Best Home Insurance in Wisconsin for 2026

The best home insurance in Wisconsin comes from Amica, The Hartford, and Chubb. Rates start at just $68 per month with Erie. Homeowners looking for the best home and auto insurance in Wisconsin can save up to 24%, or about $575 annually, by bundling eligible policies.

Read more

Save Money by Comparing Insurance Quotes

Compare Free Home Insurance Quotes Instantly

Table of Contents

Table of Contents

Social Media Manager & Professor

Ashley Dannelly has a Master of Arts in English and serves as the Social Media Manager for Quote.com's portfolio of websites. Ashley also teaches English at Columbia International University and other higher education institutions. Ashley’s background in English and media has allowed her the unique opportunity to edit and create content for many publications, including Livestrong and DiveIn....

Ashley Dannelly

Senior Director of Content

Sara Routhier, Senior Director of Content, has professional experience as an educator, SEO specialist, and content marketer. She has over 10 years of experience in the insurance industry. As a researcher, data nerd, writer, and editor, she strives to curate educational, enlightening articles that provide you with the must-know facts and best-kept secrets within the overwhelming world of insurance....

Sara Routhier

Licensed Insurance Agent

Travis Thompson has been a licensed insurance agent for nearly five years. After obtaining his life and health insurance licenses, he began working for Symmetry Financial Group as a State Licensed Field Underwriter. In this position, he learned the coverage options and limits surrounding mortgage protection. He advised clients on the coverage needed to protect them in the event of a death, critica...

Travis Thompson

Updated July 2026

Amica, The Hartford, and Chubb offer the best home insurance in Wisconsin. Affordable home insurance rates start as low as $68 per month.

- Amica offers up to 18% savings through home and auto bundling

- State Farm leads bundle savings with a 24% discount worth $575

- Erie offers Wisconsin’s lowest rate with a $5K deductible

Erie offers the lowest monthly premium in the state with a $5K deductible, while Amica ranks as the top overall provider for its exceptional claims service.

Wisconsin homeowners can expect rates to vary based on coverage limits, deductible choices, credit history, and property risks such as wind, hail, and water damage.

Top 10 Companies: Best Home Insurance in Wisconsin| Company | Rank | Claims Satisfaction | Complaints | Best for |

|---|---|---|---|---|

| #1 | 773 / 1,000 | Low | Claims Service | |

| #2 | 756 / 1,000 | Mid | AARP Members | |

| #3 | 744 / 1,000 | Low | High-Value | |

| #4 | 722 / 1,000 | Mid | Policy Bundles | |

| #5 | 720 / 1,000 | Low | Add-On Options | |

| #6 | 719 / 1,000 | Low | Local Agents | |

| #7 | 704 / 1,000 | Mid | Online Quotes | |

| #8 | 700 / 1,000 | Low | Wisconsin Roots | |

| #9 | 700 / 1,000 | Low | Green Homes | |

| #10 | 681 / 1,000 | Low | Agent Support |

This guide compares the best home insurance rates in Wisconsin, coverage options, discounts, common risks, and leading providers.

Compare quotes to find the right Wisconsin homeowners insurance policy at the best price. Enter your ZIP code into our free comparison tool to find the cheapest home insurance rates.

