At-Fault Accidents & Insurance Rates in 2026

At-fault accidents occur when you are legally responsible for causing a collision, as determined by police reports, insurance investigations, and state laws. An at-fault accident insurance increase can double your rates, but USAA has the cheapest minimum coverage after an at-fault accident at $32 per month.

Read more

Table of Contents

Table of Contents

Insurance Copywriter

Rachel Bodine graduated from college with a BA in English. She has since worked as a Feature Writer in the insurance industry and gained a deep knowledge of state and countrywide insurance laws and rates. Her research and writing focus on helping readers understand their insurance coverage and how to find savings. Her expert advice on insurance has been featured on sites like PhotoEnforced, AllWom...

Rachel Bodine

Managing Editor

Daniel S. Young began his professional career as chief editor of The Chanticleer, a Jacksonville State University newspaper. He also contributed to The Anniston Star, a local newspaper in Alabama. Daniel holds a BA in Communication and is pursuing an MA in Journalism & Media Studies at the University of Alabama. With a strong desire to help others protect their investments, Daniel has writt...

Daniel S. Young

Licensed Insurance Broker

Zach Fagiano has been in the insurance industry for over 10 years, specializing in property and casualty and risk management consulting. He started out specializing in small businesses and moved up to large commercial real estate risks. During that time, he acquired property & casualty, life & health, and surplus lines brokers licenses. He’s now the Senior Vice President overseeing globa...

Zach Fagiano

Updated April 2026

An at-fault accident occurs when you are legally determined to be responsible for causing a collision.

- Fault is determined by state laws, police reports, and insurer review

- USAA has the cheapest insurance rates after an accident at $32 monthly

- Premiums can go up by 50% after an at-fault accident claim

The at-fault claim will be added to your record and CLUE report, increasing premiums by 20%–50%, with surcharges lasting three to five years, depending on your state and insurer.

USAA offers the lowest average minimum coverage at $32 per month for eligible drivers.

Knowing how these accidents are determined and how they affect your coverage can help you take steps to minimize costs. Enter your ZIP code to compare quotes instantly and find the cheapest insurance available.

At-Fault Accidents Defined

When a driver is held legally responsible for causing a crash, it’s called an at-fault accident.

This decision is based on police reports, your insurer’s investigation, and the laws in your state.

Being at fault means your insurance will likely pay for the other driver’s damages through your liability coverage, and in some cases, your own repairs if you have collision coverage.

At-Fault Accidents and Insurance Implications| Category | Details |

|---|---|

| Insurance Impact | Premiums usually rise, especially after major accidents |

| Fault Determination | Based on reports, insurer review, and state law |

| Surcharge Duration | Lasts 3-5 years, depending on insurer and state |

| SR-22 Requirement | Needed for serious violations like DUI or reckless driving |

| Rate Increase Estimate | Typically 20%-50%, varies by state and insurer |

| Coverage Affected | Mostly liability; may impact collision too |

| Claim Filing Process | Report it, send documents, and cooperate |

The most common at-fault accident examples are drivers running stop signs and red lights or not yielding the right of way.

If the accident involves a serious violation like DUI or reckless driving, you may be required to file an SR-22 insurance form to prove you have the proper insurance coverage.

An at-fault accident means you’re legally responsible for the crash, and in severe cases, you may need an SR-22 to prove your insurance meets state requirements.

Michelle Robbins Licensed Insurance Agent

If you’re found at fault in a car accident, your premiums usually go up by 20%–50%, and the increase can last for three to five years, depending on your insurer and state.

The surcharge is typically higher for major accidents involving severe damage or injuries. Most of the time, the increase affects your liability auto insurance coverage, but collision coverage can also be impacted.

Free Auto Insurance Comparison

Compare Quotes From Top Companies and Save

At-Fault Accident Insurance Costs Compared

Rates after an at-fault accident can differ greatly between providers, making it essential to shop around.

USAA offers the lowest minimum coverage at $32 per month and full coverage at $84 per month, though eligibility is limited to military members and their families. Check out more insights in our USAA insurance review.

Auto Insurance Monthly Rates by Coverage Level| Company | Minimum Coverage | Full Coverage |

|---|---|---|

| $87 | $228 | |

| $62 | $166 | |

| $76 | $198 | |

| $43 | $114 | |

| $96 | $248 | |

| $63 | $164 | |

| $56 | $150 | |

| $47 | $123 | |

| $53 | $141 | |

| $32 | $84 |

For full coverage, Geico and State Farm remain competitive at $114 and $123 per month.

Comparing quotes from these top companies can help you secure the most cost-effective coverage after an at-fault accident.

State Farm has the smallest increase at only 21.3%, going from $47 per month for minimum coverage to $57.

USAA stays the cheapest overall, rising from $32 to $42 per month, but it’s only for military members and their families.

