be prevented.

An at-fault accident increases rates by 22% because it suggests poor driving behavior and a higher risk of future accidents.

How CLUE Reports & Claim History Impact Car Insurance

Drivers with no claims pay an average premium of around $110 a month and, being in the lowest risk category, have their choice of insurers.

The claims history in your CLUE report may affect your car and home insurance premiums. Learn how to compare auto insurance companies to find better rates if you have multiple claims on your record.

Auto Insurance Monthly Cost Impact by CLUE Claims History| Claims | Premium | Impact |

|---|---|---|

| No Claims | $110 | Widest carrier access |

| 1 At-Fault Accident | $128 | Standard market pricing |

| 2 Accidents | $145 | Some carrier restrictions |

| 3+ Accidents | $170 | Limited low-cost options |

| Major Recent Claim | $190 | High-risk tier pricing |

One at-fault accident may raise premiums to about $128 per month, while two accidents can increase rates to around $145 monthly and limit your coverage options.

If you have three or more claims on your CLUE report, premiums average $170 per month, and you may only qualify for coverage with nonstandard insurers.

A major recent claim can raise rates to $190 per month and place a driver in a higher-risk tier, making it harder to find affordable premiums.

The importance of a CLUE report is clear because auto insurance premiums often rise as you file more claims. Compare Now: Cheap Auto Insurance for High-Risk Drivers

How CLUE Claims Impact Home Insurance Costs

Insurance premiums often rise as more claims appear in a CLUE report for home buyers or those refinancing their home.

Homes with no claims have an average premium of around $95 per month, and usually have the widest access to insurers since there is no record of prior damage.

Home Insurance Monthly Cost Impact by CLUE Claims History| Claims | Premium | Impact |

|---|---|---|

| No Claims | $95 | Widest carrier access |

| 1 Weather Claim | $120 | Standard rate adjustment |

| 2 Claims | $145 | Fewer policy options |

| 3+ Claims | $175 | Limited carrier approvals |

| Major Property Claim | $205 | High-risk tier pricing |

Premiums are near $120 per month with one weather claim, which is a small increase compared to three or more claims, which can nearly double rates to $175 a month.

A big claim on a property can push rates up to about $205 per month and put the home in a higher-risk pricing tier. Save money by shopping around for the best auto and home insurance bundles.

Claims history from a CLUE report can affect car and home insurance rates, but local housing and insurance claim trends also impact prices. Research your housing market to determine what your neighbors are paying for coverage and how your quotes compare.

While CLUE reports do not generate premiums themselves, insurers use the claims information during underwriting to help determine pricing and available coverage options.

For instance, if you live in a high-risk area and also recently filed a weather-related claim, your premiums could be even higher than another homeowner in the same neighborhood.

Types of Insurance Claims in CLUE Reports

CLUE reports for insurance track certain types of incidents that often lead to bigger claim payouts, like auto accidents and weather damage.

Hail, wind, and severe storms frequently damage roofs, cars, and other property covered by homeowners insurance coverage.

Theft is another common insurance claim, including vandalism and glass damage. Fires account for only 7% of claims but usually incur expensive losses.

Your CLUE auto claims report may look different based on where you live. State statistics on claims vary due to population size, driving conditions, weather risks, and local insurance laws.

Across the country, auto claims account for a larger share because vehicle accidents occur more often.

Lower numbers reflect fewer drivers and homes. Nebraska has about 18,000 total claims compared to California, which reports about 210,000 claims.

Important Details: How to File a Home Insurance Claim After a Wildfire

Most Common High-Risk Claims in a CLUE Report

Insurance companies review CLUE reports to identify claim patterns, and certain activities in the report can lead to higher premiums.

Auto accidents and other major auto claims, such as totaling a vehicle, will increase rates more than minor claims for glass damage.

CLUE Report Activity That Can Raise Insurance Rates| Factor | Insurer Signal | Price Impact |

|---|---|---|

| Auto Accident Claim | Recent accident history | Higher auto premiums |

| Major Auto Loss | Severe vehicle damage | High-risk auto pricing |

| Major Home Loss | Major property damage | High-risk classification |

| Multiple Auto Claims | Pattern of auto claims | Limited auto insurers |

| Multiple Home Claims | Repeated home claims | Fewer home insurers |

| Non-Weather Claim | Property loss history | Higher home premiums |

Multiple auto claims, especially for multiple at-fault accidents, increase pricing the most because insurers treat that as evidence that another accident could occur.

Several auto claims submitted in a short period may reflect a pattern of frequent incidents, which can limit the number of insurers willing to offer coverage.

For homeowners, a major loss like a large fire or water damage will raise premiums the most because these claims require expensive repairs. Learn how to compare home insurance quotes after a claim to get better rates.

Multiple home claims may raise similar concerns because repeated property losses can point to ongoing risks, such as plumbing problems or structural issues.

Best Insurance Companies Using CLUE Reports

Insurance companies have full access to your CLUE report online when you are applying for a new policy or renewing your current coverage.

Insurers rely on CLUE reports for accurate, up-to-date information on a policyholder’s claim history, but each uses the report for different things and assesses risk differently.

How Top Insurance Providers Use CLUE Reports| Company | CLUE Check | Pricing Impact |

|---|---|---|

| Reviews claim history | Higher premium risk | |

| Checks loss records | Eligibility restrictions | |

| Uses claim reports | Rate adjustment | |

| Pulls loss records | Higher policy price | |

| Reviews loss history | Pricing tier increase | |

| Uses property claims | Limited policy options | |

| Checks claim patterns | Policy cost shift | |

| Reviews loss records | Risk tier increase | |

| Checks claim activity | Rate change risk | |

| Checks prior incidents | Coverage restrictions |

For example, AAA considers prior claims to determine whether to increase premiums, while Allstate reviews loss records and may drop coverage if you have multiple claims. Read More: Allstate, vs. Farmers, Geico, Progressive, and State Farm

It pays to compare multiple insurers, especially if you have more than one claim on your record. Geico and Nationwide review claim history to classify drivers into risk categories and pricing tiers, which can help high-risk policyholders save money.