Compare Home Insurance Premiums in Wisconsin

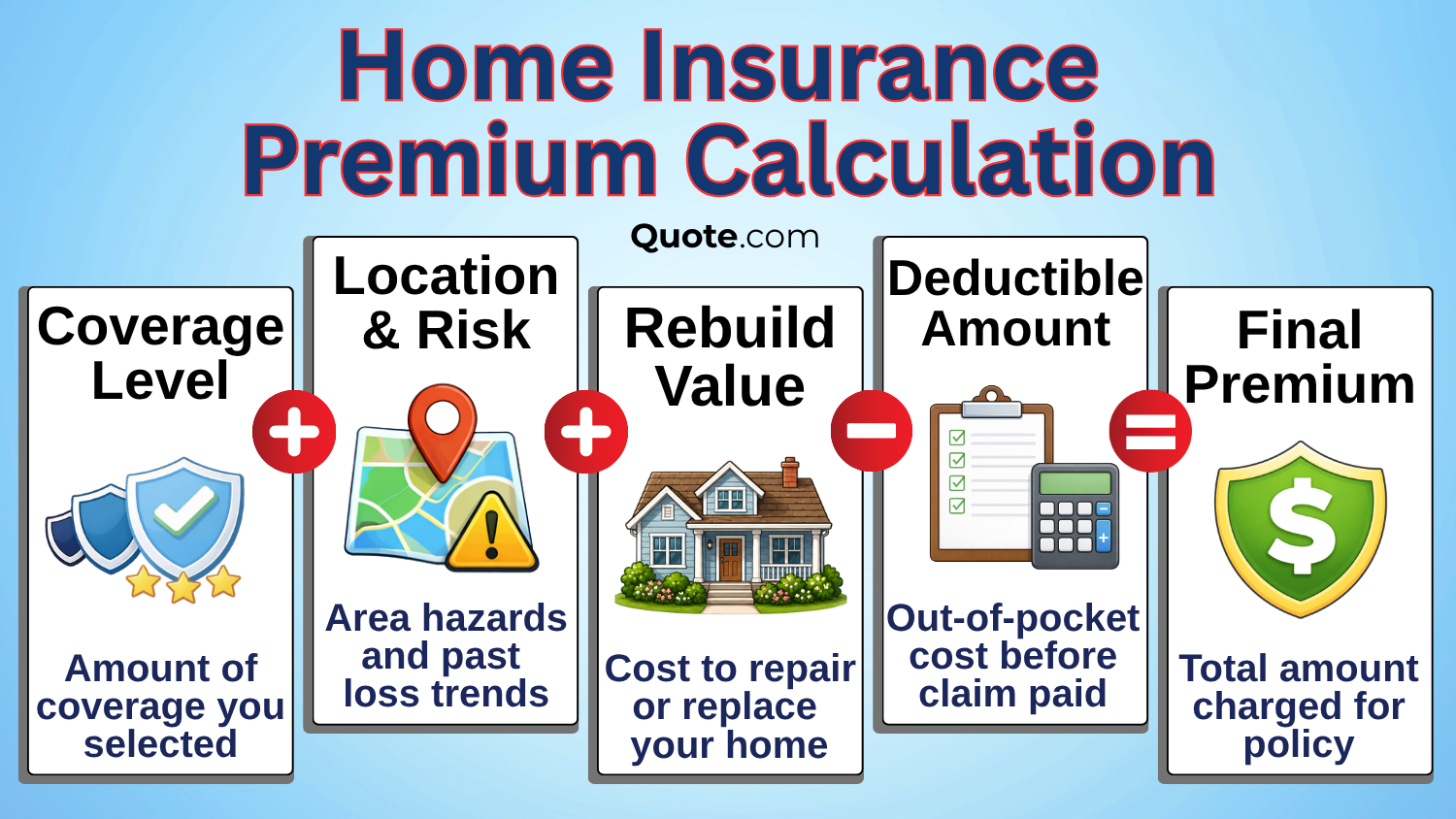

Home insurance premiums in Wisconsin remain well below the national average, although rates have steadily increased over time.

Wisconsin homeowners pay about $92 per month on average, compared to the U.S. average of $167, making the state one of the more affordable markets for homeowners coverage.

Insurance costs can vary significantly based on factors such as a home’s age and condition, geographic location, prior claims activity, deductible amount, and the level of coverage selected.

Understanding how these factors affect pricing can help Wisconsin homeowners compare policies more effectively and find the right balance between protection and affordability.

Important Details: How much homeowners insurance do you need?

Average Costs From Home Insurance Providers in Wisconsin

Dwelling coverage is one of the biggest factors affecting homeowners insurance costs in Wisconsin. As dwelling coverage increases from $200K to $500K, monthly premiums rise across all providers to reflect the higher replacement costs.

Erie offers the lowest rates overall, starting at $76 per month for $200K in dwelling coverage and $146 per month for $500K in coverage.

Wisconsin Home Insurance Monthly Rates by Dwelling Coverage| Company | $200K | $300K | $400K | $500K |

|---|---|---|---|---|

| $103 | $135 | $166 | $197 | |

| $78 | $102 | $126 | $149 | |

| $92 | $121 | $149 | $177 | |

| $112 | $147 | $181 | $215 | |

| $76 | $100 | $123 | $146 | |

| $95 | $125 | $154 | $183 | |

| $100 | $131 | $161 | $191 | |

| $86 | $113 | $139 | $165 | |

| $96 | $126 | $155 | $184 | |

| $82 | $108 | $133 | $158 |

Dwelling coverage protects the physical structure of your home and is designed to cover rebuilding or repair costs after a covered loss.

Higher dwelling coverage limits in Wisconsin generally result in higher premiums because insurers assume greater financial risk.

Wisconsin homeowners should choose a dwelling coverage amount that reflects their home’s replacement cost rather than its market value to ensure adequate protection without overpaying for coverage.

Evaluating Wisconsin homeowners insurance quotes and selecting the right coverage limit helps prevent costly out-of-pocket expenses.

How Wisconsin Home Insurance Deductibles Affect Rates

A home insurance deductible is the amount you must pay out of pocket before your insurer contributes toward a covered claim.

