FR-44 Auto Insurance in 2026: Cost, Requirements, & How it Works

FR-44 filings can increase auto insurance premiums by 94%. In Florida, FR-44 auto insurance raises DUI rates from $72 to $136 monthly. In Virginia, rates increase from $58 to $110 a month. Because drivers with FR-44s must carry higher liability limits, costs are higher. Bundling policies or paying in full may help you save.

Read more

Table of Contents

Table of Contents

Insurance Copywriter

Malory Will has an M.A. in English from Arizona State University. She has over four years of experience in writing for the insurance industry. With a background in health, auto, life, and homeowners insurance, Malory is passionate about making complex insurance topics clear and approachable. Her goal is to help readers make informed decisions with confidence.

Malory Will

Head of Content

Meggan McCain, Head of Content, has been a professional writer and editor for over a decade. She leads the in-house content team at Quote.com. With three years dedicated to the insurance industry, Meggan combines her editorial expertise and passion for writing to help readers better understand complex insurance topics. As a content team manager, Meggan sets the tone for excellence by guiding c...

Meggan McCain

Commercial Lines Coverage Specialist

Michael Vereecke is the president of Customers First Insurance Group. He has been a licensed insurance agent for over 13 years. He also carries a Commercial Lines Coverage Specialist (CLCS) Designation, providing him the expertise to spot holes in businesses’ coverage. Since 2009, he has worked with many insurance providers, giving him unique insight into the insurance market, differences in ...

Michael Vereecke

Updated May 2026

FR-44 auto insurance helps drivers with a DUI in Florida and Virginia meet state requirements and get their licenses back by providing 100/300/50 liability coverage.

- FR-44 auto insurance requires nonstop coverage after a DUI

- Virginia FR-44 drivers need a 100/300/50 DUI liability filing

- FR-44 drivers in Florida face a 3-year filing rule after a DUI

Major insurance companies such as State Farm, Progressive, and Geico offer FR-44 filings and send the FR-44 form straight to the state. They may also give discounts if you bundle policies, take a defensive driving course, or pay in full.

High-risk drivers need to keep FR-44 coverage active to avoid losing their license or restarting the filing process. Find cheap FR-44 car insurance quotes by entering your ZIP code into our free comparison tool.

Understanding FR-44 Insurance Costs

To get FR-44 insurance after a serious DUI conviction, you need to compare high-risk providers and pick a policy with higher liability limits.

You’ll need to keep your coverage active after your insurer files the FR-44 form. Missing payments can restart the filing period and may lead to your license being suspended again.

If you get a DUI in Florida or Virginia, your FR-44 auto insurance costs will go up quickly. Learn More: Cheap Auto Insurance After a DUI

Auto-Owners keeps monthly premiums close to $98 after a DUI, while The General raises rates sharply to $182 per month after serious violations.

FR-44 Auto Insurance Monthly Rates by Provider: Before vs. After DUI| Company | Before DUI | After DUI | Increase | % Change |

|---|---|---|---|---|

| $78 | $142 | $64 | +82% | |

| $69 | $129 | $60 | +87% | |

| $52 | $98 | $46 | +88% | |

| $56 | $108 | $52 | +93% | |

| $55 | $104 | $49 | +89% | |

| $64 | $121 | $57 | +89% | |

| $71 | $138 | $67 | +94% | |

| $59 | $112 | $53 | +90% | |

| $94 | $182 | $88 | +94% | |

| $70 | $132 | $62 | +89% |

Geico stays near $104 monthly, while Erie rates jump 93% after a DUI. State Farm remains cheaper than Progressive and Allstate.

It’s a good idea to compare several FR-44 providers right away, since a single DUI can increase monthly premiums by more than $88 after filing.

Top Reasons Why FR-44 Insurance Costs More

Insurance companies set FR-44 premiums in different ways. Each violation, credit tier, and coverage lapse affects how risky a driver seems to them.

Find Out More: Cheap Auto Insurance for High-Risk Drivers

Drivers in cities who have DUI records and full coverage often see their monthly premiums go up after insurers review their driving history.