Auto Insurance Monthly Rates Before & After an At-Fault Accident| Company | Before Accident | After Accident | % Increase |

|---|---|---|---|

| $87 | $124 | 42.5% | |

| $62 | $94 | 51.6% | |

| $76 | $109 | 43.4% | |

| $43 | $71 | 65.1% | |

| $96 | $129 | 34.4% | |

| $63 | $88 | 39.7% | |

| $50 | $98 | 96.0% | |

| $47 | $57 | 21.3% | |

| $53 | $76 | 43.4% | |

| $32 | $42 | 31.3% |

Nationwide and Liberty Mutual also keep their increases under 40%, which is lower than many others.

On the other hand, Progressive and Geico see the biggest jumps, with Progressive’s rates almost doubling and Geico’s going up by more than 65%.

At-fault accident points on your license will raise your rates higher than a collision caused by weather or animals, essentially making you a high-risk driver.

High-risk auto insurance rates can differ greatly between providers, and most companies will drop coverage if you have too many at-fault accidents, making it essential to shop around.

Read More: Cheap Auto Insurance for High-Risk Drivers

How At-Fault Accidents Impact Costs

Your monthly premiums are directly related to the number of accidents in your area. Traffic accidents have been steadily increasing since 2020.

While property damage is more common, bodily injury claims are much more expensive, which increases insurance costs for all drivers.

In at-fault states, drivers who cause an accident are responsible for covering the other party’s injuries.

However, having personal injury protection (PIP) or medical payments coverage (MedPay) can help cover your own medical bills so you aren’t paying out-of-pocket for everyone.

Definition Card")

PIP is more common in no-fault states, but is available in some at-fault states. It provides benefits for medical expenses, lost wages, and even essential services, regardless of fault.

MedPay is a simpler option that covers medical costs but doesn’t pay for lost income. Adding these coverages will raise your rates, so compare quotes online to get the best price.

Understanding At-Fault vs. No-Fault Auto Insurance

All states follow different systems for deciding who pays after a traffic accident. Read More: Diminished Value Claims

Most states use an at-fault system, where the driver responsible for the crash must cover the other party’s damages, typically through liability insurance.

Some states follow a no-fault insurance system. No-fault accident examples include incidents where each driver’s own insurance pays for their medical expenses, no matter who ran the red light.

A few states, like New Jersey and Pennsylvania, use a choice no-fault system, allowing drivers to choose between at-fault or no-fault rules when buying coverage. Learn More: Best Auto Insurance Companies in PA

In at-fault states, liability insurance is essential because it pays for the other driver’s injuries and property damage if you cause an accident.

However, liability does not cover your own car repairs, so you will have to carry extra coverage to pay for your medical bills and vehicle repairs.

Drivers who want more protection often choose full coverage, which includes liability, collision, and comprehensive auto insurance.

Understanding these differences helps ensure you have the right level of insurance for your state’s rules.

Investigating At-Fault Accidents

Figuring out who is responsible after a car accident is an important step in the claims process because it impacts who pays for damages and how insurance rates are affected.

Fault is determined by a mix of evidence, official reports, and state laws, and you may need to hire an at-fault accident attorney to help you navigate local laws.

- Police Reports: Officers document details at the scene, including statements, evidence, and citations.

- State Laws: Rules for right-of-way, speed limits, and other traffic laws guide fault decisions.

- Insurance Investigation: Adjusters review damage, photos, witness statements, and accident reconstructions.

- Type of Accident: Certain collisions, like rear-end crashes, often have clear fault patterns.

- Comparative or Contributory Negligence: In some states, fault can be shared, affecting how much each driver pays.

Learning how to get multiple auto insurance quotes can help you find an insurance company that keeps costs down after a crash. See how much you could save on coverage by entering your ZIP code into our free quote comparison tool.

Frequently Asked Questions

What does “at-fault accident” mean?

The at-fault accident meaning determines who is legally responsible for causing a collision based on state laws, police reports, and the insurance company’s investigation.

Which is better, no-fault or at-fault insurance?

Neither system is better for every driver. No-fault systems can speed up medical payments and reduce lawsuits, while at-fault systems may allow more opportunities to recover damages from the responsible driver.

What happens if it’s my fault in a car accident?

If you’re at fault, your insurance typically pays for the other driver’s damages through liability coverage. Your rates may go up, and you may also have to pay for your own repairs unless you have collision auto insurance coverage.

What happens if I’m at fault in a car accident in California?

California is an at-fault state, meaning the driver who caused the accident must pay for the other driver’s damages. Your insurance will cover these costs up to your policy limits, and your rates may increase.

Learn More: Best Auto Insurance Companies in California

Who is usually at fault in a car crash?

It depends on the situation. In rear-end collisions, the driver in back is often at fault, while in left-turn accidents, the turning driver is usually responsible. Each case is different and depends on the evidence.

How do insurance companies prove who is at fault?

Insurers review police reports, witness statements, accident photos, damage patterns, and sometimes traffic camera footage. They also compare these details against state traffic laws to decide responsibility. Enter your ZIP code in our free tool to start seeing quotes today.