In Wisconsin, choosing a lower deductible generally results in higher monthly premiums, while selecting a higher deductible can reduce insurance costs.

Home Insurance Deductibles in Wisconsin: Premium Impact| Category | $500 | $1K | $2K | $5K |

|---|---|---|---|---|

| Best Use | File Often | Less Often | Low Cost | Rare Claims |

| Claim Payout | Largest | High | Moderate | Smallest |

| Claim Rate | Highest | Moderate | Low | Lowest |

| Monthly Rate | $101 | $94 | $87 | $83 |

| Rate Stability | Lowest | Moderate | High | Highest |

Average premiums range from $101 per month with a $500 deductible to $83 per month with a $5K deductible, showing how increasing your deductible can lower home insurance costs in Wisconsin.

A $500 deductible offers larger claim payouts and lower out-of-pocket costs after a loss, while a $5K deductible provides lower monthly premiums and greater rate stability.

Wisconsin Home Insurance Monthly Rates by Deductible| Company | $500 | $1K | $2K | $5K |

|---|---|---|---|---|

| $113 | $103 | $98 | $93 | |

| $86 | $78 | $74 | $70 | |

| $101 | $92 | $87 | $83 | |

| $123 | $112 | $106 | $101 | |

| $84 | $76 | $72 | $68 | |

| $105 | $95 | $90 | $86 | |

| $110 | $100 | $95 | $90 | |

| $95 | $86 | $82 | $77 | |

| $106 | $96 | $91 | $86 | |

| $90 | $82 | $78 | $74 |

However, higher deductibles also mean paying more before coverage begins, making it important to choose a deductible that provides adequate Wisconsin homeowners insurance coverage.

Premiums vary significantly by insurer and deductible level. Erie and Amica offer some of the lowest rates in Wisconsin, with premiums falling to $68 and $70 per month, respectively, at a $5,000 deductible.

For Wisconsin homeowners, a higher deductible can reduce insurance costs, but it's important to choose an amount you can afford after a covered loss.

Jeff Root Licensed Insurance Agent

Homeowners looking to reduce monthly costs may benefit from higher deductibles, but they should ensure they have enough savings available to cover the deductible amount if a covered loss occurs.

Comparing quotes from multiple providers can help you find the best homeowners insurance in Wisconsin for your coverage needs and budget.

How Much Insurance Coverage Wisconsin Homeowners Need

The amount of homeowners insurance coverage you need in Wisconsin should be based on your home’s replacement cost rather than its market value.

Most insurers recommend carrying enough dwelling coverage to fully rebuild your home after a covered loss, which often requires coverage limits that exceed the property’s purchase price.

Estimated Coverage, Costs, & Risk Levels in Wisconsin| Home Value | Coverage | Monthly Rate | Rebuild Costs | Exposure |

|---|---|---|---|---|

| $200K | $220K | $98 | Very Low | Standard |

| $225K | $250K | $107 | Low | Standard |

| $250K | $275K | $114 | Low | Standard |

| $275K | $300K | $121 | Moderate | Standard |

| $300K | $330K | $129 | Moderate | Standard |

| $350K | $385K | $145 | Moderate | Elevated |

| $400K | $440K | $160 | High | Elevated |

| $450K | $495K | $176 | High | Elevated |

| $500K | $550K | $190 | High | Substantial |

| $600K | $660K | $217 | Very High | Substantial |

As home values increase from $200K to $600K, recommended coverage amounts rise from $220K to $660K to account for construction, labor, and material costs.

Homeowners with lower-valued properties may pay around $98 per month for coverage, while those with higher-value homes can expect premiums to exceed $200 per month.

How Credit Affects Wisconsin Home Insurance Costs

Your credit score can have a significant impact on home insurance in Wisconsin, because insurers often use it to predict the likelihood of future claims.

In Wisconsin, Erie’s rates increase from $76 per month for homeowners with excellent credit to $179 per month for those with poor credit.

Wisconsin Home Insurance Monthly Rates by Credit Score| Company | Excellent (800+) | Good (670-799) | Fair (580-669) | Poor (<580) |

|---|---|---|---|---|

| $103 | $134 | $180 | $242 | |

| $78 | $101 | $137 | $183 | |

| $92 | $120 | $161 | $216 | |

| $112 | $146 | $196 | $263 | |

| $76 | $99 | $133 | $179 | |

| $95 | $124 | $166 | $223 | |

| $100 | $130 | $175 | $235 | |

| $86 | $112 | $151 | $202 | |

| $96 | $125 | $168 | $226 | |

| $82 | $107 | $144 | $193 |

Homeowners with lower credit scores may face higher premiums because they are statistically more likely to file claims or miss payments.