Factors That Affect FR-44 Auto Insurance Rates

| Variable | Cost Impact |

|---|---|

| Age & Gender | Higher risk increases rates |

| Claims History | Recent claims raise premiums |

| Coverage Limits | Higher limits increase cost |

| Credit Score Tier | Good credit lowers rates |

| Driving History | Violations increase premiums |

| DUI/DWI Offense | These cause much higher rates |

| Insurance Carrier | Rates vary by insurer pricing |

| Location & ZIP | Urban areas have higher rates |

| Marital Status | Married drivers often pay less |

| Payment Method | Upfront pay may reduce cost |

| Policy Type Option | Full coverage increases cost |

| Previous Insurance | Coverage lapse raises rates |

| SR-22 or FR-44 | FR-44 filing increases rates |

| State Filing Rules | State rules impact premiums |

| Time Since Violation | Premiums decrease over time |

| Vehicle Type & Use | Vehicle use affects premiums |

Having good credit, making payments on time, and going longer without violations can help lower FR-44 costs over time. Insurers tend to reward drivers who show financial stability.

After a serious violation, it is important to compare different insurance companies. Some insurers charge high-risk drivers much more than others.

Breaking Down What Impacts FR-44 Insurance Prices

DUI convictions cause the largest increases in FR-44 insurance rates. After a serious alcohol-related violation, insurers often raise premiums by almost 90%.

Drivers with poor credit scores may see their rates go up by another 40%. Choosing higher liability limits can also raise premiums by about 45%.

Living in an urban ZIP code or having a lapse in your policy can also make FR-44 insurance more expensive. Insurers pay close attention to traffic density and any gaps in coverage.

If you keep your mileage low and drive safely over time, your premiums may go down. Insurers tend to reward drivers who show fewer long-term risks.

Check Out This Page: How Mileage Affects Auto Insurance Rates

FR-44 Premiums for Different Insurance Policies

FR-44 insurance costs rise quickly because DUI drivers must carry higher liability limits and high-risk coverage.

DUI convictions cause the biggest FR-44 premium increases because insurers treat alcohol related violations as high financial risks.

FR-44 Auto Insurance Monthly Rates by Coverage Level| Coverage Level | Premium | Liability Limits |

|---|---|---|

| Minimum | $110–$150 | 100/300/50 |

| Mid-Level | $130–$165 | 100/300/100 |

| High-End | $150–$200 | 250/500/100 |

Even drivers with just the minimum required liability coverage may see their rates go up by about 94%. See our article: Cheapest Liability-Only Auto Insurance

Basic FR-44 insurance coverage typically costs between $110 and $150 each month. If you select higher limits, your monthly premium could go up to $200.

Drivers with a DUI conviction usually pay nearly 94% more for FR-44 insurance, even if they only carry the minimum required liability coverage.

Melanie Musson Published Insurance Expert

Mid-level plans cost $130 to $165 per monthly and offer stronger liability protection after license suspensions.

Drivers who pick higher FR-44 limits often avoid high out-of-pocket costs after an accident. Serious claims can go beyond what state minimum coverage pays.

Comparing FR-44 Policy Costs in Florida vs. Virginia

Only Florida and Virginia require drivers to carry FR-44s with more liability coverage before they can get their licenses back. Read more: Best Auto Insurance Companies in Florida

In Florida, monthly insurance premiums jump from $72 to $136. Car insurance companies in Virginia increase from $58 to nearly $110 per month after a DUI.

FR-44 Auto Insurance Monthly Rates by State: Before vs. After DUI| State | Clean Record | After DUI | Increase | % Change |

|---|---|---|---|---|

| Florida | $72 | $136 | $64 | +89% |

| Virginia | $58 | $110 | $52 | +90% |

You should keep your FR-44 coverage active. If your policy lapses, you could get a suspended license, face new filing periods, and pay even higher monthly premiums.