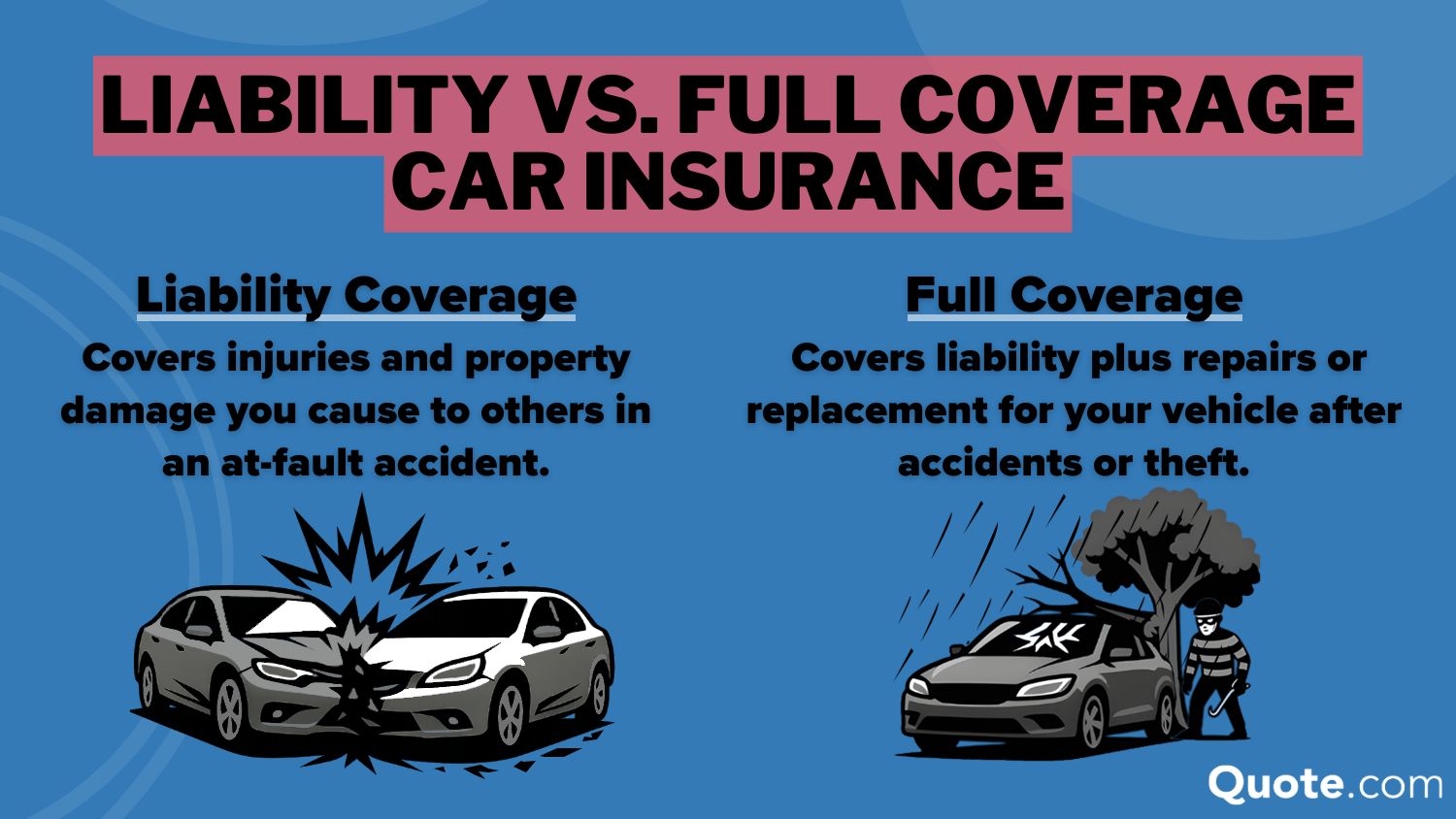

Does full coverage cover at-fault accidents?

Yes. Full coverage includes collision insurance, which can help pay for your car repairs after an at-fault accident, in addition to liability coverage for the other driver’s damages.

Read More: Liability vs. Full Coverage Auto Insurance

Should I file an insurance claim if I am at fault?

Yes, in most cases you should. Not filing can lead to out-of-pocket costs for damages or injuries, and failing to report an accident may violate your policy terms.

How do I win an at-fault accident claim?

To challenge an at-fault decision, provide evidence such as photos, dashcam footage, or witness statements. You can also request a review by your insurer or file a dispute if you believe the decision is wrong. Browse our guide on how to file an auto insurance claim and win each time.

What happens in a fault claim?

The insurance company investigates the accident, determines who is responsible, and pays for covered damages based on that decision. If you are at fault, your liability coverage pays for the other party’s losses.

How does insurance work if it was my fault?

Related Articles

-

Mar 2026

Best Commercial Auto Insurance in 2026

-

Jun 2026

Liability vs. Full Coverage Auto Insurance in 2026

-

May 2026

Roadside Assistance Coverage in 2026

-

May 2026

10 Best Auto Insurance Companies in Iowa for 2026

-

Jun 2026

Salvage Title: Insurance, Registration, & Resale Implications in 2026

-

Apr 2026

Diminished Value Claims (2026)

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.