Maintaining good credit may help homeowners qualify for lower premiums and more affordable Wisconsin homeowners insurance quotes without reducing coverage.

Check Out This Page: Best Insurance for High-Risk Homes

Risks That Impact Wisconsin Homeowners Insurance

Weather-related hazards play a major role in Wisconsin homeowners insurance costs, with wind and hail representing the most common source of claims statewide.

Water damage, flooding, fire, lightning, and winter freezes can also increase premiums, particularly for homes located in higher-risk areas.

Wisconsin Home Insurance Monthly Rates by Risk Factor| Company | Fire Risk | Tornado Risk | Water Damage | Wind & Hail |

|---|---|---|---|---|

| $121 | $117 | $131 | $129 | |

| $91 | $88 | $99 | $97 | |

| $108 | $104 | $117 | $115 | |

| $132 | $127 | $143 | $142 | |

| $89 | $86 | $96 | $95 | |

| $112 | $108 | $121 | $119 | |

| $118 | $114 | $128 | $126 | |

| $101 | $97 | $109 | $108 | |

| $113 | $109 | $122 | $121 | |

| $96 | $93 | $104 | $103 |

This can be especially important in Wisconsin, where severe weather, water damage, frozen pipes, and wind-related losses can lead to costly claims.

Erie and Amica offer some of the most affordable rates across these risk categories, with premiums starting at $86 and $88 per month, respectively, for tornado-related risks.

Homeowners can use a Wisconsin homeowners insurance calculator to estimate how factors such as credit score, coverage limits, and deductible choices may affect their premiums and overall insurance costs.

Because exposure to these hazards can affect both coverage availability and pricing, homeowners should evaluate the specific risks in their area before choosing a policy.

5 Most Common Home Insurance Risks in Wisconsin| Risk | Claims | Payout | Cost | Area |

|---|---|---|---|---|

| #1 – Wind & Hail | 32% | $17K | Moderate | South & West |

| #2 – Water Damage | 24% | $13K | Moderate | Statewide |

| #3 – Flooding | 14% | $28K | High | Flood Zones |

| #4 – Fire & Lightning | 9% | $82K | Very High | Rural Areas |

| #5 – Winter Freeze | 8% | $15K | Moderate | North & Central |

Comparing quotes, coverage options, and customer feedback in homeowners insurance Wisconsin reviews can help identify the best fit for your needs.

Researching the best home insurance Wisconsin Reddit discussions can be a good place to start, but verify recommendations against coverage details, claims service, and pricing in your area before making a decision.

How Home Insurance Premiums Vary Across Wisconsin

Location plays a major role in Wisconsin home insurance costs because weather patterns, property risks, and rebuilding expenses differ across the state.

Average monthly premiums range from about $92 to more than $215, with higher rates often found in counties that face greater exposure to wind, hail, water damage, and severe storms.

Wisconsin areas with higher construction and labor costs may also require larger coverage limits, increasing the cost of insurance.

Homes in northern and eastern Wisconsin may face different risks than properties in central or western counties, resulting in noticeable differences in premiums even when coverage amounts are similar.

Factors such as local claim frequency, weather-related losses, and rebuilding costs can all influence rates.

Comparing Wisconsin home insurance rates by state can help homeowners better understand regional pricing differences and find coverage that fits both their budget and risk profile.

Free Home Insurance Comparison

Compare Quotes From Top Companies and Save

Home Insurance Policy Options in Wisconsin

Wisconsin homeowners insurance coverage typically includes several core protections that help safeguard your home, belongings, and finances from unexpected losses.

While coverage varies by insurer, these are the five most important policy options homeowners should understand before choosing coverage.

- Dwelling Coverage: Pays to repair or rebuild your Wisconsin home after a covered loss.

- Personal Property Coverage: Covers belongings damaged or stolen by covered perils.

- Personal Liability Coverage: Helps pay legal and medical expenses if you’re responsible for injuries or property damage.

- Additional Living Expenses (ALE): Covers temporary housing and other living costs while your Wisconsin home is being repaired.

- Optional Endorsements: Add protection for flood, earthquake, valuable personal property, or roof replacement that standard policies may not fully cover.

Wisconsin homeowners should review these coverage options carefully and consider endorsements based on local risks such as flooding, wind, hail, and winter freeze damage to ensure their policy provides adequate protection.