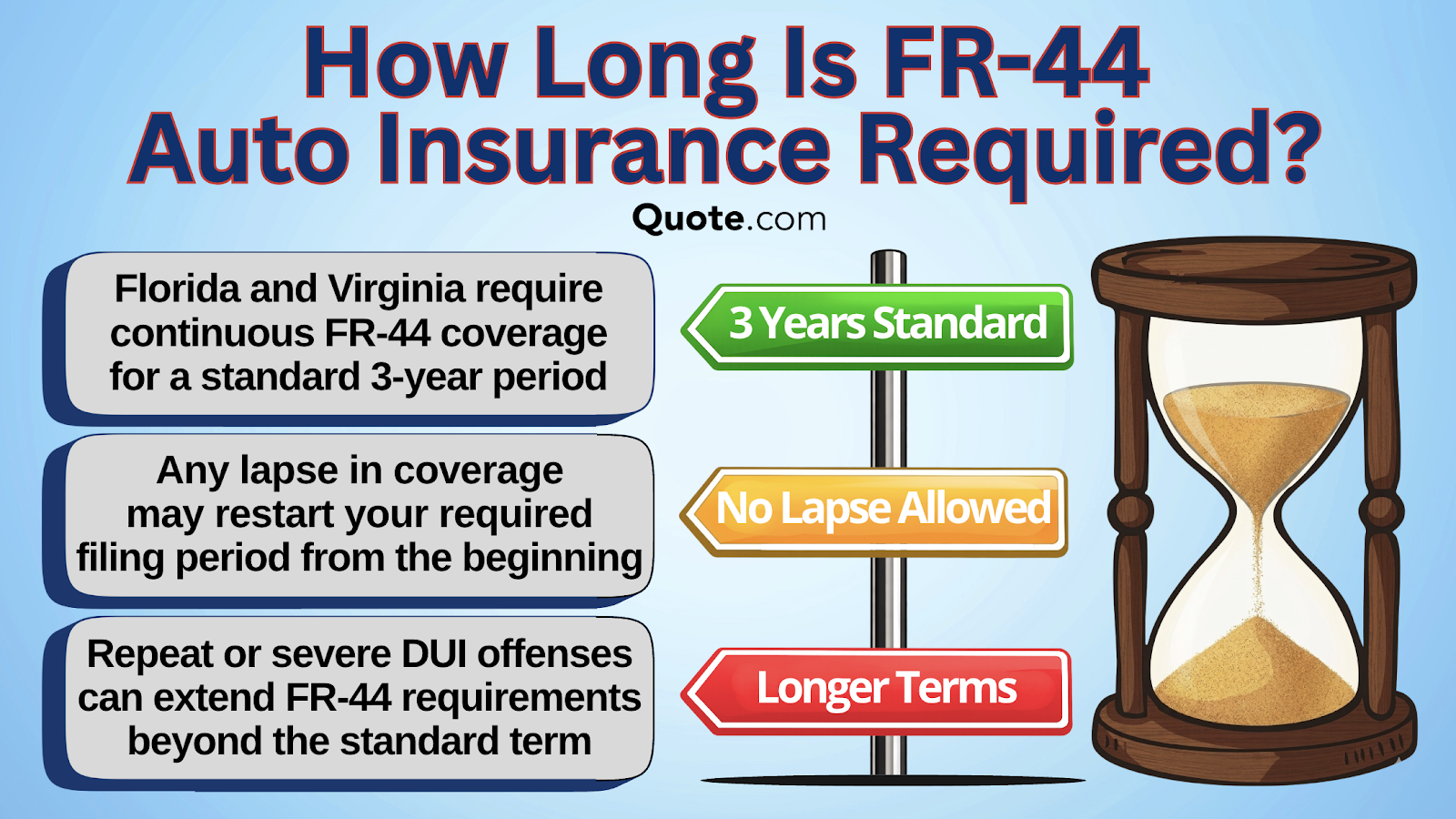

In Florida and Virginia, drivers with serious DUI convictions are usually required to have FR-44 coverage for three straight years before they can get their full driving privileges back.

If your coverage lapses, the filing period can start over. Also, if you have more than one DUI, you might have to keep FR-44 coverage for longer than three years.

Insurers watch for violations and carefully check compliance histories and CLUE reports at every renewal, so it’s important to make your payments and keep your FR-44 policy active.

How High-Risk Driving Affects Car Insurance Rates

Serious driving violations can significantly increase auto insurance costs. Insurers view suspended licenses and DUI convictions as costly long-term risks.