Free Auto Insurance Comparison

Compare Quotes From Top Companies and Save

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption

Handling Errors on Your CLUE Report

Errors can appear in a CLUE report because claim information comes from multiple insurers and may be entered incorrectly. Read More: What to Do When You’re Denied Insurance Coverage.

A misreported claim can occur when records are linked to the wrong person or property, often due to similar names or addresses.

CLUE Report Common Mistakes & How to Correct Them| Error | Cause | Fix |

|---|---|---|

| Claim Misreported | Records mixed together | Dispute with LexisNexis |

| Duplicate Claim | Same loss entered twice | Ask LexisNexis to fix |

| Incorrect Payout | Wrong payout reported | Request insurer review |

| Old Loss Listed | Report not refreshed | Ask LexisNexis to drop |

| Wrong Claim Status | Status not updated | Request insurer update |

An incorrect payout may appear if the insurer reported the wrong settlement amount, which requires the insurer to verify and update the claim record.

It’s important to keep a record of your claims because you can correct errors in your LexisNexis CLUE report by disputing the information and supplying proof.

Insurers use CLUE reports to set premiums, so errors can raise rates. Drivers should review their report before comparing quotes and disputing any duplicate claims.

Melanie Musson Published Insurance Expert

Companies use claims history to determine rates and eligibility for coverage. False or outdated information can be used against you when insurers evaluate risk during the quoting process.

Quickly disputing CLUE report errors is crucial to prevent higher auto or homeowners insurance rates at your next renewal.

Correcting inaccurate information ensures your record reflects the most up-to-date information before you start requesting quotes.

A CLUE report’s effect on insurance rates stems from how insurers review past claims to assess risk, which can influence premiums and coverage eligibility.

When You Need Your CLUE Report

People often request their CLUE report when claim history affects a financial decision, such as switching insurance providers. About 31% check their report to see how past claims could affect new quotes.

Around 27% review a CLUE report before buying a home to check for prior damage or costly claims and better understand how to buy home insurance for the property.

About 19% do so to verify the accuracy of reports, ensuring that claims and payouts are recorded accurately.

Roughly 13% review it after a claim denial to see what led to the insurer’s decision, and 10% request it before selling a home for potential buyers’ reassurance about the property’s claims history.

Review Your CLUE Report for Better Rates

A CLUE report shows a person’s auto and home insurance claim history, usually covering the past seven years. The report also helps insurers identify patterns such as repeated accidents or property damage.

Your claims history could increase your premiums if the insurance company considers you high-risk. Recent or multiple claims in the report may lead to higher rates.

Review your CLUE report before comparing quotes on the best insurance comparison sites. Checking the report regularly can also help identify mistakes and correct inaccurate claim records that could affect insurance pricing.

Enter your ZIP code to compare insurance quotes and see how your CLUE report history may affect available rates.

Frequently Asked Questions

What is a CLUE report, and how does it affect your insurance rates?

CLUE reports include up to seven years of claims history for an individual, vehicle, or property. Insurers check it to evaluate risk, and having multiple claims on your record can increase premiums. Compare auto insurance rates by vehicle to learn more.

How do insurers use CLUE reports to determine premiums?

Insurers review CLUE reports to examine your past insurance claims and identify patterns that may indicate higher risk. For instance, filing multiple claims in a short period could increase your rates with some providers.

Compare insurance options now by entering your ZIP code in our free quote comparison tool today.

Do all insurance companies use CLUE reports?

CLUE reports are not used by every insurance company, but most major insurers use them in underwriting to review claim history and assess risk. Some small insurers may use other internal records or risk assessment tools instead.

What is a CLUE report for car insurance?

A LexisNexis CLUE auto report includes your claim history, usually covering the past seven years. Insurers review it to assess risk and calculate premiums, which can affect eligibility for the cheapest car insurance rates.

How do I request a CLUE report?

You can get a CLUE report by requesting a free copy from LexisNexis, the company that maintains the database. Visit the LexisNexis Consumer Center website or call 1-888-497-0011.

Can you get a copy of your own CLUE report?

Yes. Consumers can request one free copy of their CLUE report each year from LexisNexis, the company that maintains the database. Reviewing it helps confirm that your insurance claim history is accurate before applying for coverage or comparing quotes.

How much does it cost to get a CLUE report?

Consumers can request one free CLUE report each year from LexisNexis under the Fair Credit Reporting Act. Additional copies may require a small fee.

Enter your ZIP code to find out how much car insurance costs in your area.

How far back does a CLUE report go?

A CLUE report typically includes up to seven years of claim history, but that can vary by state. Our guide to state auto insurance requirements explains more.

Can a CLUE report contain errors?

Yes. Claim information comes from multiple insurers and may be recorded incorrectly or linked to the wrong person or property. Consumers can dispute inaccurate entries with LexisNexis to have them reviewed and corrected.

Can you correct an error on your CLUE report?

Yes. File a dispute with LexisNexis, the company that maintains the report. Provide documentation that supports the correction, and the claim record will be reviewed and updated if the information is inaccurate.

Can a bad CLUE report increase your rates or lead to denial of coverage?

Do all homes have a CLUE report?

Related Articles

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.

![]() Secured with SHA-256 Encryption

Secured with SHA-256 Encryption