Most insurers offer earthquake protection as an add-on. Amica and Erie offer flood coverage, but it’s typically available through the National Flood Insurance Program (NFIP) or private insurers. Compare Now: Amica vs. Auto-Owners Review

Home Insurance Coverage Options in Wisconsin| Company | Earthquake | Flood | Roof | Valuables |

|---|---|---|---|---|

| ⚠️Add-On | ⚠️NFIP | ✅RCV | ⚠️Add-On | |

| ⚠️Add-On | ✅ | ✅RCV | ⚠️Add-On | |

| ⚠️Add-On | ⚠️Private | ✅RCV | ⚠️Add-On | |

| ⚠️Add-On | ⚠️Private | ✅RCV | ✅ | |

| ⚠️Add-On | ✅ | ✅RCV | ⚠️Add-On | |

| ⚠️Add-On | ⚠️NFIP | ✅RCV | ⚠️Add-On | |

| ⚠️Add-On | ✅ | ✅ACV | ⚠️Add-On | |

| ⚠️Limited | ✅ | ✅ACV | ⚠️Limited | |

| ⚠️Add-On | ⚠️NFIP | ✅RCV | ⚠️Add-On | |

| ⚠️Add-On | ⚠️Private | ✅RCV | ⚠️Add-On |

Chubb stands out by including coverage for valuable personal property, while most other insurers require additional endorsements.

Homeowners comparing policies should review available coverage options carefully to ensure their Wisconsin homeowners insurance coverage addresses local risks such as flooding, severe weather, and property damage.

The most common homeowners insurance policy in Wisconsin is the HO-3 Special Form, which accounts for 63% of policies statewide.

Understanding these policy options can help homeowners select Wisconsin homeowners insurance coverage that matches their property’s value, age, and protection needs.

Common Restrictions on Wisconsin Homeowners Insurance

Many Wisconsin homeowners insurance policies include restrictions that can affect eligibility, coverage, and claims payments.

Common limitations involve roof age requirements, home inspections, wind and hail coverage restrictions, and winter freeze exclusions or reviews.

Wisconsin Home Insurance Restrictions by Company| Company | Inspection? | Roof Limit | Wind & Hail | Winter Freeze |

|---|---|---|---|---|

| ⚠️by Age | 20 Yrs | ⚠️by Review | ⚠️by Review | |

| ⚠️by Age | 20 Yrs | ⚠️Limited | ⚠️by Review | |

| ⚠️by Age | 20 Yrs | ⚠️by Age | ⚠️by Review | |

| ⚠️High-Value | ✅None | ⚠️ by Cost | ✅ | |

| ⚠️by Age | 20 Yrs | ⚠️by Age | ⚠️by Review | |

| ⚠️Exterior Only | 15 Yrs | ⚠️ by Cost | ⚠️Limited | |

| ⚠️by Age | 15 Yrs | ⚠️Limited | ⚠️Limited | |

| ⚠️Exterior Only | 15 Yrs | ⚠️ by Cost | ⚠️Limited | |

| ⚠️by Age | 20 Yrs | ⚠️Limited | ⚠️by Review | |

| ⚠️Exterior Only | 20 Yrs | ⚠️by Age | ⚠️by Review |

Several insurers, including American Family, Amica, Erie, and The Hartford, may apply additional underwriting requirements for older roofs.

These restrictions are especially important in Wisconsin because severe winter weather, hailstorms, and freezing temperatures can increase the likelihood of property damage claims.

Before buying WI homeowners insurance, review roof age limits, inspection requirements, and weather-related restrictions to avoid surprises during a claim.

Michelle Robbins Licensed Insurance Agent

Some best home insurance companies may require inspections before issuing coverage or limit protection based on a home’s age, condition, or location.

Homeowners should carefully review policy terms and Wisconsin homeowners insurance coverage details to understand any exclusions, coverage limitations, or inspection requirements before purchasing a policy.

Tips on Saving on Wisconsin Home Insurance

Wisconsin homeowners can save money in several other ways. Insurance companies also consider factors such as your deductible, claims history, home condition, and coverage selections when calculating rates.

Taking steps to reduce risk and improve your home’s insurability may help you qualify for lower premiums while maintaining strong Wisconsin homeowners insurance coverage.

- Higher Deductibles: Choose a deductible between $1K and $5K to reduce monthly premiums if they can afford higher out-of-pocket costs after a claim.

- Home Updates: Replacing older roofs, plumbing, or electrical systems can help lower risk and qualify for more affordable coverage.

- Review Coverage: Regularly reviewing policy coverage before your renewal period can help prevent overinsurance and keep long-term costs under control.

- Safety Devices: Installing water leak detectors, smoke alarms, and monitored security systems may help reduce losses and earn insurance savings.

Bundling home and auto insurance is one of the most effective ways to lower homeowners insurance costs in Wisconsin.

State Farm offers the largest bundle discount at 24%, helping eligible customers save an average of $575 per year, while Allstate and Nationwide also provide substantial savings opportunities.