After a DUI, drivers with minimum coverage usually pay about $150 per month. Full coverage high-risk auto insurance can cost around $255 per month.

Reckless driving also leads to high costs. Minimum coverage averages $130 per month, and full coverage can be nearly $220 per month.

If you lose your license, minimum coverage can cost $145 per month, and full coverage auto insurance may rise to about $245 per month.

Drivers in their forties with prior violations often face stricter renewal reviews. Insurers pay close attention to payment history and accident records.

Shopping around for insurance soon after a major violation can help drivers avoid big premium increases. Some companies are tougher on high-risk histories than others.

Free Auto Insurance Comparison

Compare Quotes From Top Companies and Save

FR-44 Policy Requirements Drivers Need to Know

After a DUI, drivers in Florida and Virginia must follow strict FR-44 rules, which require much higher liability coverage right away.

Insurance companies send electronic proof that you have at least 100/300/50 coverage, and you need to keep your policy active for about three years without any gaps.

FR-44 Auto Insurance Limits, Costs, & Requirements| Category | Details |

|---|---|

| Applicable State Rules | Applies only in Florida and Virginia |

| Coverage Lapse Rules | Any lapse may restart required term |

| DUI/DWI Requirement | Triggered after DUI/DWI conviction |

| Filing Fee Range | One-time fee varies by provider |

| Filing Responsibility | Filed by your insurer with the state |

| Florida Liability Limits | Minimum limits set at 100/300/50 |

| FR-44 Filing Purpose | Confirms active high-limit coverage |

| FR-44 Policy Exclusion | Is not an insurance policy on its own |

| License Reinstatement | Required to restore driving privileges |

| Minimum Coverage | Higher than basic state requirements |

| Non-Owner Policy | Available without owning a vehicle |

| Policy Cancellation | Cancellation could suspend license |

| Policy Reinstatement | Reinstatement may restart your term |

| Premium Increase | High rates charged after DUI or DWI |

| Proof Filing Method | Filed electronically by your provider |

| Typical Filing Duration | Required for a standard 3-year period |

| Upfront Payment Rules | Upfront payment might be required |

| Virginia Liability Limits | Typically double state minimum limits |

If your coverage lapses or you miss a payment, the filing period can start over, and the state might suspend your license again if your policy is canceled.

Even if you do not own a car, you can get a non-owner FR-44 policy, but some insurers may ask for a bigger upfront payment before starting your coverage.

Don’t Miss It: How to File an Auto Insurance Claim & Win

Pros and Cons of FR-44 Car Insurance

To get your driving privileges back after a DUI, you usually need to keep FR-44 insurance active at all times while the state monitors your compliance.

Courts and DMVs accept FR-44 filings from approved insurance companies, but drivers still have to meet stricter rules and higher liability limits after a DUI.

FR-44 Auto Insurance Benefits & Limitations| Pros | Cons |

|---|---|

| Accepted by state authorities | May involve strict state oversight |

| Allows continued legal driving | May not apply to all motorists |

| Applies to high-risk drivers | Applies after serious violations |

| Available from major insurers | Fewer insurer options available |

| Enables license reinstatement | Required after major offenses |

| Enables return to legal driving | May delay full driving privileges |

| Ensures proof of coverage filing | Ongoing coverage proof required |

| Helps avoid additional penalties | Does not eliminate all penalties |

| Insurer files proof with the state | May increase insurer involvement |

| Keeps coverage state-compliant | Requires strict policy compliance |

| Maintains legal driving status | Must maintain without any lapses |

| Meets state filing requirements | Includes higher filing requirements |

| Offers non-owner policy option | Not all insurers offer this option |

| Provides higher liability limits | Requires higher liability coverage |

| Provides required liability limits | May increase coverage pricing |

| Recognized by courts and DMV | May involve court or DMV review |

| Restores driving privileges faster | May take time to fully reinstate |

| Supports post-DUI compliance | Linked to DUI or DWI convictions |

If you do not own a car, you may qualify for non-owner FR-44 insurance. This option lets you meet legal requirements without buying a regular auto policy.

If you miss payments or cancel your policy early, you could face new penalties. States may suspend your license again if you do not stay in compliance.