10 Best Home & Auto Insurance Bundle Discounts in Wisconsin| Company | Rank | Discount | Savings | Bundle Rules |

|---|---|---|---|---|

| #1 | 24% | $575 | Bundled Billing | |

| #2 | 20% | $420 | New Policies | |

| #3 | 17% | $297 | Existing Customers | |

| #4 | 16% | $285 | Auto Customers | |

| #5 | 15% | $265 | Multiple Vehicles | |

| #6 | 15% | $245 | Active Auto | |

| #7 | 14% | $220 | Early Shopper | |

| #8 | 13% | $210 | Loyalty Bundle | |

| #9 | 12% | $190 | Online Enrollment | |

| #10 | 10% | $170 | Military Only |

Many insurers reward policyholders who combine multiple policies, maintain existing coverage, or meet specific eligibility requirements such as bundled billing or multiple vehicles.

Comparing bundle discounts from the best home and auto insurance in Wisconsin can also help you simplify policy management through a single insurer.

Additional Wisconsin Homeowners Insurance Discounts

Wisconsin homeowners can lower their insurance costs through a variety of discounts beyond home and auto bundling.

Amica offers some of the largest savings, including discounts of up to 18% for bundling, 12% for new homes, 9% for remaining claims-free, and 6% for home security features.

Top Home Insurance Discounts in Wisconsin| Company | Bundling | New Home | No Claims | Security |

|---|---|---|---|---|

| 16% | 10% | 8% | 5% | |

| 18% | 12% | 9% | 6% | |

| 16% | 11% | 7% | 5% | |

| 12% | 9% | 6% | 7% | |

| 13% | 10% | 8% | 5% | |

| 15% | 9% | 7% | 6% | |

| 17% | 11% | 8% | 6% | |

| 12% | 8% | 6% | 5% | |

| 16% | 10% | 7% | 5% | |

| 14% | 9% | 8% | 6% |

Nationwide, American Family, and Auto-Owners also provide competitive discount opportunities for eligible policyholders.

Taking advantage of multiple discounts can significantly reduce Wisconsin homeowners insurance premiums while maintaining strong coverage and protection for your home.

Get More Details: 26 Hacks to Save Money on Insurance

Top Home Insurance Companies in Wisconsin

Wisconsin’s homeowners insurance market is led by well-established national and regional carriers, with American Family holding the largest market share at 21%.

These companies insure hundreds of thousands of homes across the state and maintain strong financial ratings, reflecting their ability to pay claims and support policyholders after covered losses.

10 Largest Home Insurance Companies in Wisconsin| Company | Market Share | Policy Count | Premiums Written | Financial Rating |

|---|---|---|---|---|

| 21% | 380K | $525M | A | |

| 17% | 302K | $417M | A+ | |

| 8% | 142K | $196M | A+ | |

| 6% | 103K | $137M | A+ | |

| 5% | 88K | $122M | A | |

| 4% | 76K | $104M | A+ | |

| 3% | 58K | $79M | A++ | |

| 3% | 52K | $72M | A | |

| 2% | 39K | $54M | A++ | |

| 2% | 36K | $50M | A+ |

Market share and financial strength can help homeowners evaluate an insurer’s stability and ability to pay claims.

However, reviewing each company’s pros and cons is equally important for comparing the cheapest home insurance companies, coverage options, discounts, claims service, and overall value.

#1 – Amica: Top Pick Overall

Pros

- Claims Service: Amica offers some of the best home insurance in Wisconsin, with rates starting at $78 per month and the highest claims satisfaction score in the rankings.

- Low Complaints: Wisconsin homeowners benefit from Amica’s consistently low complaint volume and strong customer retention.

- Policy Features: Amica provides robust Wisconsin homeowners insurance coverage with customizable endorsements and replacement-cost options.

Cons

- Limited Agents: Wisconsin homeowners who prefer face-to-face service may find fewer local offices than regional carriers.

- Fewer Discounts: Some Wisconsin competitors offer a broader selection of policy discounts and bundle incentives. See Details: Amica Insurance Review

#2 – The Hartford: Best for AARP Members

Pros

- AARP Benefits: Wisconsin seniors can access exclusive AARP member perks, policy features, and savings through The Hartford.

- Claims Support: Wisconsin homeowners benefit from a strong 756/1,000 claims satisfaction score and dependable customer service.

- Coverage Options: The Hartford offers broad Wisconsin homeowners insurance coverage with protection for common property risks.

Cons

- Membership Requirement: Many of The Hartford’s best Wisconsin benefits are reserved for eligible AARP members.

- Mid Complaints: Wisconsin policyholders may encounter a higher complaint ratio than some top-ranked competitors.

#3 – Chubb: Best for High-Value

Pros

- Luxury Coverage: Chubb is ideal for Wisconsin homeowners with high-value properties requiring enhanced protection.

- Valuable Items: Wisconsin policies can include expanded coverage for jewelry, artwork, collectibles, and other valuables.

- Claims Reputation: Chubb’s strong claims satisfaction score reflects reliable service for Wisconsin homeowners.

Cons

- Higher Premiums: Wisconsin homeowners often pay more for Chubb’s premium coverage features. Compare More Details: Replacement Cost vs. Actual Cash Value

- Limited Value: Budget-focused Wisconsin homeowners may find more affordable options elsewhere.

#4 – Liberty Mutual: Best for Policy Bundles

Pros

- Bundle Savings: Liberty Mutual helps Wisconsin homeowners save by combining home and auto insurance policies.

- Flexible Coverage: Wisconsin customers can customize policies with a variety of endorsements and optional protections.

- Digital Access: Liberty Mutual offers convenient online tools for Wisconsin policy management and claims tracking.

Cons

- Mid Complaints: Wisconsin homeowners may experience more customer complaints than with some higher-ranked insurers.

- Roof Restrictions: Older Wisconsin homes may face stricter underwriting requirements for roof coverage. Read our guide for a detailed look: Liberty Mutual Insurance Review

#5 – Nationwide: Best for Add-On Options

Pros

- Add-On Options: Nationwide provides Wisconsin homeowners with numerous endorsements and optional protections.

- Discount Programs: Wisconsin policyholders can reduce costs through bundling, protective devices, and loyalty discounts.

- Low Complaints: Our Nationwide insurance review shows the company maintains a favorable complaint record among Wisconsin home insurers.

Cons

- Higher Rates: Wisconsin homeowners may find lower premiums from providers like Erie or Amica.

- Coverage Limits: Certain Wisconsin endorsements may have eligibility requirements or coverage restrictions.

#6 – Erie: Best for Local Agents

Pros

- Affordable Rates: Erie offers Wisconsin homeowners some of the state’s lowest premiums, starting at $76 per month.

- Local Agents: Wisconsin customers receive personalized guidance from local independent agents.

- Customer Service: Erie’s low complaint ratio and strong satisfaction ratings support its reputation in Wisconsin.

Cons

- Limited Technology: Wisconsin homeowners seeking advanced digital tools may find fewer options than national competitors.

- Regional Focus: As noted in our Erie insurance review, it serves a smaller footprint than many large Wisconsin insurance providers.

#7 – Progressive: Best for Online Quotes

Pros

- Online Quotes: Progressive makes it easy for Wisconsin homeowners to compare rates and purchase coverage online.

- Competitive Pricing: Wisconsin customers benefit from below-average premiums and flexible policy options.

- Digital Tools: Progressive offers user-friendly online account management and claims services. More Insights: Progressive Insurance Review

Cons

- Mid Complaints: Wisconsin homeowners may encounter a higher complaint ratio than with several top-ranked insurers.

- Agent Access: Local Wisconsin agent support may not be as extensive as some regional competitors.

#8 – American Family: Best for Wisconsin Roots

Pros

- Wisconsin Roots: American Family’s longstanding Wisconsin presence provides local market expertise.

- Agent Network: Wisconsin homeowners have access to a large network of local agents and support resources.

- Market Leadership: American Family insures more Wisconsin homes than any other carrier in the state.

Cons

- Higher Costs: Wisconsin homeowners may pay more than they would with lower-cost competitors.

- Lower Scores: Claims satisfaction trails several higher-ranked Wisconsin providers.

#9 – Travelers: Best for Green Homes

Pros

- Green Coverage: Travelers supports Wisconsin homeowners with coverage options for eco-friendly home upgrades.

- Financial Strength: Wisconsin policyholders benefit from Travelers’ A++ financial strength rating.

- Competitive Rates: Travelers Insurance offers affordable Wisconsin homeowners insurance with solid coverage options.

Cons

- Limited Discounts: Wisconsin homeowners may find fewer discount opportunities than with some competitors.

- Older Homes: Certain Wisconsin properties may face underwriting restrictions based on age or condition.

#10 – Auto-Owners: Best for Agent Support

Pros

- Agent Support: Auto-Owners provides Wisconsin homeowners with personalized service through independent agents.

- Competitive Rates: Wisconsin customers receive affordable coverage backed by strong financial stability.

- Low Complaints: Auto-Owners maintains a positive reputation among Wisconsin homeowners for customer service.

Cons

- Basic Technology: Wisconsin homeowners may find fewer digital tools than those offered by larger insurers. Find Out More: Auto-Owners Insurance Review

- Fewer Options: Some Wisconsin homeowners may prefer carriers with a broader selection of endorsements and add-ons.

Free Home Insurance Comparison

Compare Quotes From Top Companies and Save

Finding the Best Wisconsin Homeowners Insurance

The best home insurance companies in Wisconsin depend on your home’s value, location, coverage needs, and budget.