Get The Details: Auto Insurance Requirements by State

Key Differences Between FR-44 vs. SR-22

A lot of drivers with serious violations are confused about how SR-22 vs. FR-44 filings differ. Both filings help people get their driving privileges back after certain offenses.

SR-22 auto insurance filings usually last for two to three years. FR-44 filings require higher liability limits and last at least three years.

SR-22 vs. FR-44 Insurance Filing Comparison| Category | SR-22 | FR-44 |

|---|---|---|

| Duration | 2-3 year requirement | 3 year minimum |

| Liability Limits | State minimum limits | Higher liability limits |

| Required for | DUI or serious offenses | DUI conviction only |

| States Used | Used in 44 states | Used in Florida & Virginia |

| Trigger Severity | High-risk violations | Severe DUI offenses |

Most states accept SR-22 filings after a reckless driving conviction or a driving without insurance conviction, but FR-44 coverage is required only in Florida and Virginia.

FR-44 rules are meant for severe DUI convictions, since states want stricter liability protections before fully restoring suspended licenses.

Drivers with FR-44 coverage usually pay higher monthly premiums because insurers see alcohol-related violations as higher financial risks.

Carefully comparing SR-22 and FR-44 insurance requirements helps drivers avoid mistakes, since filing errors can quickly lead to another license suspension.

Drivers with FR-44 coverage usually pay higher monthly premiums because insurers see alcohol-related violations as higher financial risks.

Carefully comparing SR-22 and FR-44 requirements helps drivers avoid mistakes, since filing errors can quickly lead to another license suspension.

State Rules for FR-44 & SR-22 Filings

Most drivers just need to file an SR-22. FR-44 forms are only required in Florida and Virginia, and only after serious DUI convictions.

States like Texas, California, and Illinois often require SR-22 filings. However, many other states do not require additional insurance paperwork after an incident.

FR-44 policies usually come with higher liability limits and longer monitoring periods because states consider alcohol-related violations to be greater financial risks.

Drivers who move to a new state should check their filing requirements carefully. Missing these steps can cause registration problems or even lead to a suspended license.

If you are convicted of a DUI in Florida or Virginia, you will usually need an FR-44 filing. In other states, SR-22 coverage is more common after a license suspension.

If you do not have major violations or unresolved insurance problems, you probably will not need either filing. States usually require these forms only for higher-risk situations.

Check Out This Page: Best Auto Insurance Companies in Virginia

Lowering Your FR-44 High-Risk Insurance Rates

You can lower your high-risk FR-44 insurance premiums by earning discounts. Insurers often reward drivers who drive safely and pay their bills on time.

Telematics programs can save you up to 30%. If you bundle your home and auto policies, you might lower your monthly costs by nearly 25%.

Top Auto Insurance Discounts for FR-44 Drivers| Discount | Eligibility | Savings |

|---|---|---|

| Accident-Free | No recent at-fault claims | 10% |

| Anti-Theft | Installed anti-theft tech | 15% |

| Auto Pay | Enroll in auto pay plan | 5% |

| Bundling | Bundle home and auto | 25% |

| Defensive Driving | Complete driving class | 10% |

| Driver Training | Finish driver training | 10% |

| Early Shopper | Quote before renewal | 8% |

| Electronic Billing | Enrollment in e-billing | 5% |

| Full Payment | Pay policy fully upfront | 10% |

| Good Student | Maintain strong grades | 15% |

| Homeowner | Own primary residence | 10% |

| Loyalty | Maintain active policy | 10% |

| Low Mileage | Drive fewer miles yearly | 15% |

| Military | Active or former military | 15% |

| Multi-Policy | Hold multiple policies | 20% |

| Multi-Vehicle | Insure two or more cars | 25% |

| Paperless | Switch to paperless | 5% |

| Safe Driver | Maintain clean record | 20% |

| Senior Driver | Driver age 55 or older | 10% |

| Telematics | Enroll in telematics | 30% |

| Vehicle Safety | Vehicle safety features | 15% |

Using anti-theft devices, keeping your mileage low, or insuring more than one vehicle can often get you extra discounts of 15% to 25%.

Taking a defensive driving course and enrolling in automatic payments can help lower your FR-44 costs and improve your insurance record over time.

You can lower the high cost of FR-44 insurance after a DUI by bundling your policies, signing up for automatic payments, and taking a defensive driving course.

You might also save more by insuring multiple vehicles, adding anti-theft features, or paying your policy in full.

Check It Out: Best Anti-Theft Auto Insurance Discounts

Free Auto Insurance Comparison

Compare Quotes From Top Companies and Save

Get Affordable FR-44 Auto Insurance Coverage

Finding affordable FR-44 coverage can be challenging. After a DUI, drivers are moved into stricter high-risk insurance categories, which makes rates go up.

Always compare providers before you file an FR-44 so you don’t end up overpaying for coverage. Learn More: Best Car Insurance Companies

In Florida, monthly premiums often rise from $72 to $136. In Virginia, rates typically range from $58 a month to nearly $110 monthly after a DUI.

Some insurers, like Auto-Owners, keep post-DUI premiums around $98 per month. Others, such as The General, raise rates sharply to about $182 per month.

FR-44 filings raise premiums because insurers track risky behavior closely, and DUI convictions raise rates the most.

Daniel Walker Licensed Insurance Agent

Once you find a provider that fits your budget, ask them to file the FR-44 when your policy starts.

Drivers can lower their long-term costs by using telematics discounts, which may save up to 30%. Find cheap FR 44 auto insurance quotes with our free comparison tool today.

Frequently Asked Questions

What is FR-44 car insurance?

FR-44 auto insurance isn’t actually insurance coverage, but proof that high-risk drivers carry the increased liability limits required after a DUI.

What does FR stand for in insurance?

The FR in FR-44 stands for “financial responsibility,” reflecting the increased policy limits on FR-44 filings.

How much extra is FR-44 insurance?

FR-44 insurance usually increases monthly premiums by 82% to 94% after a DUI because drivers must carry higher liability limits. Learn More in Our Guide: Liability auto insurance

What is the average cost of FR-44 insurance in Florida?

The average cost of FR-44 insurance in Florida rises from about $72 to $136 monthly after a DUI conviction and filing requirement.

How long do drivers have to carry FR-44 insurance in Florida?

Florida drivers typically must keep FR-44 insurance active for 3 continuous years after a DUI-related license suspension. Find affordable FR 44 insurance quotes by entering your ZIP code into our free online comparison tool today.

Can drivers get FR-44 insurance without vehicle coverage?

Drivers can get FR44 insurance without vehicle ownership through non-owner policies that satisfy Florida or Virginia filing requirements. Read Our Article for More Details: Driving Without Auto Insurance

What is the cheapest FR-44 insurance in Florida?

Auto-Owners offers some of the cheapest FR-44 insurance in Florida, with post-DUI rates starting near $98 per month.

Can drivers pay FR-44 monthly in Florida?

Most insurers allow monthly FR-44 payments in Florida, though some may require larger upfront payments following serious violations.

How long do you need FR-44 insurance after a DUI?

Drivers usually need FR-44 insurance for at least 3 continuous years after a DUI conviction in Florida or Virginia. Explore Our Guide: Auto Insurance Rates by State

Can you pay FR-44 monthly in Virginia?

Most insurance companies allow monthly FR-44 payments in Virginia, though higher upfront deposits may be required after severe violations. Enter your ZIP code to compare monthly auto insurance quotes in Virginia.

How long do you need FR-44 insurance in Virginia?

How long does FR-44 take to process?

Is FR-44 more expensive than SR-22?

What is the cheapest car insurance in Florida after a DUI?

Does State Farm FR-44 insurance support DUI filings?

Does Geico do FR-44 insurance?

Does Allstate offer FR-44 insurance in Florida?

Related Articles

-

Mar 2026

Progressive Auto Insurance Review for 2026

-

Jun 2026

10 Best Auto Insurance Companies in Wyoming for 2026

-

Oct 2025

10 Best Auto Insurance Companies in Utah for 2026

-

Jun 2026

The Best Time to Buy a New Car in 2026

-

Jun 2026

Travelers Insurance Review: Customer Ratings & Coverage Breakdown (2026)

-

Jan 2026

Cheap Auto Insurance for Low-Income Drivers in 2026

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.