Amica ranks as the top overall provider for its exceptional claims service, strong customer satisfaction, and competitive rates, while The Hartford and Chubb excel for AARP members and high-value homes, respectively.

Homeowners should also consider factors such as deductible options, available endorsements, financial strength, and customer satisfaction when comparing insurers.

A policy with the lowest premium may not always provide the best value if it offers fewer coverage options or stricter policy limitations. Wisconsin’s changing weather conditions make it especially important to choose coverage that fits your property’s unique risks.

Strong claims service can save you far more than a slightly lower premium after a major loss.

Chris Abrams Licensed Insurance Agent

Evaluating policy exclusions, replacement cost limits, and available discounts can help ensure your home is adequately protected while keeping insurance costs manageable.

Reviewing multiple Wisconsin homeowners insurance quotes can help you identify the right balance of coverage, service, and affordability.

Your home deserves adequate protection. If you’re looking for home insurance coverage that won’t break your budget, enter your ZIP code into our quote comparison tool to get started.

Frequently Asked Questions

What is the best homeowners insurance company in Wisconsin?

Amica is one of the best homeowners insurance companies in Wisconsin due to its industry-leading claims satisfaction score, low complaint ratio, and competitive rates starting at $78 per month.

Don’t Miss It: Home Insurance for New Construction

Who has the cheapest homeowners insurance rates in Wisconsin?

Erie offers some of the lowest home insurance rates in Wisconsin, with premiums starting at $68 per month when paired with a $5K deductible. Amica and Travelers also provide affordable rates while maintaining strong coverage options and customer satisfaction scores.

What does homeowners insurance cover in Wisconsin?

Most Wisconsin homeowners insurance policies cover your home’s structure, personal belongings, personal liability, and additional living expenses if your home becomes uninhabitable after a covered loss. Optional endorsements are available for flood, earthquake, roof replacement, and valuable personal property, depending on the insurer.

How much homeowners insurance coverage do I need in Wisconsin?

Most Wisconsin homeowners should carry enough dwelling coverage to fully rebuild their home after a covered loss. Insurers typically recommend coverage limits based on replacement cost rather than market value to account for labor and construction expenses.

What deductible should I choose for homeowners insurance in Wisconsin?

The best deductible depends on your budget and financial situation. A higher deductible can lower your monthly premium, while a lower deductible reduces your out-of-pocket costs if you file a claim. Choose a deductible you can comfortably afford after a covered loss. Make sure to compare home insurance rates by entering your ZIP code to avoid overpaying.

Does credit score affect homeowners insurance rates in Wisconsin?

Yes. Many insurers use credit-based insurance scores when determining premiums. Homeowners with strong credit often qualify for lower Wisconsin homeowners insurance rates, while lower credit scores can lead to higher premiums for the same level of coverage.

What weather risks affect Wisconsin home insurance?

Wisconsin homeowners commonly face risks from wind and hail storms, water damage, flooding, fire, lightning, and winter freezes. Wind and hail account for the largest share of claims, while flooding and fire often result in the highest claim payouts. For natural disaster risks, you may also want to understand whether home insurance policies cover wildfire damage.

How can I lower my Wisconsin homeowners insurance premium?

Homeowners can reduce premiums by increasing deductibles, bundling home and auto policies, upgrading older home systems, installing security devices, and maintaining a claims-free history. Comparing Wisconsin homeowners insurance quotes from multiple providers can also help identify lower rates.

Is flood insurance included in Wisconsin homeowners insurance?

Standard homeowners insurance policies generally do not cover flood damage. Wisconsin homeowners in flood-prone areas may need separate flood insurance through the National Flood Insurance Program (NFIP) or a private flood insurance provider for adequate protection.

What factors affect homeowners insurance rates in Wisconsin?

Insurance companies consider several factors when calculating premiums, including your home’s location, age, replacement cost, deductible, claims history, credit score, and exposure to weather-related risks. Comparing multiple quotes is the best way to find the right coverage at a competitive price. Get the perfect home insurance policy at the best price by using our free comparison tool.

Related Articles

-

Jun 2026

Best Home Insurance in Nebraska for 2026

-

Jun 2026

Best Home Insurance in Hawaii for 2026

-

Jul 2026

Best Home Insurance in Alabama for 2026

-

Mar 2026

How to File a Wildfire Home Insurance Claim in 2026

-

Jun 2026

Vacant Home Insurance: Cost, Coverage, & Risks Explained (2026)

-

Jun 2026

Best Home Insurance in Delaware for 2026

Get a FREE Quote in Minutes

Insurance rates change constantly — we help you stay ahead by making it easy to compare top options and save.